Crocs (CROX – Snapshot Report) announced disappointing quarterly results last Thursday, missing the Zacks EPS consensus by over 400%. The company reported $-0.31 EPS for the quarter, missing the analyst consensus of $+0.10 by $-0.41.

The company delivered revenue of $274.1 million for the quarter, slightly missing expectations of $275.63 million. This performance was down -9.4% compared to the same quarter a year ago.

Much of the damage was already priced-in to CROX shares as the company had warned about the their difficult turn-around at an Investor Day on September 30. In two days surrounding the event and lowered guidance, the stock fell over 20% from $14 to $11.

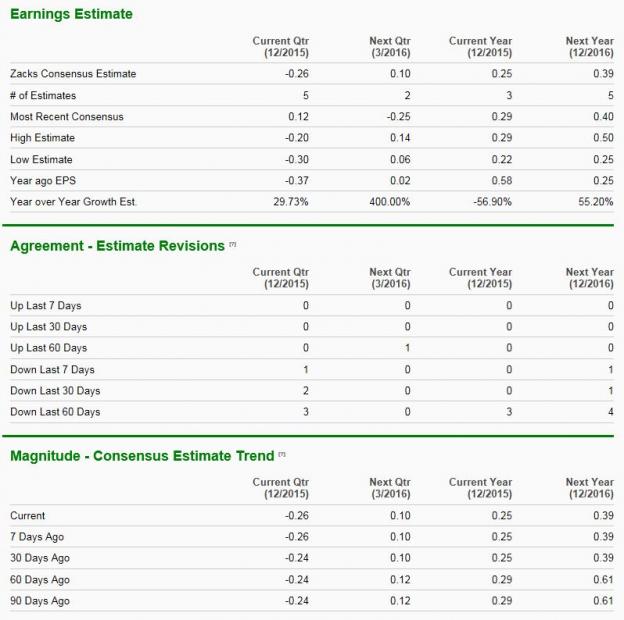

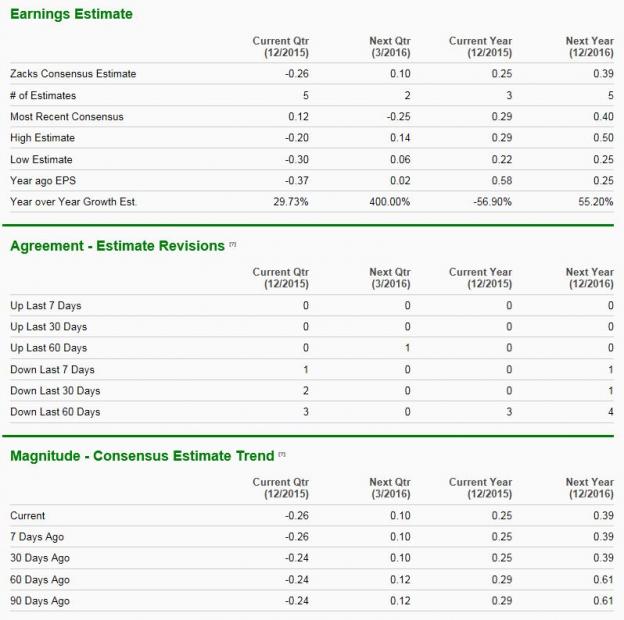

Here are the Zacks Detailed EPS tables which told investors to stay away from the stock headed into this report…

As you can see, the bulk of downward estimate revisions took place right after the Investor Day when next year’s consensus dropped a whopping 36% from $0.61 to $0.39. That estimate would still represent 55% EPS growth over this year.

But the company is in the middle of a slow transition to turn strongly profitable again and so that still puts these estimates in jeopardy.

How Long the Turnaround?

October was an exciting month for athletic and leisure footwear companies with Nike (NKE – Analyst Report) shares soaring to new all-time highs on strong global growth and Skechers (SKX – Analyst Report) getting kicked to the curb by over 35% after reporting sales growth of only 27%.

So it’s no wonder apparel investors have little tolerance for the struggles at a niche footwear maker like Crocs. Here’s what the company had to say about the quarter…

“We delivered third quarter sales in line with our revised expectations reflecting challenges in China and currency,” CEO Gregg Ribatt said in a statement. “Our China business is undergoing changes as we transition away from under-performing distributors.”

Related Posts

Deutsche Bank analysts see Bitcoin recovering to $28K by December

Deutsche Bank analysts see Bitcoin recovering to $28K by December Stock Exchange: Can Model-Based Trading Beat The Market?

Stock Exchange: Can Model-Based Trading Beat The Market?- Snoop Dogg revealed as co-founder of Web3-powered livestream platform

- Top-Five Buy/Strong Buy Upgrades – February 29, 2016

US Import, Export Prices Tumble For 2nd Month As China Deflation Exports Accelerate

US Import, Export Prices Tumble For 2nd Month As China Deflation Exports Accelerate- Mercado Bitcoin operator acquires Portuguese crypto exchange

Leave A Comment