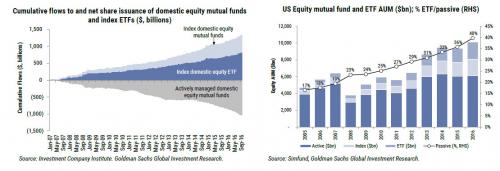

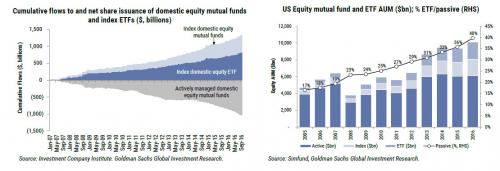

By now it is generally accepted that the primary source of fund inflows into stocks (aside from buybacks of course) are ETFs, the retail investor’s new favorite passive investing vehicle.

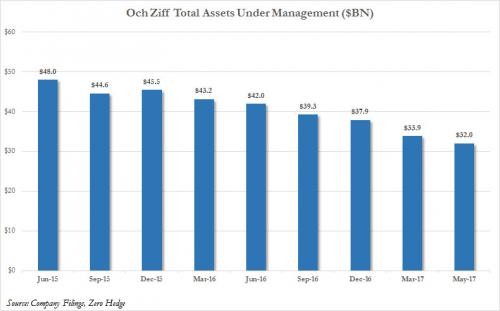

On the other side, are outflows from active managers – mutual and hedge funds – such as Och Ziff which as presented earlier today, suffered its biggest YTD redemptions and drop in AUM in history.

The underlying dynamics here are simple: institutional investors, whether voluntarily or because they are forced to through redemptions, are selling risk exposure to retail investors, something JPM observed two months ago in “Institutions, Hedge Funds Are Using The Rally To Sell To Retail.”

Overnight, Bank of America gave the latest confirmation that this dynamic is accelerating, when it reported that it had just observed the biggest institutional sales in nearly a year. Specifically, “last week, during which the S&P 500 rallied 1.5% amid optimism on tax reform that we think may signal the end of the “Trump put”, BofAML clients were net sellers of US equities for the second week, in the amount of $2.9bn.”

As BofA’s Jill Hall adds, “this was the largest net sale since two weeks prior to the Brexit vote in early June.” She further notes that clients sold both single stocks and ETFs (first ETF sales since mid-September 2016). Net sales were led by institutional clients, whose sales were the largest of any week since mid-Sept. 2015, and private clients were also net sellers for the first time in seven weeks…. Clients sold stocks across size segments, with small caps—where we recently turned bearish—seeing net sales for the first time in four weeks.

What did BofA’s clients sell? Pretty much everything, with an emphasis on taking profits: “Broad-based sales across all sectors except Utilities. Clients were broad-based net sellers of stocks across ten of the eleven sectors last week, with sales led by this year’s winners, Consumer Discretionary and Tech. Only Utilities saw net buying last week, similar to the prior week when only Utilities and Telecom saw

inflows. Tech continues to have the longest consecutive selling streak, with net sales for the last eight weeks, and sentiment remains the most persistently bearish within Health Care, where less-volatile four-week average flows have been negative since March of 2016. Year-to-date, Telecom is the only sector which has seen cumulative inflows, entirely due to private clients buying.”

Leave A Comment