We live in a non-linear world that is almost always described in linear terms. Though Einstein supposedly said compound interest is the most powerful force in the universe, it rarely is appreciated for what the statement really means. And so the idea of record highs or even just positive numbers have been equated with positive outcomes, even though record highs and positive growth rates can be at times still associated with some of the worst. It may seem like a paradox, but that is only because of the linear frame of reference.

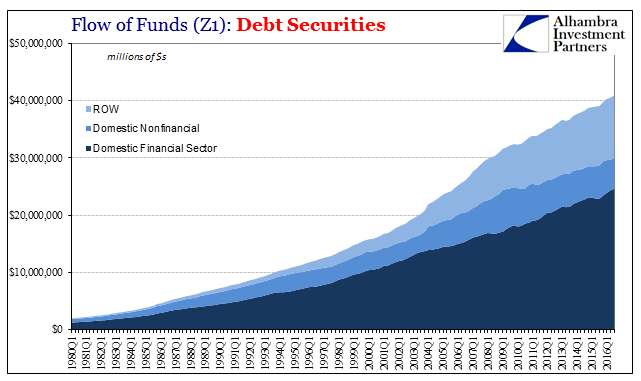

The next update for the Financial Accounts of the United States Z1 (formerly Flow of Funds) is scheduled for tomorrow, but in anticipation of it the statistics through Q3 2016 are sufficient to illuminate this big picture discussion. According to them, total debt securities in the US reached a record high $40.93 trillion in Q3. And in Q2 2016, total outstanding loans within the US of $24.30 trillion ($24.59 trillion in Q3 2016) finally surpassed the prior peak set in Q3 2008 ($24.22 trillion). The Federal Reserve must be right that recovery has been achieved through credit?

Without the non-linear context, these figures are highly misleading. Credit growth simply does not equate to anything other than credit growth. We are conditioned to believe that if there are positive numbers especially in places like debt levels (with all these huge numbers well into the tens of trillions) then it must be that things are getting better if not well on the way to full restoration. But if we look at something like debt securities, the difference may seem quite subtle but no less enormous.

At first glance, there doesn’t appear to be much wrong with the growth of securities; no big contraction during the 2008 panic and certainly not one thereafter. The most you can detect from this linear view is what appears to be a slight change in trend after 2008. If you take it apart further by its constituents, you are left with the impression that it is the Domestic Nonfinancial sector that is responsible for this (and it is to some extent).

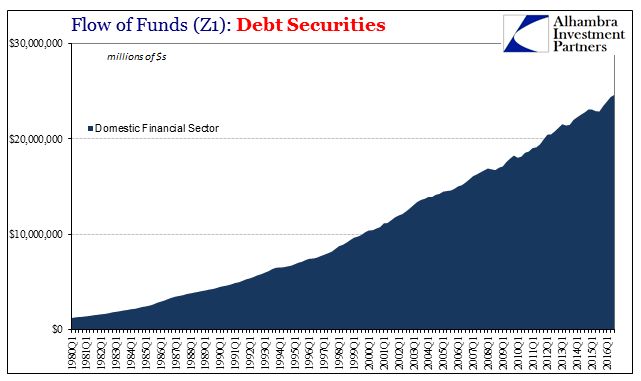

A good deal of that contraction after 2008 is merely different pockets, to where households who held bonds outright prior to 2009 shifted to holding bonds in the form of bond funds (financial sector). From the view of the financial sector, the largest segment, the growth of debt securities have been virtually uninterrupted.

There isn’t even much of a shift pre- or post-crisis except in proportion of what securities the financial sector was holding (a topic for a separate discussion). Overall, the level of debt securities has remained more or less constant, leaving us the foreign sector denoted as ROW (rest of world).

Leave A Comment