When historians sort out this era of once-a-decade financial bubbles, they’ll marvel at how dissimilar the drivers of each boom were. The junk bonds of the 1980s were essentially leveraged tools for extracting wealth from companies. The dot-coms of the 1990s were vehicles for exotic new technologies and untested business models. The sub-prime mortgages and credit default swaps of the 2000s were semi-fraudulent fee-generation schemes.

All, in retrospect, were strange, unsteady foundations on which to build a global economy. But they look positively sane compared to the pillars of the current expansion: China and fracking.

As the true extent of China’s debt binge becomes apparent, the only reasonable reaction is awe. To cook the story down to its essence, the world’s biggest developing country decided to become developed in the space of a few years, borrowing nearly as much money as the entire rest of the world and using the proceeds to buy up every conceivable kind of industrial commodity. The result was a natural resources boom that, for a little while, floated the global economy on a rising tide of leverage. For much more detail, see this long Zero Hedge analysis.

Then, as all debt binges eventually do, this one ended in a tangle of malinvestment and evaporating cash flows. China’s excess capacity in basic industries like steel and cement is now epic. Mass layoffs are being announced daily. Its velocity of money — a measure of the tempo of economic activity — is the lowest in the world. And external trade is collapsing, with February imports and exports falling 13.8% and 25.4%, respectively.

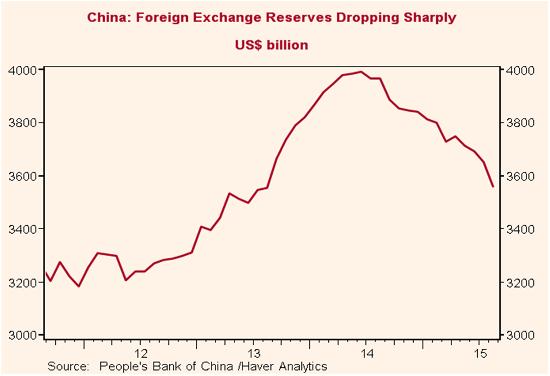

Now in damage control mode, China is spending its foreign exchange reserves in a probably-futile attempt to keep its currency from plunging, while capital is pouring out of the country in search of safe havens and hedge funds are placing billion-dollar bets on a big yuan devaluation.

China, in short, has become a drag on the global economy rather than its savior. And much, much worse is coming.

Leave A Comment