Photo Credit: Matthew Keys

Netflix, Inc. (NFLX) Consumer Discretionary – Internet & Catalog Retail | Reports January 19, After Market Closes

Key Takeaways

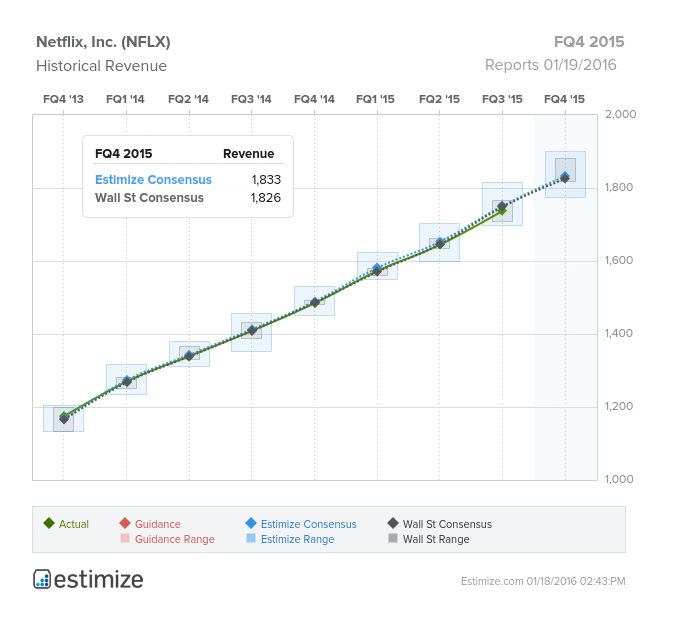

Netflix’s upcoming earnings report this Friday may be more exciting than its newest series “Making a Murderer”. Following an impressive 2015, with share prices rising a resounding 130%, analysts have begun to suspect the video streaming service is destined for slower growth. Netflix’s domestic subscription growth saw a surprising slowdown in Q4 2015 as competitors, Amazon Instant Video and Hulu began to establish their foothold in video streaming. If the fears prove to be true and Netflix delivers disappointing earnings, share prices could experience a sharp decline leading analysts to reevaluate their expectations of FANG stocks. On the other hand, if the company reports well, share prices could surge as Netflix will be viewed as a safe stock through what is expected to be a volatile year for the markets. The Estimize community expects EPS of $0.04 and revenue of $1.833 billion for Netflix’s earnings reports, slightly higher than the Wall Street consensus. Compared to Q4 2014, this represents a decline in EPS of 55% while revenue will have increased 24%. In fact, Netflix’s revenue has consistently improved quarter over quarter for each of the past 8 quarters, insisting more room to grow.

Just ahead of their Q4 2015 earnings, Netflix announced its entry into 130 international markets, including major countries like India and Russia. A key strength for Netflix is its strong market position which provides them with a competitive advantage over their peers. Prior to the recent announcement, the video streaming service had reached 60 million members in approximately 50 countries worldwide. By broadening their global reach, Netflix creates a new market with the opportunity to generate new subscriptions and bolster revenue growth. That being said, Netflix has already established itself in most of the lucrative markets around the world. Hence, its success elsewhere, while not guaranteed, will come with increasing content acquisition costs and lower operating margins than they have been accustomed to. Furthermore, Netflix faces stiffer competition as networks transition to digital streaming services. Over the past couple years, prominent networks like HBO, Starz and Showtime have launched streaming services while Amazon and Hulu continue to entrench themselves. Netflix has been able to weather this storm, particularly with the help of exclusive Netflix series. Despite some skepticism, Netflix’s track record and unprecedented growth have justified a “buy” rating for the stock.

Leave A Comment