I vividly remember my first desktop computer. It was a mighty machine powered by an AMD Athlon 800mhz processor with 64mb ram. As a true geek, I upgraded it several times and with respect to the graphics cards, there were only two choices at the turn of the century. You either went with AMD’s Radeon chips or NVIDIA’s GeForce range. My choice settled on a Radeon with 64mb; AMD was the underdog at the time, but their Radeon cards were top quality. It offered crisp pictures, and smooth gameplay, to support my career as online gamer in the Unreal Tournament clan The Viper’s Nest.

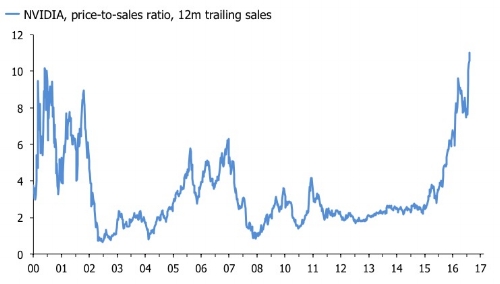

The world has moved on since then. I am no longer as adept with an Instagib rifle as I used to be, and NVIDIA no longer only relies on selling graphic chips. Today the firm is centre stage in the debate on whether U.S. tech stocks—and the infamous FANGs—are in a bubble. I concede that I don’t completely understand why investors have suddenly decided that NVIDIA is morphing into Skynet 2.0. But it appears to be something about offering AI data center services to the likes of Facebook, Amazon and Alibaba to store and train their AI algos. Cut through the Terminator references, and the story seems pretty simple. The FANGs are the big kids on the block, and NVIDIA has managed to create a service they want, or perhaps even one they need. That’s a good business model. Investors love it, and they are paying up. I had one of my agents on the buy side send me the latest bull-report from Citi. The bank’s bull case for NVIDIA is $300, a cool 100% upside from the current level. The chart below shows that NVIDA shares are trading hands at a price-to-sales ratio of a dizzying 11 times, slightly above the ding-dong highs immediately before the dot-com bubble burst.

This is ominous for momentum chasers, but not necessarily conclusive. Shorting a chart like the one above can be very bad for your financial health, at least in the near term. More generally, it is possible that NVIDIA’s drive into AI data centres is indeed the new black, but I am not sure that I want to pay 11 times trailing sales for the luxury of owning that story. Even tech firms with good businesses were destroyed when the tech bubble unravelled in 2000. The picture for the Nasdaq as a whole is more complicated. The index is expensive based on its own history. It currently trades at the same multiples as it did just before the 2008 crash. But first chart below shows that the index’ price-to-sales is also well below the lofty levels in 2001 before the denouement. If this is a repeat of anything close to the Dotcom surge, the Nasdaq has a lot further to run. On the other hand, if I run it through my trusty valuation score, the message is to steer well clear of adding exposure.

Leave A Comment