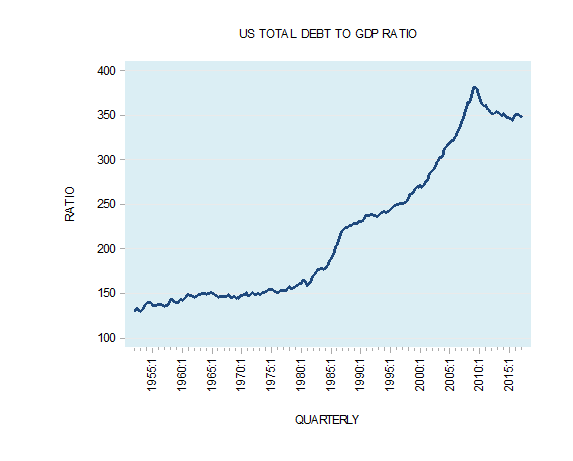

After the 2007-2009 global financial crisis, fears of ballooning public debt and worries about the drag on economic growth pushed authorities in some countries to lower government spending, a tactic that economists now think may have slowed recovery. Note that in the United States the total debt to GDP ratio stood at 349 in Q1 this year.

In a paper presented at the Kansas City Federal Reserve’s annual economic symposium on August 26, 2017, Alan Auerbach and Yuriy Gorodnichenko from the University of California suggested that “expansionary fiscal policies adopted when the economy is weak may not only stimulate output but also reduce debt-to-GDP ratios”. (Fiscal Stimulus and Fiscal Sustainability, August 1, 2017, UC – Berkley and NBER).

Some commentators are of the view that these findings may be welcome news to central bankers who face limited options of their own to combat a future downturn, given existing low-interest rates and low inflation rates in their economies. “With tight constraints on central banks, one may expect — or maybe hope for — a more active response of fiscal policy when the next recession arrives,” the University of California researchers wrote.

These findings are in agreement with Nobel Laureate in economics Paul Krugman, and other commentators that are of the view that an increase in government outlays whilst the economy is relatively subdued is good news for economic growth.

Can increase in government outlays strengthen economic growth?

Observe that government is not a wealth generating entity as such — the more it spends, the more resources it has to take from wealth generators. This, in turn, undermines the wealth generating process of the economy.

The proponents for strong government outlays when an economy displays weakness hold that the stronger outlays by the government will strengthen the spending flow and this, in turn, will strengthen the economy.

Related Posts

So Market, Do You Think You Can Dance?

So Market, Do You Think You Can Dance? Illumina Q1 Earnings Rise, 2017 Forecast In-Line

Illumina Q1 Earnings Rise, 2017 Forecast In-Line What is Online Accounting Software | KPMG PREVA

What is Online Accounting Software | KPMG PREVA Is Raising The Federal Funds Rate A Done Deal?

Is Raising The Federal Funds Rate A Done Deal?- Conundrum 2.0 And The S&P 500 In The Middle Of 2017

The World Has 6 Options To Avoid Japan’s Fate, And According To HSBC, They Are All Very Depressing

The World Has 6 Options To Avoid Japan’s Fate, And According To HSBC, They Are All Very Depressing

Leave A Comment