At the end of Friday, the Dow Jones (US30) Index added 0.04% (+1.61% for the week), while the S&P 500 (US500) Index fell 0.16% (+0.75% for the week). The NASDAQ Technology Index (US100) closed negative 0.18% (for the week +0.39%). Weakness in chip company stocks pressured the broader market on Friday, even as S&P US PMI reports showed that the US economy continues to grow. The S&P US Manufacturing PMI for June unexpectedly rose 0.4 to 51.7, stronger than expectations of a decline to 51.0. In addition, the S&P Services PMI for June unexpectedly rose 0.3 to a two-year high of 55.1, stronger than expectations for a decline to 54.0. Stocks also declined as the quarterly expiration of options and futures occurred on Friday, prompting traders to roll over existing positions or open new ones. About $5.5 trillion of positions expired on Friday, according to options platform SpotGamma.Equity markets in Europe were mostly down on Friday. Germany’s DAX (DE40) was down 0.50% (for the week +0.86%), France’s CAC 40 (FR40) decreased by 0.56% (for the week +1.19%), Spain’s IBEX 35 (ES35) lost 1.15% (for the week -0.03%), and the UK’s FTSE 100 (UK100) closed negative 0.42% (for the week +1.12%). The S&P Eurozone Manufacturing PMI for June unexpectedly fell by 1.7 to a 6-month low of 45.6, weaker than expectations of a rise to 47.9. The S&P Composite PMI for June unexpectedly fell by 1.4 to 50.8, weaker than expectations for a rise to 52.5.Friday’s dollar strength pressured commodity markets. WTI crude oil fell below $81 per barrel. Nevertheless, the market remains supported by geopolitical risks in the Middle East as Israeli forces moved further into the Gaza Strip and Yemeni Houthis carried out another attack on a ship in the Arabian Sea on June 24. Meanwhile, Israel and Lebanon’s Hezbollah stand on the brink of a new conflict. Ecuador’s state oil company, Petroecuador, also declared force majeure on some Napo heavy oil shipments due to the shutdown of a major pipeline and oil wells amid heavy rains. In addition, recent data points to a decline in US crude oil inventories amid a rebound in energy consumption.Asian markets were predominantly up last week. Japan’s Nikkei 225 (JP225) gained 0.40%, China’s FTSE China A50 (CHA50) fell by 1.22%, Hong Kong’s Hang Seng (HK50) gained 1.01%, and Australia’s ASX 200 (AU200) was positive 0.93%. Asian stock markets opened lower on Monday, reeling from weakness on Wall Street, as shares of Nvidia and other artificial intelligence chip makers saw heavy selling after strong gains.Singapore’s annual inflation rate for May 2024 rose to 3.1%, exceeding market forecasts of 3.0% and accelerating from April’s 2-year low of 2.7%. The annualized core inflation rate unexpectedly came in at 3.1%, the same as in the previous two months, beating the consensus forecast of 3.0%. Monthly, CPI rose by 0.7%, the highest since February, after rising 0.1% in April.The Australian dollar weakened below $0.665, extending recent losses as the US dollar rose on strong US business activity data that dampened expectations of an interest rate cut by the Federal Reserve. Investors are also cautiously awaiting Australian inflation data this week after the country’s central bank said it discussed the need for a rate hike at its June meeting and did not consider the case for a rate cut.S&P 500 (US500) 5,464.62 ?8.55 (?0.16%)Dow Jones (US30) 39,150.33 +15.57 (+0.04%)DAX (DE40) 18,163.52 ?90.66 (?0.50%)FTSE 100 (UK100) 8,237.72 ?34.74 (?0.42%)USD Index 105.83 +0.24 (+0.23%)Important events today:

More By This Author:Analytical Overview Of The Main Currency Pairs – Monday, June 24Dell And Nvidia Are Jointly Building An Artificial Intelligence Factory. SNB Cuts Rate For The Second Time In A Row Analytical Overview Of The Main Currency Pairs On Friday, June 21

Related Posts

Macy’s Announces 5,000 Job Cuts, Closure Of 7 More Stores; Stock Tumbles

Macy’s Announces 5,000 Job Cuts, Closure Of 7 More Stores; Stock Tumbles Nigeria’s Inflation Declines For Nine Consecutive Months

Nigeria’s Inflation Declines For Nine Consecutive Months- Get Stock Insurance With These 2 High-Yielders

EUR/USD: Balance Of Risks Into Next Week’s ECB

EUR/USD: Balance Of Risks Into Next Week’s ECB- Saudi Cash Reserves Drop To Lowest Level In 40 Months Amid Crude Carnage

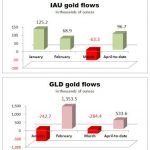

Gold ETFs Do Not Always Do The Same

Gold ETFs Do Not Always Do The Same

Leave A Comment