The entire status quo is based on the delusion that rapidly rising debt will never generate any negative consequences.

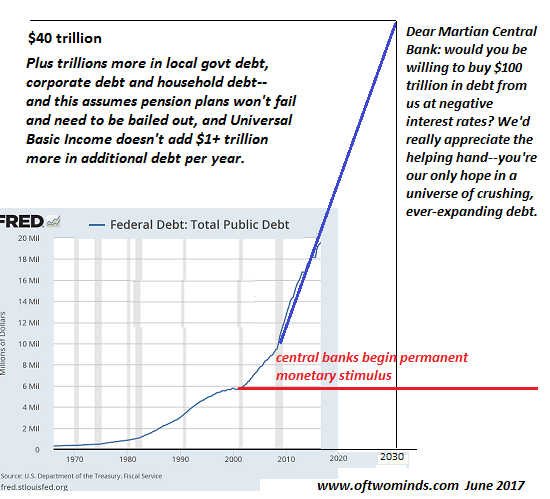

Here’s a chart of America’s national debt, extended a mere dozen years into the future: the current $20 trillion in debt will double to $40 trillion, and that assumes 1) trillions of dollars in private and local government pensions don’t implode and have to be bailed out by the federal government, a bail-out that will have to be paid by borrowing more money, 2) a recession doesn’t slash federal tax revenues, 3) Universal Basic Income (UBI) doesn’t become policy, adding $1+ trillion in additional borrowing annually–and so on.

Color me skeptical that doubling the debt in 12 years won’t have any negative consequences. Let’s start by noting that federal debt is only the tip of America’s total debt load, which is rising fast in all sectors: federal, state/county/city, corporate and household.

Total government, corporate and household debt soared from $15.5 trillion in 2000 to $41.1 trillion in 2016. (see chart below, courtesy of 720Global). If we extend this expansion another 12 years, we will have a total debt load in the neighborhood of $100 trillion by 2030. And that’s if the “recovery” news is all good.

The consensus is that all this debt will have no negative consequences because 1) interest rates will remain near-zero forever and 2) it’s all “investment”, right? Actually, no; the vast majority of this debt is consumption, not investment, or even worse, it simply services existing debt or funds speculative gambling (stock buybacks, etc.)

Recall that every debt is somebody’s asset. Debt jubilees sound great to debtors, but not so appealing to insurance companies, pension funds, mutual funds, etc. that own the debt and rely on the income from that debt to pay pensioners their pensions, settle insurance claims, etc.

A meaningful debt jubilee would wipe out the pension and insurance sectors, not to mention trillions in IRA and 401K accounts invested in various debt instruments.

Related Posts

The Secret “Squares” Of Your Retirement Savings

The Secret “Squares” Of Your Retirement Savings USD/CAD Forecast Sep. 24-28 – Crude Climb For CAD Awaiting The Fed And GDP

USD/CAD Forecast Sep. 24-28 – Crude Climb For CAD Awaiting The Fed And GDP- Safe Haven Demand Props Up Yen

Bollinger Bands On Russell 2000 Indicate A Breakout Could Be Imminent

Bollinger Bands On Russell 2000 Indicate A Breakout Could Be Imminent On Currencies That Are A Store Of Value, But Maybe Not For Long

On Currencies That Are A Store Of Value, But Maybe Not For Long Weak Finish To The Week; Bank & Metal Stocks Continue To Fall

Weak Finish To The Week; Bank & Metal Stocks Continue To Fall

Leave A Comment