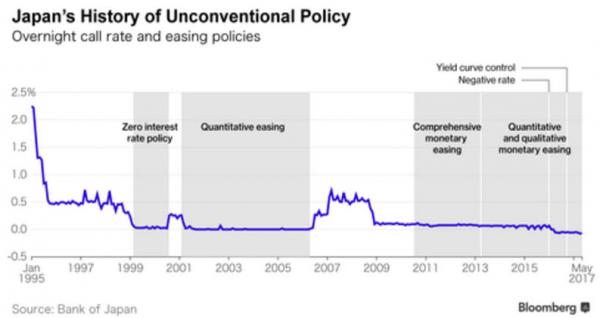

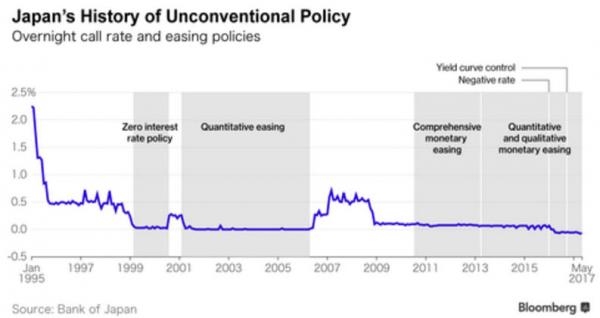

Japan’s long and sordid dance with unconventional monetary policy continues. With most analysts expecting a ‘nothingburger’ from Kuroda (though some hinting at the potential for shock-and-awe), The BOJ delivered… nothing – no change. However, most critically, the BOJ admitted defeat of deflation and delayed the timing of reaching their 2% inflation goal to around FY2019.

No change to policy:

But…

BOJ Raises Assessment of Economy – FY2017 GDP forecast is 1.8%, FY2018 GDP Forecast Is 1.4%, FY2019 GDP Forecast Is 0.7% – But sees risk skewed to the downside.

Growth to Continue Above Potential Through Fiscal 18

Japan Economy Likely to Continue Moderate Expansion

Risk to Economy, Prices Skewed to Downside

BOJ Delays Timing of Reaching 2% Goal to Around FY2019 – BOJ FY2018 Core CPI Forecast Is 1.5%

“Around FY 2019” means in the year ending March, 2020. So the board probably won’t have to revisit this issue for quite some time.

Price Momentum Not Yet Sufficiently Firm

Inflation Expectations Remain in Weakening Phase

As Bloomberg’s Chief Asia Economics Correspondent noted, the statement reads very dovish to me. An impartial observer landing from Mars could only conclude the BOJ’s massive stimulus has a long way to go yet.

The BOJ’s distorting effect in the stock market is in focus today, after Bloomberg scoops on concerns among BOJ officials and the head of Japan’s stock exchange with the scale of ETF purchases.

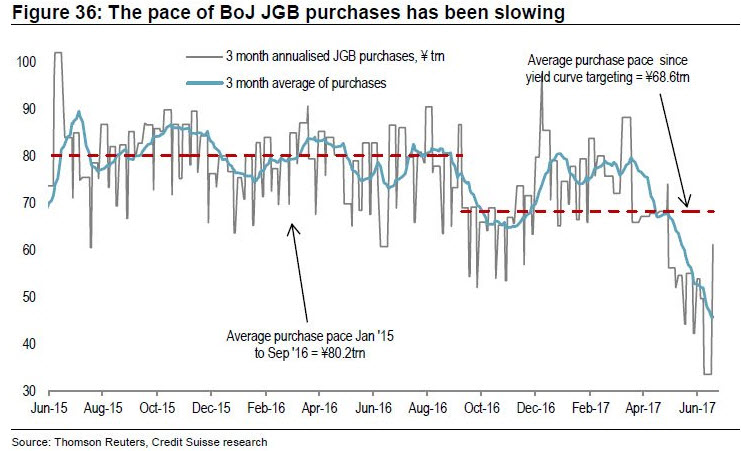

While policy is held unchanged, the Bank of Japan has tapered its purchases without spooking investors into thinking its scaling back stimulus – by switching to the yield-curve target as its priority.

But with ETFs, there’s no obvious bait-and-switch option to change the focus from what’s now solely a quantitative target. It’s very hard to see the BOJ adopting, for example, a stock-price target in the way that it now targets yields.

Related Posts

7 Myths Of Investing

7 Myths Of Investing 4 Water Utility Stocks For A Thirsty Portfolio

4 Water Utility Stocks For A Thirsty Portfolio Divergences Occurring In This Market

Divergences Occurring In This Market- Continued Increase In Silver Buying & Future Supply Disruptions

- In Praise Of A Genuine Gold (Not Gold-Backed) Bond

E

It Is Easy To Understand Why The U.S. Has Backed Down On NAFTA Deadlines With Canada

E

It Is Easy To Understand Why The U.S. Has Backed Down On NAFTA Deadlines With Canada

Leave A Comment