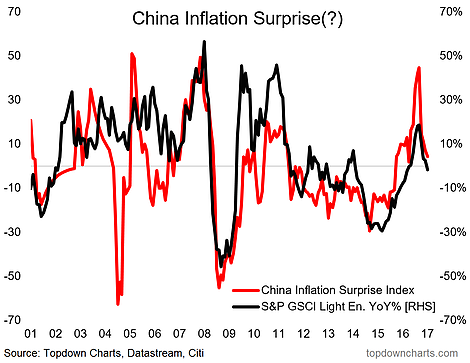

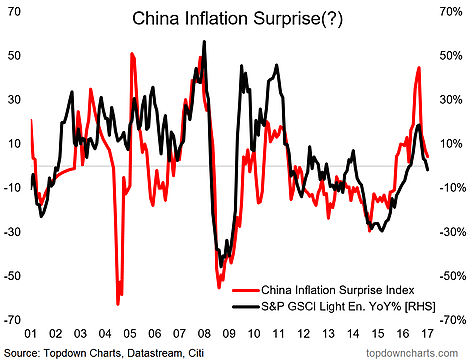

The latest inflation figures out of China weren’t much to talk about on the face of it, with CPI at 1.5% yoy in June and PPI at 5.5% – both unchanged from June and more or less in line with expectations. But what is notable, besides the persistent underlying inflation pressures we’re seeing, is the way producer prices have been rocked around by commodities. The following two charts help put it in context. The first shows how the surge in China’s inflation surprise index had a big helping hand from commodities (although I would also note that most had been too negative on China last year – at a time when we were optimistic on the cyclical outlook due to stimulus and property).

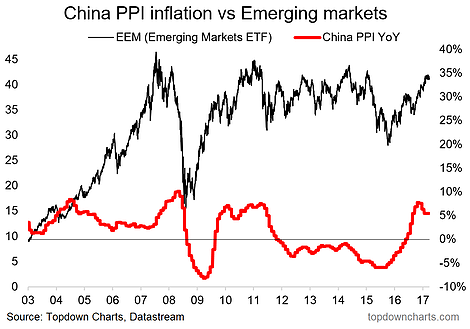

The second shows the apparent link between China PPI and emerging market equities. There is a fairly logical link there because there is a significant portion of EM economies that are commodity-sensitive. The other point is China is a big consumer and driver of commodity prices, so rising commodity prices often reflect generally better cyclical conditions in China – which get reflected in Chinese equities and Chinese demand for other inputs and finished products. The main point is that when PPI is in deflation it tends to be negative EM and vice versa. Just one factor, but one that captures a lot of important drivers.

China’s inflation surprise index surged on the back of rebounding commodity prices and overly pessimistic sentiment on the outlook for China’s economy.

Chinese PPI inflation (or deflation) provides an important signal when thinking about emerging market equities. It captures a couple of key drivers, and the main rule of thumb is that positive PPI inflation is generally supportive for emerging markets.

Related Posts

USD/CAD Forex Elliott Wave Technical Analysis – Wednesday, May 29

USD/CAD Forex Elliott Wave Technical Analysis – Wednesday, May 29 Robert Samuelson Is Unhappy That We Have Evidence Based Economics

Robert Samuelson Is Unhappy That We Have Evidence Based Economics To Hike Or Not To Hike-Is That Really The Question To Ask?

To Hike Or Not To Hike-Is That Really The Question To Ask?- China Promises To Support Yuan At G20 Meeting

Copper Is The One Metal You Can’t Ignore

Copper Is The One Metal You Can’t Ignore- Trace One to Launch Audit-Driven QMS

Leave A Comment