Don’t expect Fed to cause Apocalypse

The Fed has ample room to shrink its balance sheet by draining excess commercial bank reserves held at the Fed without causing either the economy to crater or debt and equity markets to crash. Indeed this has been rapidly underway since the start of 2016.

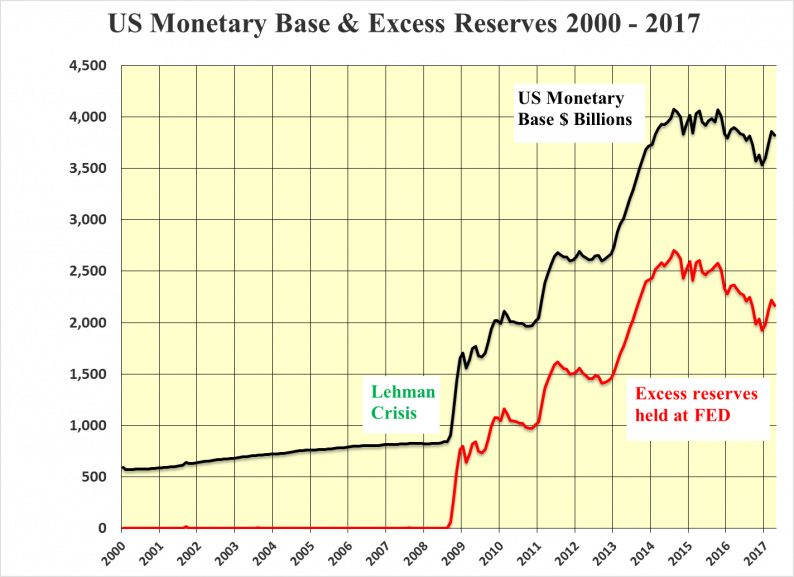

As mentioned previously the Fed has been engaged in Quantitative Contraction, QC, from its post Lehman peak of US$4.075 trillion in August 2014. First gradually, then more rapidly in 2016, to the recent low of last December at US$3.532 trillion.

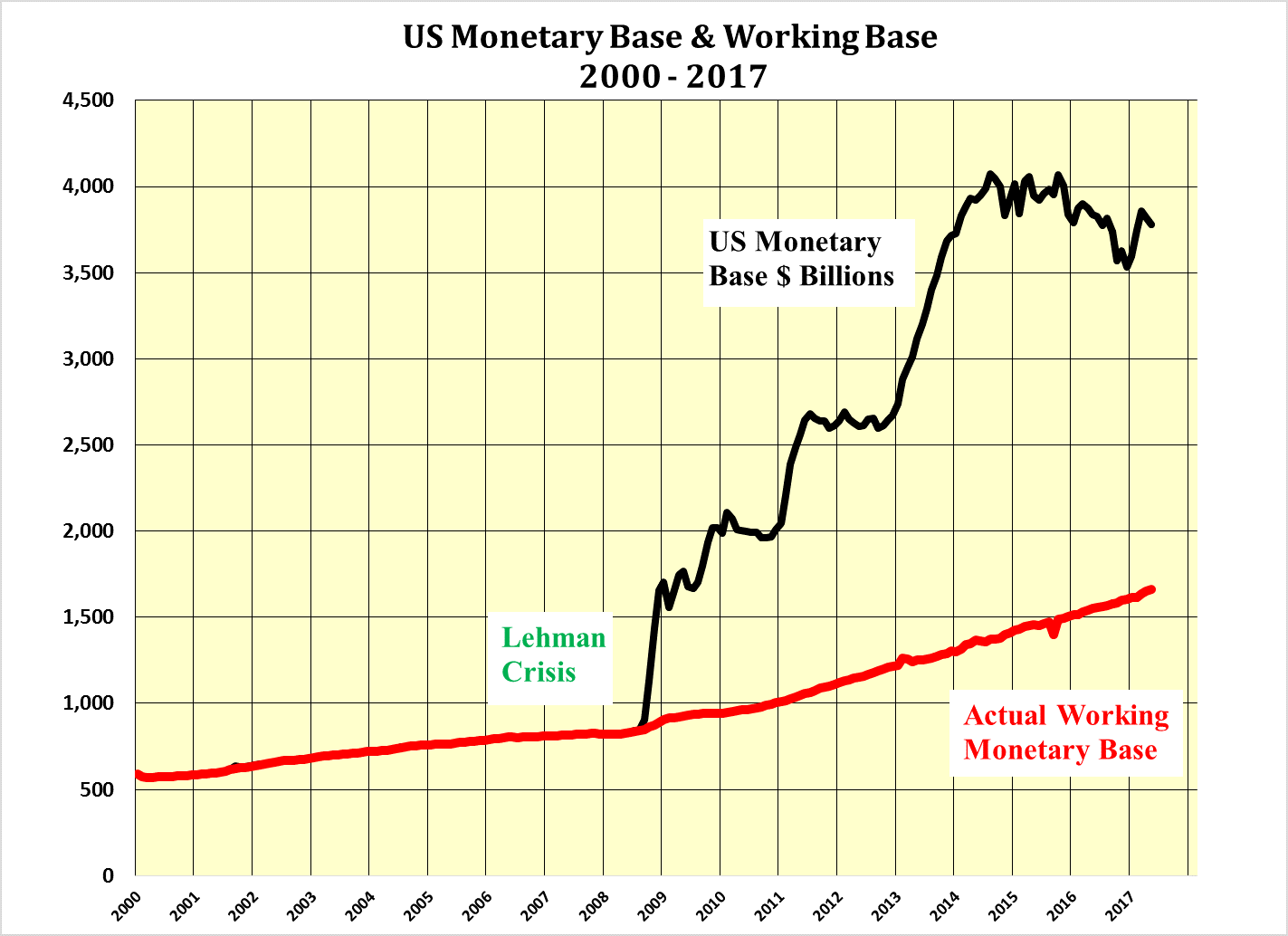

The 13% drop over the 16 months amounted to US$0.543 trillion. All of this was the result of a 30% reduction, US$0.775 trillion, in the excess reserves held at the Fed. The difference between these figures of US$0.232 trillion continued the movement of funds into the real economy with the Actual Working Monetary Base, AWMB, rising the same US$0.232 trillion.

Since the start of 2017 the Fed appears to have reversed its action evidenced by the rise in both the total monetary base and the continuing rise of the AWMB. From this it could be surmised that QC in 2016 was overdone with the rebound in the 30 year T Bond yield from its July low of 2.10% and the rise in the U.S. dollar above parity was accompanied by lower than expected growth of U.S. GDP.

The last things the Fed wants are:

Despite the heavier than required action by the Fed in 2016, to avoid the above, the Fed’s watchword now appears to be “gradualism”. Hence, it is unlikely that there will be any more dramatic action to move short-term rates sharply higher any time soon.

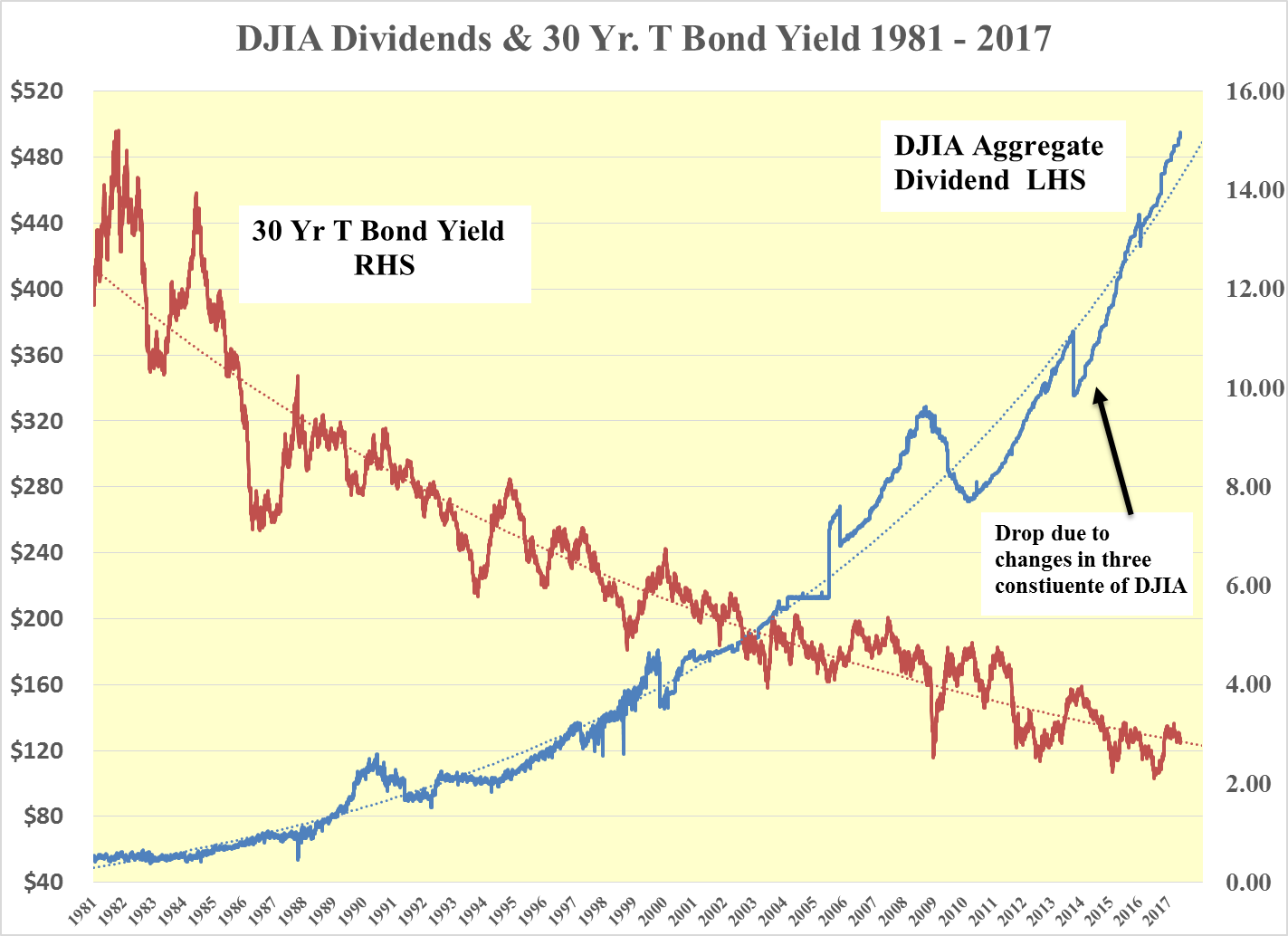

Steady Fed and Record Dividends Point to Higher DJIA

Any gradual increase in rates will be to lean against the winds of inflation resulting from an overheating economy, which is not likely during the remainder of this decade. Rather a slow and steady reduction in the total monetary base over the next 5 years seems probable with the continuation of growth in the AWMB.

Related Posts

Markets Are In The “Eye Of The Storm”, Trader Warns

Markets Are In The “Eye Of The Storm”, Trader Warns Stocks And Precious Metals Charts – As Greed Turns Slowly To Fear

Stocks And Precious Metals Charts – As Greed Turns Slowly To Fear USD/JPY Price Analysis: Shies From 160.00 As Japan’s Intervention Fears Intensify

USD/JPY Price Analysis: Shies From 160.00 As Japan’s Intervention Fears Intensify- When Will The Corporate-Debt Bubble Burst?

Top 5 cryptocurrencies to watch this week: BTC, ADA, SOL, MATIC, KLAY

Top 5 cryptocurrencies to watch this week: BTC, ADA, SOL, MATIC, KLAY- BTC/USD Forex Signal – Monday, Nov. 27

Leave A Comment