High-level distillation of the drivers of selected currencies.

US Dollar

Jobs data ahead of the weekend should recover after a storm depressed the September jobs growth. The base effect will allow earnings to show a strong year-over-year gain.

The FOMC meets next week. A 25 bp rate hike in December remains the most likely scenario despite the heightened volatility in the stock market. With the effective Fed funds rate hitting the level of interest on reserves, there is scope for a new technical adjustment. It is possible, but seems unlikely, that the Fed would end the unwinding of its balance sheet.

The most likely results of the mid-term election, according to tracking polls is for the Republicans to retain control of the Senate and the Democrats to secure a majority in the House of Representatives. It may not be an important near-term market factor.

The US dollar rose against all the major currencies in October but the Japanese yen. (around JPY113.15 puts the dollar down about 0.5% against the yen). At 97.00, the Dollar Index gained nearly 2% on the month, its best showing since May. The dollar appreciated against most emerging market currencies, but Argentina (~12.4%) and Turkey (~10.3%) staged recoveries, and investors were encouraged by the political developments in Brazil (~9.5%). Other Latam currencies led the declines with Chile (~-5.3%), Mexico (~-6.8%), and Colombia (-7.4%).

Euro

Growth slowed to 0.2% in Q3 after 0.4% expansions in Q1 and Q2. In 2017, the eurozone economy grew consistently at 0.7%.

Inflation ticked up in October, with the headline rate edging up to 2.2% from 2.1%. Half of EMU’s inflation is coming from food and energy. The core rate rose 1.1% from a year ago after a 0.9% pace in September. Core goods prices rose 0.14%, and core service prices rose 0.19%.

Merkel’s decision not to continue as CDU head and pre-announce no intention to seek re-election as Chancellor, nor an EU post, is significant even if the market impact is minimal. The next key development will be the CDU convention in December to choose a successor as party leader.

The euro fell roughly 2.2% in October. It is the second largest monthly decline this year after May’s 3.2% fall. It is near the year’s low set in mid-August near $1.13. We look for lower levels, and our near-term target is a little below $1.12. The recent decline has left technical indicators stretched, but we anticipate corrections to be capped now in front of $1.15.

Futureverse co-founders launch $50M venture fund

Futureverse co-founders launch $50M venture fund August 2018 Headline New Home Growth Improves

August 2018 Headline New Home Growth Improves USD/CAD Cup And Handle Formation On Intraday Charts

USD/CAD Cup And Handle Formation On Intraday Charts Bulls Wrest Back Control Of Market Direction, Despite Global Adversity

Bulls Wrest Back Control Of Market Direction, Despite Global Adversity Homebuilder Stocks Hit Record High As Homebuilder Confidence Plunges To 8-Month Lows

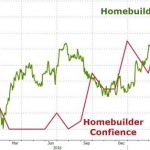

Homebuilder Stocks Hit Record High As Homebuilder Confidence Plunges To 8-Month Lows

Leave A Comment