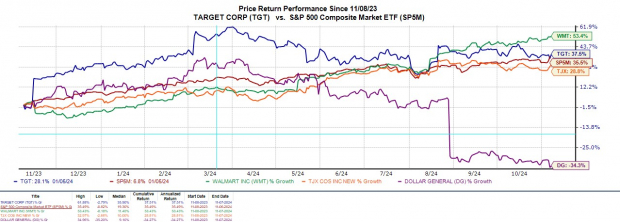

Making significant progress in addressing inventory concerns, Target’s (TGT) stock appears to be at a positive inflection point ahead of its Q3 results on Wednesday, November 20.Sporting a Zacks Rank #1 (Strong Buy) and landing the Bull of the Day, let’s take a look at why investing in Target looks favorable again. Targets Q3 ExpectationsBased on Zacks estimates, Target’s Q3 sales are projected to increase 2% to $25.97 billion. On the bottom line, Q3 EPS is expected to rise 8% to $2.28 versus $2.10 per share in the comparative quarter.Target most recently surpassed Q2 earnings expectations by nearly 19% in August with EPS at $2.57 compared to estimates of $2.16 a share. Notably, Target has surpassed the Zacks EPS Consensus in three of its last four quarterly reports posting an average earnings surprise of 20.26%.  Image Source: Zacks Investment Research Addressing Shrink ConcernsTarget has been at the forefront of addressing shrink concerns as theft and damaged goods have affected many retailers in recent years. To that point, Walmart (WMT), TJX Companies (TJX), and Dollar General (DG) are some of the other notable names that have dealt with the dismal effects of shrink.As reported by Yahoo Finance, Target has been a leader in increasing security measures by installing locking cases for items prone to theft while investing in additional security members and third-party training services.Target also plans to partner with the US Department of Homeland Security to develop cyber defense technology in a bid to curb organized retail crime. These efforts have largely attributed to Target’s increased probability considering shrink reduced its profit by an astonishing $1.2 billion in the last two years. Tracking Targets Rebound & ValuationBoosting investor sentiment by addressing its shrink issues, Target’s stock is up a modest +6% year to date but has now soared +37% over the last year. Edging the benchmark S&P 500’s one-year performance, Target has trailed Walmart’s +53% but has topped TJX’s +28% and Dollar General’s plummet of -34% .

Image Source: Zacks Investment Research Addressing Shrink ConcernsTarget has been at the forefront of addressing shrink concerns as theft and damaged goods have affected many retailers in recent years. To that point, Walmart (WMT), TJX Companies (TJX), and Dollar General (DG) are some of the other notable names that have dealt with the dismal effects of shrink.As reported by Yahoo Finance, Target has been a leader in increasing security measures by installing locking cases for items prone to theft while investing in additional security members and third-party training services.Target also plans to partner with the US Department of Homeland Security to develop cyber defense technology in a bid to curb organized retail crime. These efforts have largely attributed to Target’s increased probability considering shrink reduced its profit by an astonishing $1.2 billion in the last two years. Tracking Targets Rebound & ValuationBoosting investor sentiment by addressing its shrink issues, Target’s stock is up a modest +6% year to date but has now soared +37% over the last year. Edging the benchmark S&P 500’s one-year performance, Target has trailed Walmart’s +53% but has topped TJX’s +28% and Dollar General’s plummet of -34% .  Image Source: Zacks Investment ResearchMost intriguing, is that TGT trades at 15.4X forward earnings which is a pleasant discount to the S&P 500’s 25.1X and Walmart’s 34.2X.Magnifying this perceived discount is that Target’s annual earnings are forecasted to increase 7% in its current fiscal 2025 and are projected to climb another 11% in FY26 to $10.56 per share.It’s also noteworthy that TGT trades at just 0.6X sales with its top line expected to be virtually flat in FY25 but slated to increase 3% in FY26 to $110.27 billion.

Image Source: Zacks Investment ResearchMost intriguing, is that TGT trades at 15.4X forward earnings which is a pleasant discount to the S&P 500’s 25.1X and Walmart’s 34.2X.Magnifying this perceived discount is that Target’s annual earnings are forecasted to increase 7% in its current fiscal 2025 and are projected to climb another 11% in FY26 to $10.56 per share.It’s also noteworthy that TGT trades at just 0.6X sales with its top line expected to be virtually flat in FY25 but slated to increase 3% in FY26 to $110.27 billion.  Image Source: Zacks Investment Research Bottom LineCorrelating with Target’s strong buy rating is that earnings estimate revisions have remained higher for FY25 and FY26. The Average Zacks Price target of $177.28 a share suggests 20% upside in TGT with Target checking an overall “A” VGM Zacks Style Scores grade for the combination of Value, Growth, and Momentum.More By This Author:Block Q3 Earnings Meet EstimatesQualcomm Q4 Earnings And Revenues Surpass Estimates3 Large-Cap Stocks To Buy As Earnings Approach: MELI, TM, QCOM

Image Source: Zacks Investment Research Bottom LineCorrelating with Target’s strong buy rating is that earnings estimate revisions have remained higher for FY25 and FY26. The Average Zacks Price target of $177.28 a share suggests 20% upside in TGT with Target checking an overall “A” VGM Zacks Style Scores grade for the combination of Value, Growth, and Momentum.More By This Author:Block Q3 Earnings Meet EstimatesQualcomm Q4 Earnings And Revenues Surpass Estimates3 Large-Cap Stocks To Buy As Earnings Approach: MELI, TM, QCOM

Related Posts

Morning Call For Friday, February 9

Morning Call For Friday, February 9- Goldman Is Troubled By The Fed’s Growing Warnings About High Asset Prices

The World’s Largest Retailer – Walmart, Will Release Its Earnings Today

The World’s Largest Retailer – Walmart, Will Release Its Earnings Today Netflix Increases Focus On Original Content

Netflix Increases Focus On Original Content September 2014 Business Inventories And Sales Growth Is Relatively Unchanged

September 2014 Business Inventories And Sales Growth Is Relatively Unchanged E

Trump Fail; Tourism Declines In USA

E

Trump Fail; Tourism Declines In USA

Leave A Comment