“Currency adds volatility – and that can be costly.” – Sales Pitch

One of the main selling points for hedging currency exposure in foreign equities is a reduction in volatility.

The argument typically goes as follows: as a U.S. investor, why take on additional currency volatility if you don’t have to? Simply hedge the foreign currency exposure, leaving you with just the equities, a lower volatility exposure.

On the face of it, this seems to make perfect sense. Currencies have volatility, and so adding them to the risk equation would appear to make an investment more volatile (equity volatility + currency volatility = more volatility). But is this actually the case? Let’s take a look…

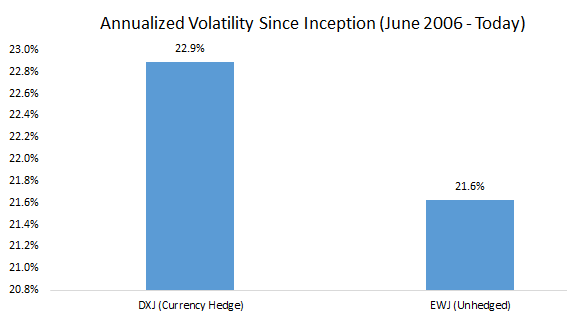

The oldest and largest currency hedged ETF is the WisdomTree Japan Hedge Equity ETF (DXJ), with assets under management of over $5 billion. Since its inception in June 2006, DXJ has an annualized volatility of 22.9% versus 21.6% for EWJ (the unhedged iShares MSCI Japan ETF).

Note: calculated using daily total returns. Data source for all charts/tables herein: YCharts.

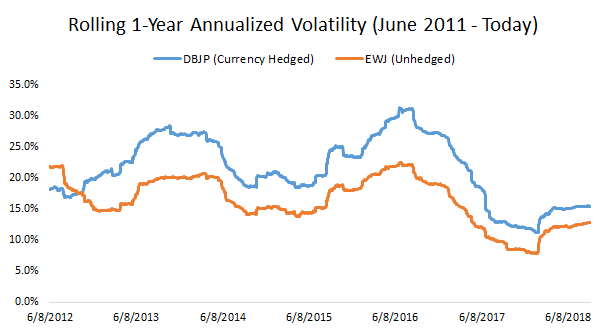

Looking at rolling 1-year periods, we find that DXJ had higher volatility than EWJ 59% of the time.

A second Japan hedged equity ETF (DBJP) was launched in June 2011. Since then it has an annualized volatility of 21.4% versus 17.1% for EWJ, with higher volatility in 94% of rolling 1-year periods.

What gives? How can currency-hedged ETFs exhibit more volatility than their unhedged counterparts?

The volatility of an instrument depends on its variation (deviation from the mean). Including currencies in a foreign equity holding could increase variation and make the path more volatile but it could also decrease variation and make the path less volatile. The latter scenario is precisely what we’ve seen since the start of these two currency-hedged ETFs.

I realize this is not intuitive so let’s run through an example. You are bullish on Japanese equities and bearish on the Japanese Yen, the perfect combination for a hedged Japan exposure. Over the next five days Japanese equities are up every day (+0.5%, +2%, +1.25%, +0.75%, +1%) while the Yen is down every day (-0.2%, -0.3%, -0.4%, -0.25%, -0.5%). The hedged exposure is a success, returning 7.35% versus 5.62% for the unhedged exposure.

Leave A Comment