Look at where multiples and rates were in 1999. I’m not saying stocks are screaming cheap, but you’re nowhere near an overheated market. Any comparisons to past overheated markets are ridiculous.

That’s what David Tepper told CNBC back in September and by God, he’s sticking with that assessment in the new year.

Who knows, maybe it’s not a great idea to question Tepper’s judgement. Recall the following from our buddy Kevin Muir, recounting the “Tepper Bottom“:

That worked out pretty goddamn well, so you know, who are we (or anyone else) to question the following from Tepper, who spoke to CNBC on Thursday:

Explain to me where this market is rich? It’s not rich with the tax thing that just changed earnings projections. With earnings forecasts going up and interest rates where they are, how is this market expensive? I don’t see the overvaluation. World growth is higher.

There’s no inflation. The market coming into this year doesn’t look rich, in fact, it looks almost as cheap as coming into last year.

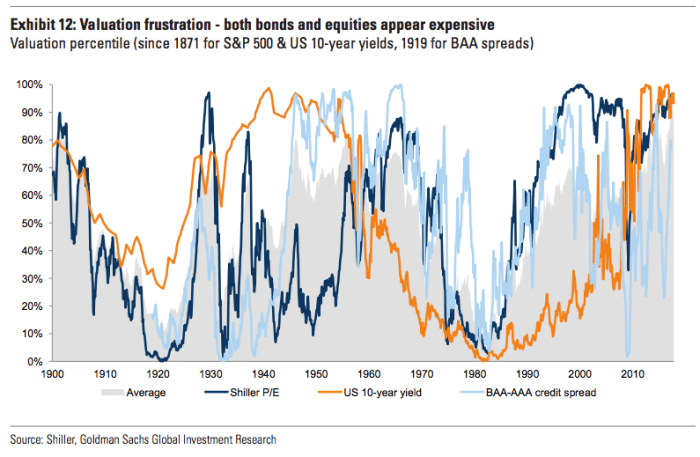

Ok. I mean, it doesn’t “look cheap.” Actually, it looks really – really – expensive. But remember, this is a world where “cheap” is a relative term. As Goldman will be happy to remind you, in absolute terms stocks, bonds, and credit haven’t been this simultaneously expensive in 100 years:

But relative to bonds, there’s still some “value” in equities – I guess. That’s what Tepper is going with. To wit, from the same interview:

The market can’t go down until the bond market gets hit.

Right. Everyone agrees with that. The question is how quickly and how violently do stocks react in a bond tantrum? That is, will there be enough time to get out or will Marko Kolanovic’s “quantitative exuberance” mean that when rates vol. finally does pick up (thanks probably to an uptick in inflation and the policy shock – i.e. aggressively hawkish central bank communication – that would almost invariably accompany that uptick), the systematic crowd will be forced to deleverage so quickly that everyone gets caught offsides?

Related Posts

Coca-Cola Names Brian Smith As President And COO, Effective January 1, 2019

Coca-Cola Names Brian Smith As President And COO, Effective January 1, 2019 IMF Sounds The Alarm On Global Debt, Warns “United States Stands Out”

IMF Sounds The Alarm On Global Debt, Warns “United States Stands Out”- Recapping The Fed Statement And Tax Reform

CAD: Has Peak Negative CAD Sentiment Been Reached? What’s The Trade? – Nomura

CAD: Has Peak Negative CAD Sentiment Been Reached? What’s The Trade? – Nomura Above The 40 – Stock Market Stasis

Above The 40 – Stock Market Stasis- US Mid-Term Elections Dominate Price Action In All Markets

Leave A Comment