With investor attention increasingly focused on China’s credit pipeline to see if the recent crackdown on shadow lending has unlocked other sources of debt in a country where growth is always and only a credit phenomenon, and where both the housing and auto sectors are suddenly reeling, overnight’s latest credit data from the PBOC was closely scrutinized… and left China watchers with a very bitter taste.

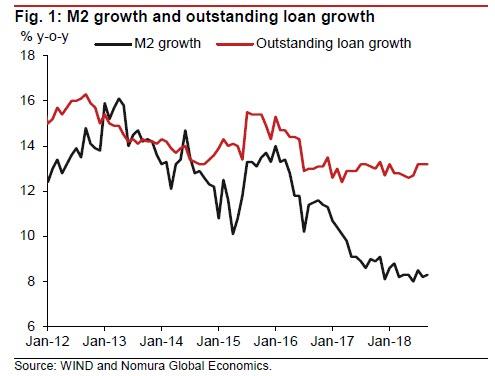

What it showed was that traditional new RMB loans rose to RMB1,380bn in September, largely as expected (exp RMB1,360bn) from RMB1,280bn in August, with the growth of outstanding loans unchanged at 13.2% Y/Y and up from 12.7% a year ago. New loans to the corporate sector rose to RMB677bn from RMB613bn in August, in which medium- to long-term loans rose to RMB380bn from RMB343bn in August. New loans to the household sector rose slightly to RMB754bn in September from RMB701bn in August, and the long-term loan component (mostly mortgage loans) remained largely flat at RMB431bn (August: RMB442bn). New loans to non-bank financial institutions were -RMB60bn in September versus -RMB44bn in August (average September level: RMB13bn). Also of note, M2 growth rose by 0.1% to 8.3% Y/Y in September, in line with market expectations, however as Nomura writes in a note this morning, monetary aggregate growth is no longer as important to the central bank’s policymaking as it once was, and Beijing is focusing more on interbank liquidity conditions, aggregate financing and investment.

Where the data was especially interesting, however, was in the broader Total Social Financing category, which on the surface came in well stronger than expected printing at RMB2,205bn in September from RMB1,929bn in August, above the $1,550bn estimate, and the strongest month since January.

However, this being China, there was as usual a big footnote with this latest credit data: starting this month, the PBoC further adjusted its definition of aggregate financing by including net financing through local government special bond issuance – just two months after it added asset-backed securities (ABS) and non-performing loan write-offs into this measure – and the same LGFV source of debt which yesterday S&P said could contain as much as $5.8 trillion in off-balance sheet debt.

Leave A Comment