Image Source: Pixabay

Image Source: Pixabay

Asian stock markets are trading with mixed results on Thursday, following the uncertain signals from Wall Street overnight as META earnings failed to impress afterhours causing a late selloff. Traders are exercising caution as they await the report on first quarter US GDP data, which could potentially influence the outlook for interest rates. While the Fed is anticipated to maintain interest rates at next week’s US Fed monetary policy meeting, traders are keen to gather hints about the likelihood of future rate cuts.In the UK, the morning’s CBI distributive trades survey offers early insights into consumer trends this month. March’s retail sales balance hit a 10-month peak, signaling a promising sectoral outlook, although this month’s balance might taper slightly, possibly due to Easter’s early timing this year. Attention will likely turn to the UK GfK consumer confidence survey set for early release on Friday. With a recent upward trend, indicative of modest enhancements in consumer fundamentals amid peaking interest rates and real wage increments, another minor uptick to -20 is expected this month. This rise is bolstered by recent Budget tax cuts and ongoing inflationary retreat.Across the pond, today’s focal point lies in the initial assessment of US Q1 GDP growth. Last week’s robust March retail sales data, coupled with upward revisions to prior months, suggests another substantial GDP uptick. Anticipating a 2.5% annualized increase, matching consensus estimates, the surge primarily stems from continued robust consumer spending. However, weaker contributions from sectors like business investment and slowed inventory accumulation may dampen growth. Despite potentially marking the slowest quarterly growth rate in three quarters, it still exceeds most trend growth estimates, prompting Federal Reserve policymakers to maintain cautious optimism regarding interest rate adjustments.On Friday, the Bank of Japan unveils its latest monetary policy update, expected to maintain short-term interest rates within a 0%-0.1% range after exiting negative territory last month. Market focus centers on Governor Ueda’s guidance, with expectations for further rate hikes later in the year.

Overnight Newswire Updates of Note

(Sourced from Bloomberg, Reuters and other reliable financial news outlets)

FX Options Expiries For 10am New York Cut (1BLN+ represent larger expiries, more magnetic when trading within daily ATR)

CFTC Data As Of 19/04/24

Technical & Trade ViewsSP500 Bullish Above Bearish Below 5070

EURUSD Bullish Above Bearish Below 1.0720

EURUSD Bullish Above Bearish Below 1.0720

GBPUSD Bullish Above Bearish Below 1.24

GBPUSD Bullish Above Bearish Below 1.24

USDJPY Bullish Above Bearish Below 154.60

USDJPY Bullish Above Bearish Below 154.60

XAUUSD Bullish Above Bearish Below 2379

XAUUSD Bullish Above Bearish Below 2379

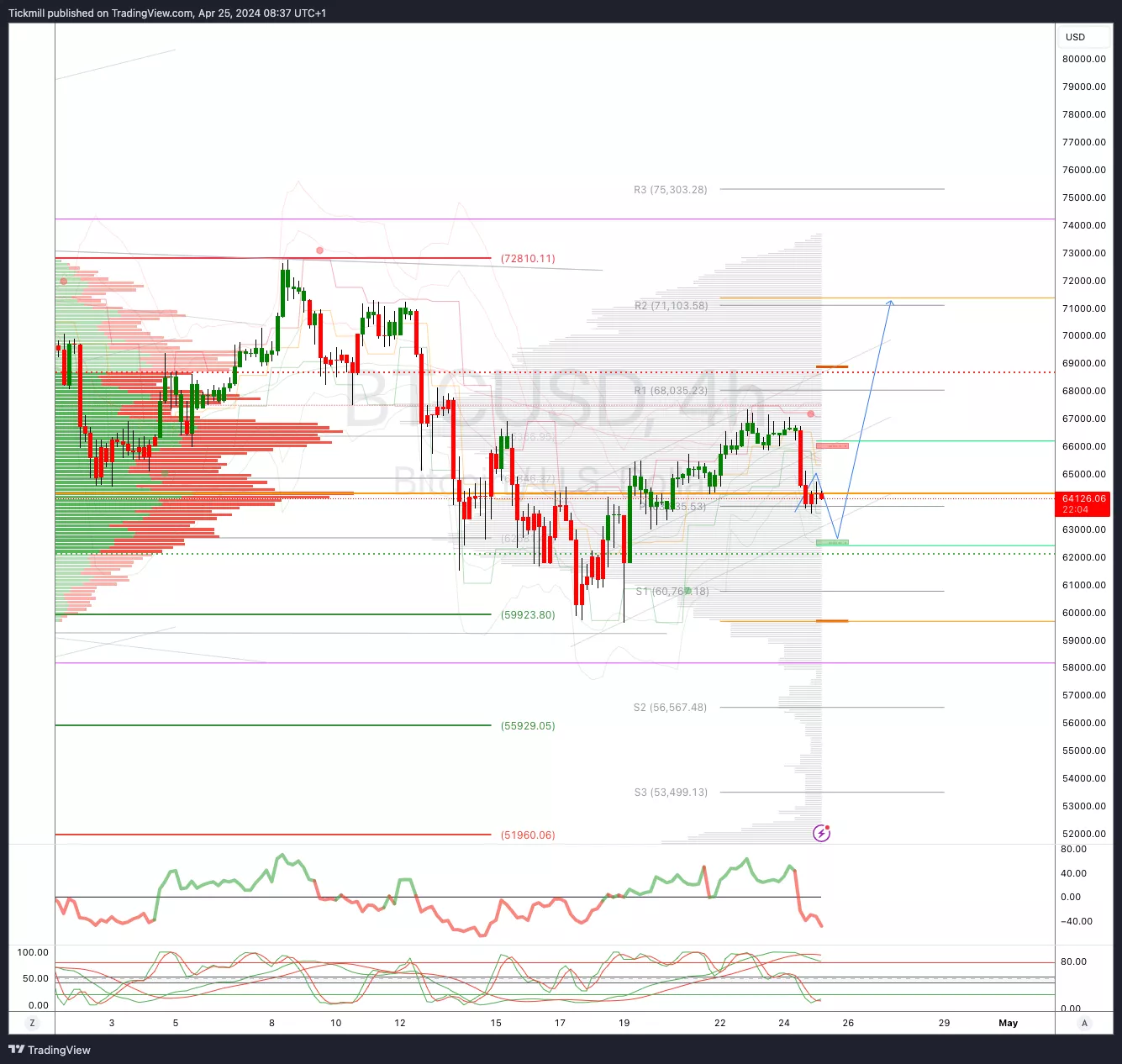

BTCUSD Bullish Above Bearish below 62000

BTCUSD Bullish Above Bearish below 62000

More By This Author:FTSE Finally Breaks Record Highs Before PausingDaily Market Outlook – Tuesday, April 23FTSE On The Front Foot As MIddle East Tensions Recede

More By This Author:FTSE Finally Breaks Record Highs Before PausingDaily Market Outlook – Tuesday, April 23FTSE On The Front Foot As MIddle East Tensions Recede

Related Posts

Negative Interest Rates Means Passive Capital Must Incur Huge Losses In A Crash Scenario

Negative Interest Rates Means Passive Capital Must Incur Huge Losses In A Crash Scenario Celsius denies allegations on Alex Mashinsky trying to flee US

Celsius denies allegations on Alex Mashinsky trying to flee US E

Comey’s Testimony, European Central Bank & U.K Snap Election May All Produce Greater Volatility This Week

E

Comey’s Testimony, European Central Bank & U.K Snap Election May All Produce Greater Volatility This Week- Industrial Metals Stock Outlook – November 2017

DeFi tokens book double-digit gains after Bitcoin rallies above $39,000

DeFi tokens book double-digit gains after Bitcoin rallies above $39,000- Sensex Ends Flat; ICICI Bank & SBI Top Gainers

Leave A Comment