Baker Hughes (BHI) delivered Q3 revenue of $3.79 billion, which hit analysts’ target on the button. After the company reported a sequential decline in revenue of 31% in Q1, I have been one of Baker Hughes’ biggest detractors. However, things may be looking up. I had the following takeaways on the quarter:

North America Is Still A Problem

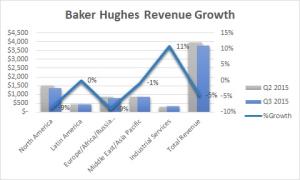

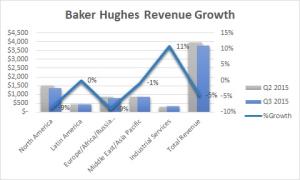

The oil industry E&P is still down, but revenue declines are not as dramatic in comparison to previous quarters. Total revenue was off 5% sequentially.

Revenue from North America and Europe/Africa/Russia both fell 9% Q/Q. North American land drillers have been the most hard-hit segment of the oil services space. Shale plays have some of the highest production costs in the industry. At oil prices sub-$50, they may not have the cash flow to fund capex. Meanwhile the Europe/Africa/Russia segment was hit by a decline in the rig count and unfavorable exchange rates, particularly in Russia and Norway.

According to the company, next quarter North America could get worse due to lower commodity prices and the impact of the holidays. Since North America still represents 36% of revenues, its demise will continue to hold back revenue growth.

Cost Containment Efforts

The oil industry downturn seemed to have caught Baker Hughes off guard as its EBITDA margins shrank from around 15% in Q4 2014 to less than 10% in Q1 2015. Among the big four — Halliburton (HAL), Schlumberger (SLB) and Weatherford (WFT) — Baker Hughes still has the lowest EBITDA margin. Through head count reductions and other cost containment efforts, Q3 margins increased to 14% despite continued revenue declines.

Gross margins have declined since Q4 due to price concessions demanded by clients. This appears out of the company’s control. However, management has cut SG&A expense and R&D costs in lockstep with revenue declines. From a management execution standpoint, this was probably the best longs could have asked for this quarter.

Related Posts

Risk-Blind And The Great Bear Market Coming

Risk-Blind And The Great Bear Market Coming Indian Indices End Marginally Lower; FMCG Stocks Witness Losses

Indian Indices End Marginally Lower; FMCG Stocks Witness Losses- Bovespa-based bank expands loan porfolio

Memecoin mania hits Base: Obscure tokens skyrocket amid rug pulls and FOMO

Memecoin mania hits Base: Obscure tokens skyrocket amid rug pulls and FOMO Fossil Fuels Are Toast – But Real Assets Are Still The Place To Be

Fossil Fuels Are Toast – But Real Assets Are Still The Place To Be 10 Stocks For Using A Benjamin Graham Value Investing Strategy – December 2016

10 Stocks For Using A Benjamin Graham Value Investing Strategy – December 2016

Leave A Comment