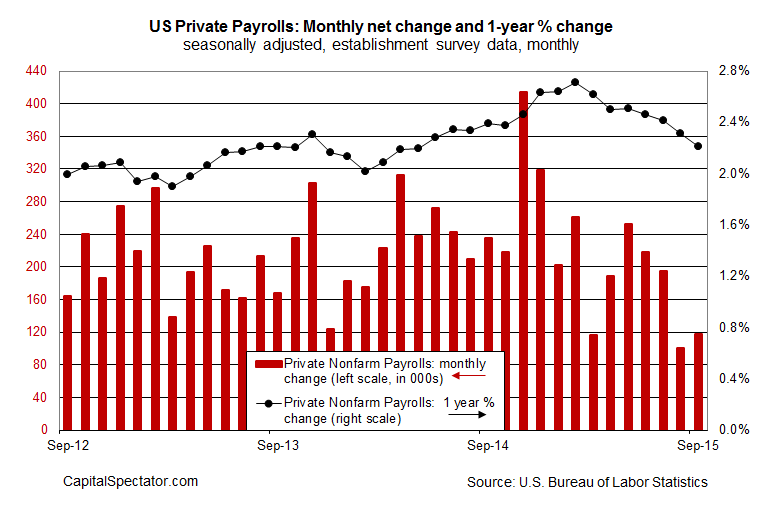

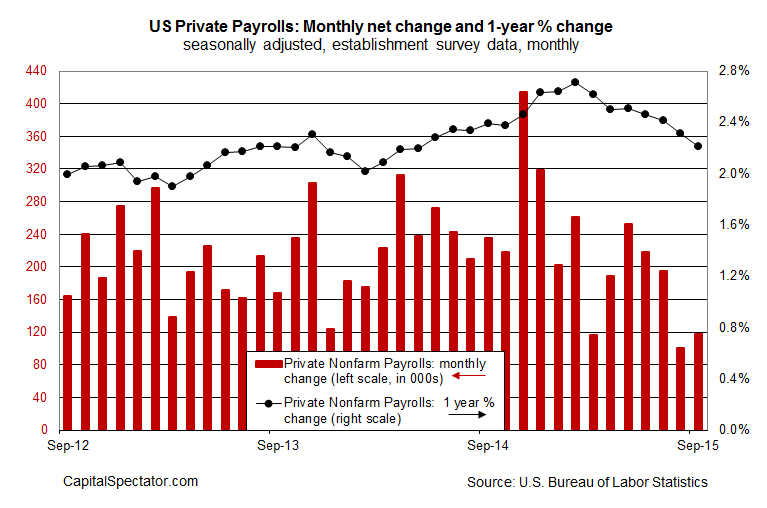

Today’s payrolls report from Washington is ugly. The crowd was expecting that today’s jobs report from the Labor Department would show that US companies added 200,000 positions in September. Instead, today’s release shows that private payrolls increased by a weak 118,000. The good news is that the year-over-year trend is still ahead by a solid 2.2% through last month. Unfortunately, the annual pace continues to decelerate. Does this add up to a recession signal for the US? No, not yet, but today’s update doesn’t help boost confidence that the worst will be avoided. As I’ve been discussing for the past month or so, macro risk for the US has been rising lately, even if it still falls short of a clear and reliable signal that the business cycle has turned negative (see here and here, for instance). Today’s employment report tips the scales a bit further toward a bearish outlook for the economy.

Monthly changes can be noisy, but it’s clear that the growth trend for US employment continues to slide. That’s a worrisome development and one that deserves close attention in the months ahead. The 2.21% rise in private employment last month vs. the year-earlier level is still a solid pace—if it holds. Unfortunately, the downside momentum of late suggests that even lesser rates of annual growth are coming. Meantime, last month’s year-over-year rise in private-sector jobs is the lowest gain since May 2014 and well below the cyclical peak of 2.71% in Feb. 2015.

Adding insult to injury, the initially reported August rise of 140,000 for private payrolls was revised sharply lower to a tepid 100,000 advance. As a result, the aggregate gain in private-sector employment for August and September is a soft 218,000—the smallest two-month increase in over three years.

Despite today’s disappointing numbers, September is unlikely to dispense a clear signal of a new recession for the US. The deceleration in growth for payrolls and other indicators certainly raise questions about how the macro trend will fare in the final quarter of the year. But for the moment, slower growth hasn’t crossed the line into recession, even if the risk of trouble is edging higher.

Related Posts

This Is The Biggest Risk To Amazon Stock

This Is The Biggest Risk To Amazon Stock Our S&P 500 Forecast Of 2125 Points Got Invalidated?

Our S&P 500 Forecast Of 2125 Points Got Invalidated?- WTI Crude Oil Pressured To The Downside

AUD/USD A Big Gainer – Is 0.80 In Play?

AUD/USD A Big Gainer – Is 0.80 In Play? ServiceNow Counting On AI And Natural Language For Growth

ServiceNow Counting On AI And Natural Language For Growth- Contrino Consulting: Revolutionising Formby’s Financial Service Landscape

Leave A Comment