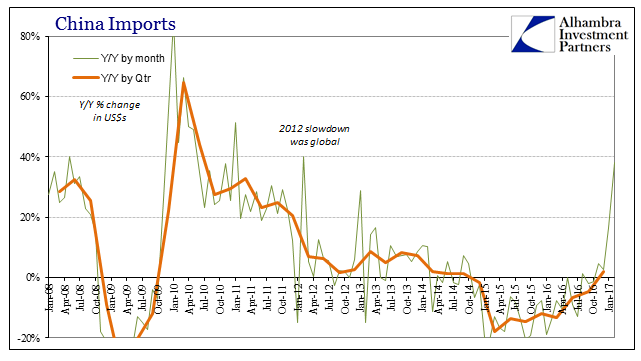

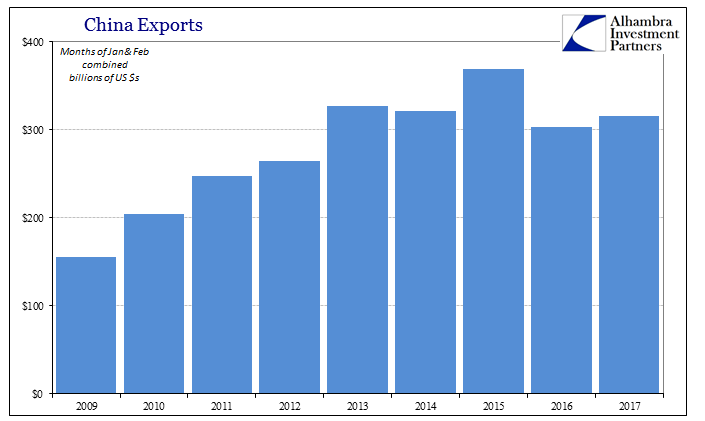

Chinese trade figures for the month of February 2017 were decidedly mixed. On the import side, total trade rose by 38.1% from February 2016. That latter month, however, was one of the lowest trade figures in years (the first time imports had added up to less than $100 billion in any month going back to February 2010) as it ended up with both the worst of the “rising dollar” conditions as well as holding last year’s Lunar New Year holiday. For January and February combined, imports were 26% higher than the same two months in 2016, but still 16% below January and February 2014.

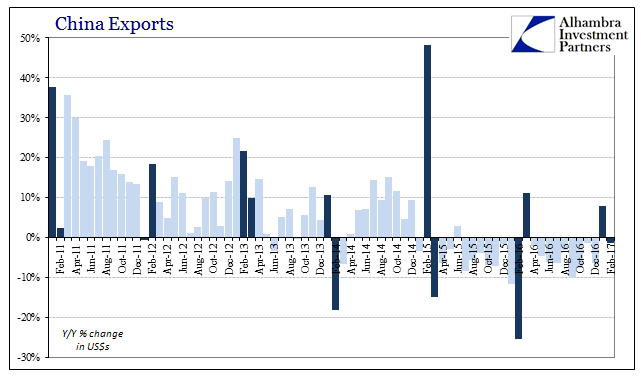

Chinese exports, on the other hand, contracted yet again. Though “analysts” were projecting a 14% gain for the month, exports totaled $124.5 billion, down 1.3% from one of the worst months in China’s statistics. That is why expectations were for a seemingly robust gain, as base effects made it improbable that exports would be lower in February 2017 than in February 2016. Calendar effects being what they were, however, January and February combined this year were up just 4% compared to last year during the worst economic conditions since the depths of the Great “Recession.”

It doesn’t exactly provide the comparisons “reflation” was hoping for, particularly in terms of exports which are the best proxy for global trade and therefore “demand.” As with US trade and its economic accounts, conditions are clearly not getting worse. The contraction appears to have been stopped but giving way to the same sort of lackluster pace of activity as had prevailed before it started. Even the import figures when placed into the context of the nearly 3-year slump aren’t as cheerful as they appear.

In the first months out of the Great “Recession”, for example, imports stopped contracting in October 2009 and within two months, by that December, they were up 56% year-over-year. In January 2010, with another Golden Week calendar effect similar to 2016’s, imports jumped by 86%. These rates were achieved with conditions that were strikingly similar in China to those of early 2016 – enormous fiscal and monetary “stimulus” introduced during a contraction which at its worst in Chinese trade wasn’t that much greater than at the worst in 2015-16.

Related Posts

Circle co-founder says converged dollar books on Binance would be good for USDC

Circle co-founder says converged dollar books on Binance would be good for USDC 70% Of Fund Managers Say The Economy Is Late Cycle

70% Of Fund Managers Say The Economy Is Late Cycle Is This Why FANG Stocks Rebounded This Morning?

Is This Why FANG Stocks Rebounded This Morning? Snap, Inc. Stock Upgraded By One Firm, Another Asks If It’s The Next FB Or TWTR

Snap, Inc. Stock Upgraded By One Firm, Another Asks If It’s The Next FB Or TWTR Weekly Unemployment Claims Unexpectedly Fell And Dow Hit Its Highest Level

Weekly Unemployment Claims Unexpectedly Fell And Dow Hit Its Highest Level- Is The Grass Getting Greener?

Leave A Comment