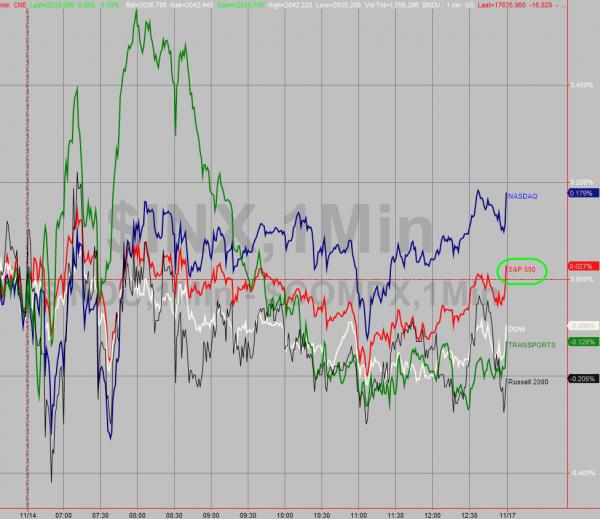

Stocks were somewhat of a sideshow to the moves in Bonds, commodities, and FX today. Trannies (Airlines) and Nasdaq (AAPL) led on the week with Small Caps the laggard and Dow/S&P not much better. A 6-7bps plunge in yields from around 10am ET today left Treasury yields only 0-2bps higher on the week. The USD dumped at around the same time, cracking back to unchanged on the week as USDJPY failed at 117. While oil prices lifted modestly today, WTI Crude fell 3.2% this week – 7th week in a row – longest losing streak since 1986 (the last time US oil production was above 9 mm bbl/d). Silver screamed over 7% off its intraday lows today (+4.1% on the day – the best day in 5 months) and gold surged 2.4% on the day (4.1% off the lows) for its 2nd best day in 5 months. VIX (higher on the week), HY credit, and TSYs all diverged notably on the week from equity ‘strength’ but today’s moves were seemingly driven by Swiss Gold Initiative rumors. It’s a Friday so 330ET saw the standard ramp to grab the S&P green and record close (+0.02%)

The S&P 500 closed the day green… so get out there and spend all that extra cash you have from lower gas prices…

A low volume narrow range day in the S&P…closing perfectly at VWAP

On the day Nasdaq led (AAPL) and Trannies lagged (as oil picked up) along with Small Caps as the late day ramp to green for S&P could not hold…

But on the week Trannies and Nasdaq led and Small Caps lagged unable to be rescued green on the week…

On the week, Discretionary and Tech led as Utes and Energy lagged with Financials red

As Financials for the 3rd time roll over and catch down to credit…

VIX closed the week higher – despite stocks strength…notably divergent

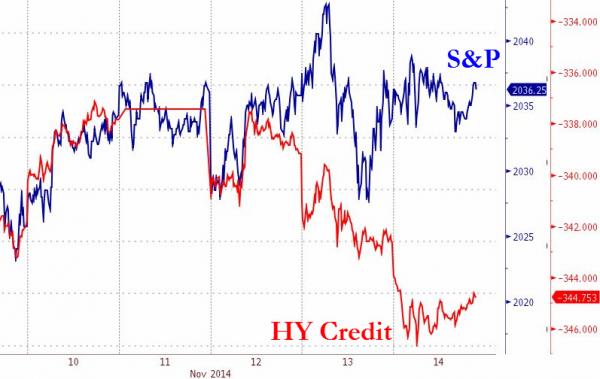

HY credit closed the week wider… notably divergent

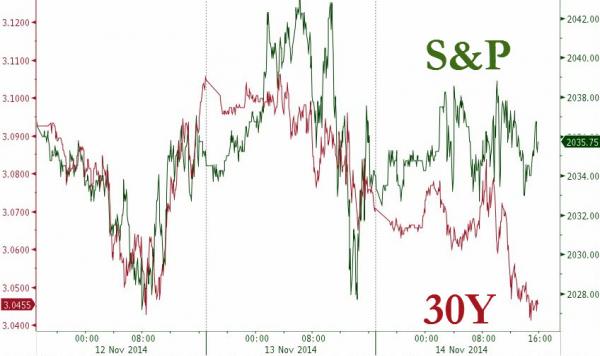

And TSY yields decoupled from stocks once they came back from vacation Tuesday…

Treaury yields surged and purged today with a dramatic rally starting around 10am

Related Posts

EUR/USD Continues To Ease Off – Market Least Short Since May 2014

EUR/USD Continues To Ease Off – Market Least Short Since May 2014 3 Signs That Inflation Is Under Control

3 Signs That Inflation Is Under Control Forex Today: Bitcoin Keeps Coiling Below Record High

Forex Today: Bitcoin Keeps Coiling Below Record High Trump Unwisely Escalates Trade War: Expect A “Rare Earth” Response From China

Trump Unwisely Escalates Trade War: Expect A “Rare Earth” Response From China Short Setups – If There Was Ever Going To Be A Sell-Off

Short Setups – If There Was Ever Going To Be A Sell-Off- Binary Options Trading Opportunities – December 22, 2015

Leave A Comment