Drug giant GlaxoSmithKline (NYSE: GSK) seems like it has been in turnaround mode for several years.

While shareholders are waiting for the company to find its footing, they’re enjoying a 5% yield. Can they bank on that 5% going forward?

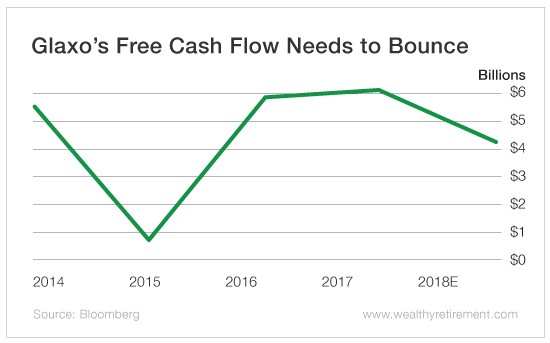

Free Cash Flow Needs to Improve

In 2015, Glaxo’s free cash flow fell off a cliff, dropping to $812 million from $5.5 billion the prior year. It recovered in 2016 and increased in 2017. However, this year, free cash flow is forecast to slip to $4.25 billion.

Four billion dollars sounds like a lot of free cash flow. But when GlaxoSmithKline is paying out more than $5 billion in dividends, that’s a problem.

The fact that free cash flow doesn’t cover the dividend means that the stock’s dividend safety rating gets penalized significantly.

One thing going for Glaxo is its track record. In British pounds, the company has sustained or raised its dividend since at least 2005. The dividend may have fluctuated a bit for U.S. investors after accounting for changing currency exchange rates. But SafetyNet Pro (and I) consider the track record in local currency because that’s what management can control.

The dividend history is impressive, and I’m sure GlaxoSmithKline’s management would like to keep that in intact. However, if free cash flow doesn’t improve soon (to the point where it covers the dividend), management may have little choice but to lower the dividend.

Keep in mind that there has been a talk that GlaxoSmithKline will break up into separate pharmaceutical and vaccine companies. Should that happen, we’d have to see what the dividends – as well as the free cash flow and payout ratios – for each company are to determine whether their respective dividends are safe.

But for now, with the way GlaxoSmithKline is structured, the dividend could be shaky.

Related Posts

GDP Hope Fades As Wholesale Inventories Tumble Most In 8 Months

GDP Hope Fades As Wholesale Inventories Tumble Most In 8 Months China’s Banking System Hits $33 Trillion, Overtaking The Eurozone As World’s Largest

China’s Banking System Hits $33 Trillion, Overtaking The Eurozone As World’s Largest Is The Nasdaq Market Ride Over? Watch Those Divergences

Is The Nasdaq Market Ride Over? Watch Those Divergences EUR/USD Awaits Bearish Pullback And Bullish Bounce At 1.2250

EUR/USD Awaits Bearish Pullback And Bullish Bounce At 1.2250 Gemini joins Coinbase and Block at the Crypto Council for Innovation

Gemini joins Coinbase and Block at the Crypto Council for Innovation- Gold Daily And Silver Weekly Charts – A Simple Lack Of Character

Leave A Comment