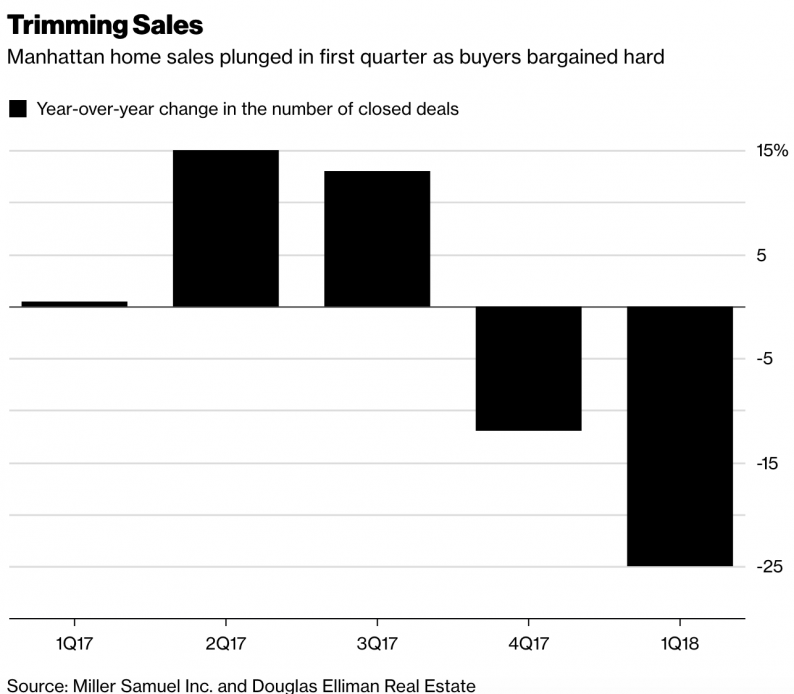

It’s not just in Canada’s most expensive markets that home sales are tumbling in 2018. A report today shows that from luxury condos to the least expensive co-ops in Manhattan, sales fell 25% year over year in Q1 2018 for the biggest annual decline since NYC’s property market froze during the 2009 financial crisis. Similar secular forces are at work in both countries: debt-maxed consumers, tighter lending standards, recent foreign speculation impediments, higher interest rates, aging owners looking to downsize expenses, and a lower US limit for mortgage interest deduction, are all working to slow sales volumes.

Declines in sales typically precede price by a few months.See:

The median price of all sales that closed in the quarter was $1.095 million, down 5.2 percent from a year earlier, brokerage Town Residential said in its own report. Three-bedroom apartments saw the biggest drop, with a decline of 7 percent to a median of $3.82 million, the firm said.

Neither new developments nor resales were spared from buyer apathy. Purchases of newly constructed condos, which continue to proliferate on the market, plummeted 54 percent in the quarter to 259, Miller Samuel and Douglas Elliman said. Sales of previously owned apartments dropped 18 percent to 1,921.

The plunge in transactions is actually a good thing, in that it may serve as a wake-up call for more sellers to scale back their price expectations.

Similar global trends connect in the abuse of debt-centric financial policies over the past decade as covered this month by the UK’s Financial Times, in the article “How the financial crash made our cities unaffordable”:

“Over the past 10 years, the life-cycles of global cities such as London New York and Sydney [as well as the most populous Canadian cities] start to look very similar.They begin with central banks cutting rates; then foreign buyers are welcomed in, prices go up, high-end homes are built, capital appreciation drops and then cities are left with a lot of stock which is too expensive to sell.”

Related Posts

Five High Dividend Stocks To Survive Volatile Markets

Five High Dividend Stocks To Survive Volatile Markets- USD/JPY Forecast Sept. 24-28 – Will The Fed Send It Even Higher?

- Endaoment raises $7M for nonprofits in its first year as crypto donations thrive

- Divergence: First Fed Rate Hike In 8 Years

Has Amazon Destroyed Best Buy’s Business?

Has Amazon Destroyed Best Buy’s Business? Binance Australia offices reportedly searched by local regulator

Binance Australia offices reportedly searched by local regulator

Leave A Comment