The biggest risk to the bond bear case, that expressed by Bill Gross, Jeffrey Gundlach, and Ray Dalio, is, ironically, stocks. Convention has it that rising interest rates are bad for them, but what are falling stock prices for UST’s? Historically speaking, the introduction of risk and even liquidations is bond positive.

When the last jobs report came out, Bill Gross immediately claimed the 10-year yield should shoot up to 3% and trigger the big bond rout everyone has been waiting ten years for. In that time, yields are lower (particularly in Germany) and the inflation hysteria that was blamed for the last stock market stumble has itself been left in limbo, in some places more thoroughly erased. Yet, stocks are stumbling again.

Inflation expectations in the US as well as Europe have faded over the past few weeks, so the case for the BOND ROUT!!!! has softened significantly. That has left the mainstream to reach for the trade war as a possible explanation. This one’s perfect for this sort of commentary, to blame a selloff on prospects for negative economic pressures even though the last one was supposed to be because things were getting too good (inflation).

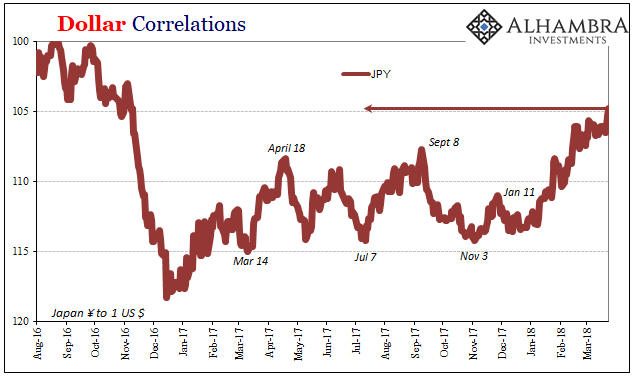

Maybe instead it has nothing to do with inflation or tariffs. The biggest problem for the bond bears may just be Japan.

Related Posts

WTI/RBOB Spike After Smaller Than Expected Crude Build, New Record High Production

WTI/RBOB Spike After Smaller Than Expected Crude Build, New Record High Production Terra contagion leads to 80%+ decline in DeFi protocols associated with UST

Terra contagion leads to 80%+ decline in DeFi protocols associated with UST Outline Of American Funds Washington Mutual A Fund (AWSHX)

Outline Of American Funds Washington Mutual A Fund (AWSHX)- The UK Was The Best Part Of The European Union

- Preview For June NFPs & Outlook For USD-pairs

- Qorvo Beats Q3 Earnings Estimates, Misses On Revenue

Leave A Comment