Economic growth and higher wages historically weren’t always associated, at least for decades (typically before the Gold standard was dropped and global growth expanded, largely -in time- at the expense of American workers and our industrial expansion), with ‘inflation’ as somehow being ‘desirable’. The idea was to see profits and growth occurring consistently, amid organically-achieved GDP gains; not any sort of financial engineering beyond consistent slow M2 growth.

The thousands of words presented by the FOMC today boil-down to cowardice, as relates to using the data points they had said justified a slight rate rise; to put the economic community back into a quandary from now until the June meeting; a more treacherous time to take any move, given the proximity to the BREXIT vote, and an often-seen sluggishness occurring during the Summer.

Despite evidence based on measures their own work suggested; they demurred and did nothing today, which markets loved. Chair Yellen was less than candid; although the admission that both inflation and growth will be low, disappoint her; while only the slow growth part should be bothersome. That’s fine; rallying like this in the S&P market was initially sold-into; then rebounded, and held-up pretty well, perhaps slightly related to the Quadruple Quarterly Expiration coming now.

Lots of ‘open interest’ was likely consumed by wild moves (including downward phases within the comeback), which may mitigate how much is left for these two days of the Expiration starting now. That’s one reason I noted that we’re merely in the lower reaches of the resistance area (now upper part of the lower zone for June S&P, with the higher part being 2040-2060 and thus a break-even mental stop on the remaining quarter of the original (near) June 2065 short-sale.

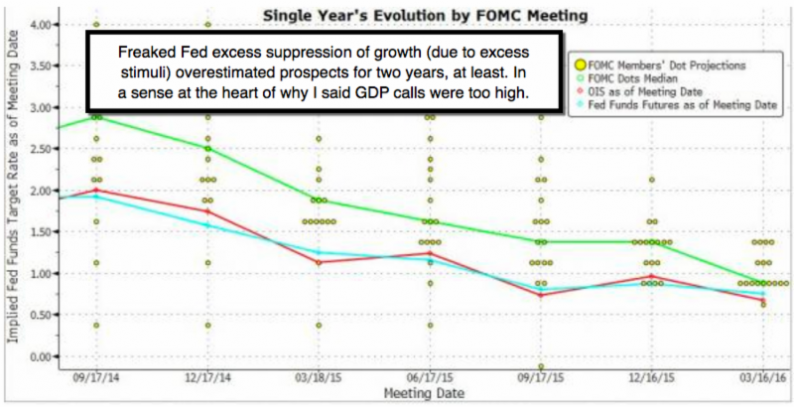

In-sum: my takeaway from today’s Fed ‘chat’ was that the global economy has and is slowing ‘more’ than they previously anticipated (recall there was criticism late last year about the Fed justifying their slight increase based on ‘recovery’).

Financials sold-off, which is the primary group that responded properly to what is a Fed intent on keeping rates low; which diminishes bank income prospects, since the tapering already reduced the ability to have a revolving money-making door (playing the circuitous Treasury approach they did for several years). What kept the broader market up? Besides Apple and the most-shorted (due to some accelerated reduction of remaining pre-Expiration open-interest stocks or index positions); you had Oil stocks benefiting from Iran’s flip-flop (perhaps their need for oil revenue paled in their bazaar dealings with Moscow, when Russia refused to keep ‘carpet’ bombing their adversaries).

Teheran’s rug merchants probably got so hard to deal with (remember originally a Russian Oil meeting which got cancelled because Kuwait, and especially Iran, despite said beholden to Russia as it relates to their cherished ‘Shia Crescent’, wouldn’t support Russia’s need for oil prices to firm); that Russia announced the partial withdrawal from Syria. Their Army was more present than widely known; as I’ve pointed-out a couple times. Now; whether nervous about eroding what’s been achieved (from their perspective) or not, they reversed course yet-again; and a meeting in Doha is scheduled for next week regarding oil production level concerns. That supported Oil stocks and Oil; and is part of the rest of the story.

Related Posts

EU Session – Bullet Report – No Rate Hike For Now – Gold Reaches 2 Month High

EU Session – Bullet Report – No Rate Hike For Now – Gold Reaches 2 Month High Jefferies Ups Finisar To Buy On Valuation, M&A Potential

Jefferies Ups Finisar To Buy On Valuation, M&A Potential- Is The Fed Confused?

Why I Still Like Cash

Why I Still Like Cash- Here’s how the crypto industry is using artificial intelligence

- Top 5 cryptocurrencies to watch this week: BTC, DOT, SAND, RUNE, ZEC

Leave A Comment