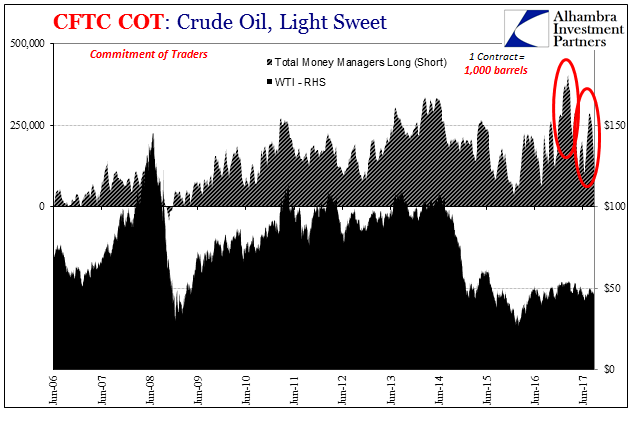

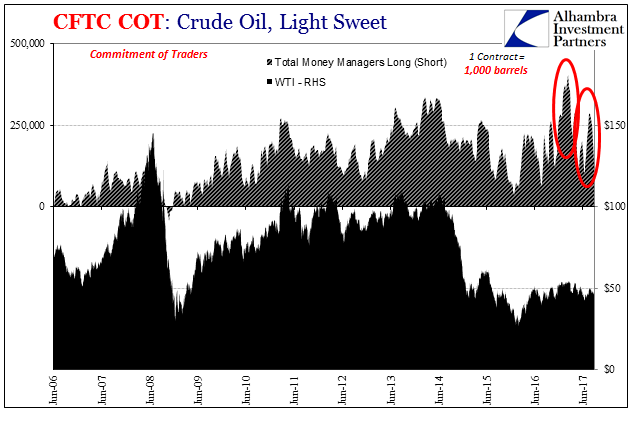

Over the past month, crude prices have been pinned in a range $50 to the high side and ~$46 at the low. In the futures market, the price of crude is usually set by the money managers (how net long they shift). As discussed before, there have been notable exceptions to this paradigm including some big ones this year.

It was earlier in February when money managers piled in to WTI longs, apparently expecting better things from “reflation.” It was perceived as such a sure thing that by the week of February 21the market was stretched at a record to that side. Oil prices did not follow, however, and then began to slide as managers rethought what might really be going on.

It happened again more recently though to a lesser extent. Triggered by copper, Draghi’s BOND ROUT!!!, or RMB (or some combination plus inventory drawdowns), money managers crowded long again in July. Still oil prices did not follow by all that much, staying at best in the range and often contradictorily with a downside bias.

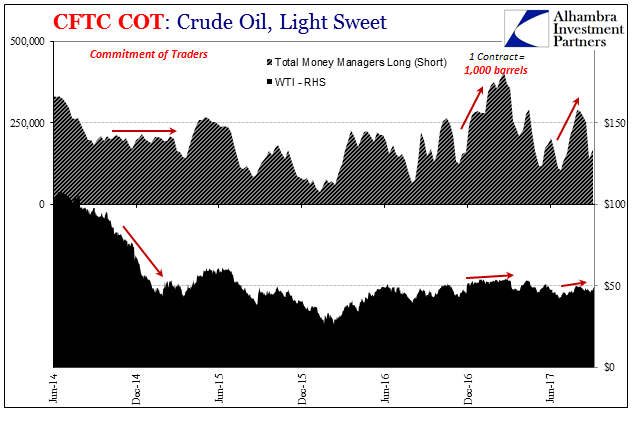

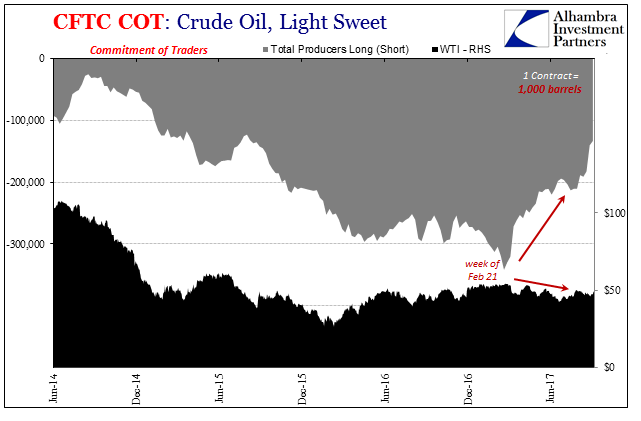

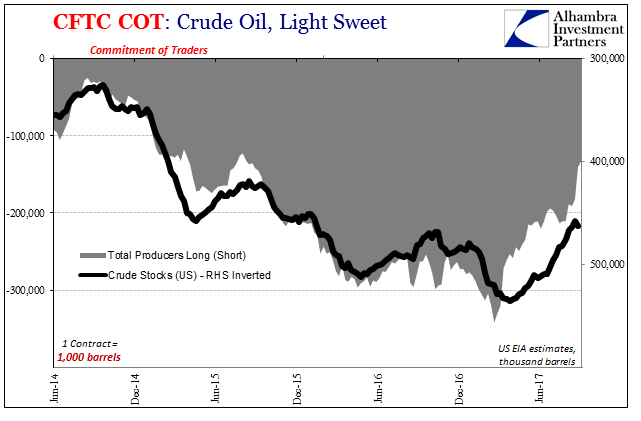

The reason was ironically the producer segment. The very players this market was meant to serve have since February used far less of it. They have literally fewer reasons to do so, as the need to short WTI in the futures market follows closely domestic crude inventory levels.

It has negated all that money manager enthusiasm; twice. Over the past month, inventories have continued to decline (though in the first week of September they rose likely as a hurricane effect), as has the aggregate net short position of producers. Money managers have become much less enthusiastic again, positioning oil futures market overall more pessimistically.

The difference isn’t all that large, however, with both dealers and “others” taking up some of the slack. That may account for the relatively narrow range in which WTI has traded since early August. The futures market during that time was mostly balanced if slightly more to the downside (indicated for price).

Leave A Comment