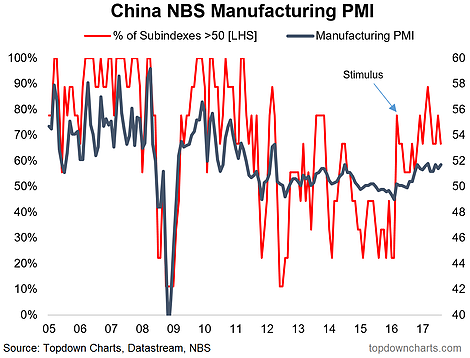

The August round of official PMI data from China showed some mixed signals, and a little bit of something for everyone, but overall a signal of steady as it goes for now. The manufacturing PMI was up +0.3 to 51.7 while the non-manufacturing PMI was down -1.1 to 53.4 with the breakdown: Service index -0.5 to 52.6 and Construction -4.5 to 58 – which is interesting given our call on the Chinese property market. Within the manufacturing PMI it was the SOEs in the lead at -0.1 to 52.8 and medium sized +1.4 to 51.0 and small +0.2 to 49.1 – notable that the uptick on a headline basis was driven by medium sized manufacturers.

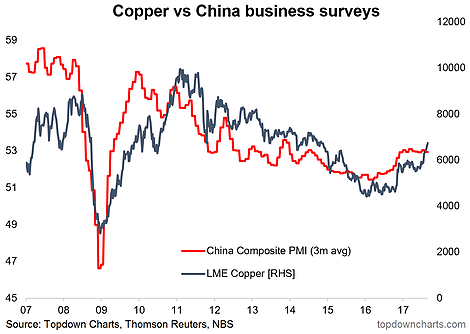

The rolling 3 month combined metric (a key signal I track) was down -0.1 to 52.9 – but really basically unchanged, and still locked in the circa-53 range it has been in since the start of the year… which really is the best consistent run China’s economy has had on this measure since 2011, and represents a significant turnaround from 2015/16. So overall it’s a mildly positive story for China’s economy right now. But as previously noted, I expect the headwinds to come back in 2017. So when you see Copper running ahead of the combined PMI you have to wonder who’s “right”…

Copper is running ahead of the combined China PMI – makes you wonder which one is “right”.

Manufacturing PMI breadth has tapered off somewhat while the headline index has hit a plateau. Stronger global trade, a weaker currency, and domestic stimulus are short-term supportive forces.

Related Posts

Are Foreign Investors Done Selling Japanese Equities?

Are Foreign Investors Done Selling Japanese Equities? Peer-to-peer ecosystem champions censorship resistance with new features

Peer-to-peer ecosystem champions censorship resistance with new features Demand Slides For 2Y Treasuries As Yield Surges To Highest Since Sept 2008

Demand Slides For 2Y Treasuries As Yield Surges To Highest Since Sept 2008- Trump Tariffs Crush Small Businesses: “We Are At The Limit”, Optimism Sinks

Revisiting The Margin Of Safety: The IW Box

Revisiting The Margin Of Safety: The IW Box- The Secret To Predicting Oil Prices – And Cutting Through The “Expert” Hype

Leave A Comment