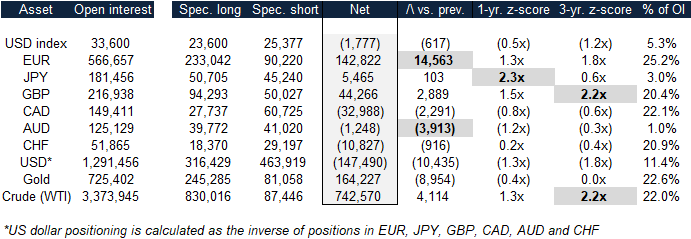

Relative to recent history, this week’s Commitments of Traders Report contains few notable changes. Looking at the data, the most significant moves include rising net long positions in the euro and falling net long positions in the Australian dollar. Changes in other currencies and commodities were relatively modest. On the bullish side, speculators continue to accumulate net long positions in the British pound. On the bearish side, the US dollar and commodity currencies (including the Canadian dollar) remain out of favor.

Turning to extremes in positioning, net long positions in the Japanese yen, the British pound and crude oil are looking fairly one-sided. This has been the case in recent history, and continues this week. Speculators have been chasing recent strength in the yen and the pound, while crude oil has been a consensus long position since late last year.

The purpose of this weekly report is to track how the consensus is positioned across various major currencies and commodities. When net long positions become crowded in either direction, we flag extended positioning as a risk. Crowded positions do not suggest an imminent reversal, but should be considered as a significant risk factor when investing in the same direction as the crowd. This is shown below:

CFTC COT speculator positions (futures & options combined) – April 10, 2018

Source: CFTC, MarketsNow

Notable extremes, significant changes in weekly positions, and large net positions as a proportion of open interest are highlighted above. Extremes in net positions are highlighted when speculator positioning is more than two standard deviations above trailing 1-year and 3-year averages. Weekly changes are highlighted when they are significant as a proportion of open interest. Finally, net positions as a proportion of outstanding interest are highlighted when they are large relative to historical averages. 1-year and 3-year z-scores are visually represented below:

1-year and 3-year z-scores based on net speculator positions

Leave A Comment