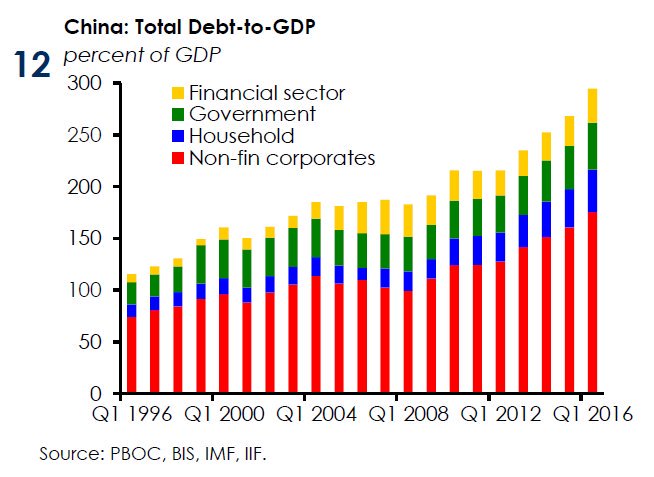

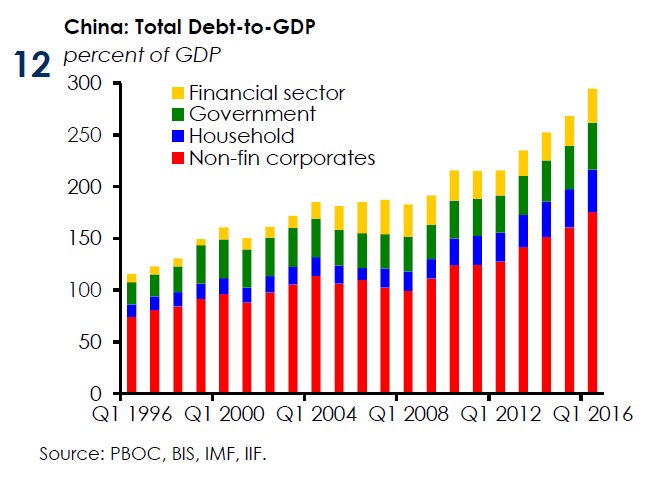

It’s a well-known risk, perhaps the biggest to the global financial system: China’s debt is too high, with estimates ranging from 250% to 300% of GDP per the IIF:

And while China has largely ignored, or avoided, discussing the troubling implications of its unprecedented debt load, this changed today when the head of China’s central bank, Zhou Xiachuan finally admitted that it has a debt “problem” saying that corporate debt levels are too high and that “it will take time to bring them down to more manageable levels”, underlining what has become the defining battle to put the world’s second-largest economy on a more sustainable footing: keeping GDP growing at 6.5% (or above) while injecting trillions in new debt.

“Non-financial corporate leverage is too high,” PBOC Governor Zhou Xiaochuan told reporters at a news conference on the sidelines of the annual parliament session.

Quoted by Reuters, he said that efforts will be made to contain debt levels, including restructuring of firms with heavy debt burdens, alongside a push to reduce excess industrial capacity.Furthermore, banks will withdraw support for financially unviable firms, he added, repeating pledges by other officials last year to drive such “zombie” firms out of the market.

“I personally think this process is relatively medium-term. It won’t have very obvious results in the short-term because the existing stock (of debt) is very large,” he said.

Zhou Xiaochuan, Governor of the People’s Bank of China, attends a news

conference in Beijing China March 10, 2017. REUTERS/Jason Lee

Zhou also said that measures by local governments to cool rising house prices will slow mortgage growth to some degree, but housing loans will continue to grow at a relatively rapid pace. We profiled China’s mortgage debt problem last October when we showed that over 70% of all new loans went to fund mortgages, which in turn now account for a fifth of total Chinese outstanding loans.

Related Posts

The Safety Net: Expect Another Cut To This 7.8% Yield

The Safety Net: Expect Another Cut To This 7.8% Yield Elliott Wave Technical Forecast: Unlocking ASX Trading Success: CSL Limited

Elliott Wave Technical Forecast: Unlocking ASX Trading Success: CSL Limited Coffee and Culinary Innovation: How Chefs Infuse Coffee into Savory Dishes, Sauces and Cocktails

Coffee and Culinary Innovation: How Chefs Infuse Coffee into Savory Dishes, Sauces and Cocktails The Shale Oil Bubble

The Shale Oil Bubble Dollar Dropped Like Hot Potato After Core CPI Disappointed

Dollar Dropped Like Hot Potato After Core CPI Disappointed Blockchain Founders Fund raises $75M to encourage Web3 mass adoption

Blockchain Founders Fund raises $75M to encourage Web3 mass adoption

Leave A Comment