In a December articleI laid a conservative estimate for what we could expect from AMD (AMD) in 2018 and why the $10 price was a real bargain. After three months the stock is 15%-20% up, and if you sold on the peak, it’s probably time to grab back your shares.

The stock is trading at similar or better valuation levels than it was in December. My updated valuation shows that the current price today is only reflecting the beat in earnings for Q4, and while the upside is virtually the same, the downside is much lower.

I like to do pessimistic valuations to ensure even some negative surprises are within the forecast range. Q4 managed to beat my most optimistic forecast, guidance for 2018 was a bit ambiguous, but at this price, the stock has small probabilities of going down and plenty of room to grow.

Valuation

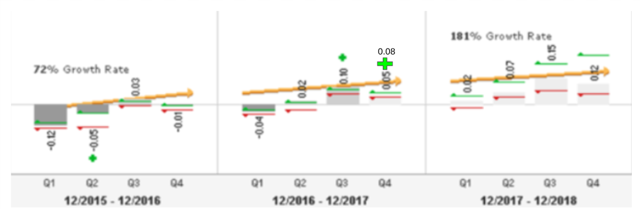

Let’s go back in time three months, and look at the Non-GAAP EPS forecast.

Source: TD Ameritrade + Author’s remarks

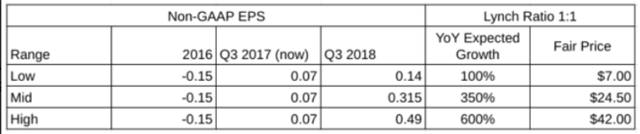

I used the Lynch method for growth valuation.This method uses the ratio between the expected earnings growth and the P/E of the stock to determine its fair value. A stock that has a 1:1 ratio is fairly priced. The higher the number, the more underpriced the stock is.

Both extremes reflected AMD being at the very top or the very bottom of the expected earnings range four quarters in a row. The bottom prediction by the Lynch method had the fair price falling to a $7 price while the top had it blowing up to 42 dollars, as it can be seen in the chart above.

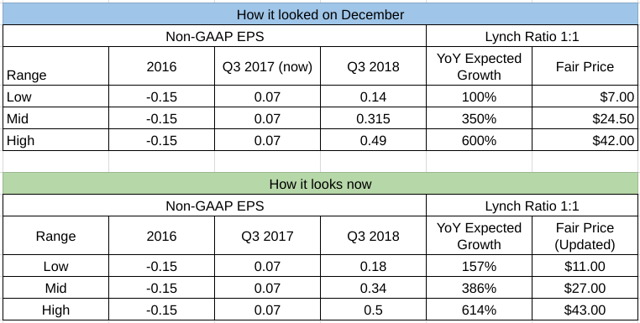

Q4 delivered an impressive and unexpected beat in earnings, which changes significantly how the same chart would look now.

Source: Author’s Charts

The Top range increased only $1, not very exciting, but the bottom valuation is now $11, a considerable improvement. So while the stock has about the same upside, the downside is much less. While in December the stock was trading 3 dollars above the most pessimistic fair price, now it is trading at less than $1 above an arguably fair price.

Leave A Comment