Flattening Yield Curves Must Not Be Ignored: The Case in Canada

The debate about the true meaning of a flattening yield curve continues, especially among FMOC members. As reported in recent blogs[1], Chairman Powell suggested that low inflation diminishes the usefulness trying to forecast a recession based on the spread between long and short Treasury yields. In fact, Fed member Loretta Mester, goes even further by claiming that the recent flattening of the U.S. yield curve is due to “structural factors,” such as bond-buying by central banks. Finally, in a non-sequitur, she switches the argument to say that long rates will go up and therefore the Fed must continue to raise short rates. [2] It seems that nothing will get in the way of the Fed jacking up short rates, including a flattening yield curve.

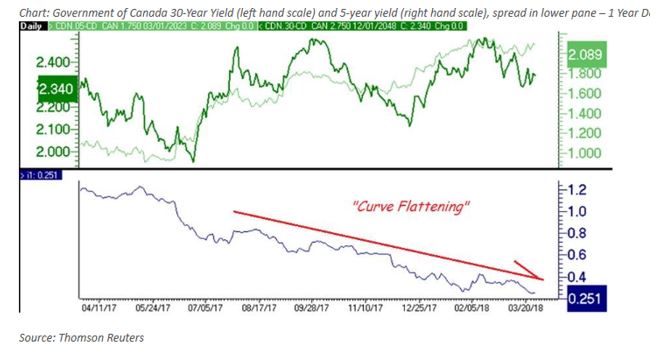

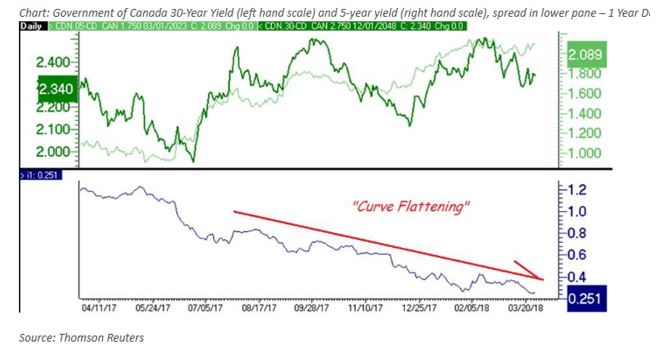

The Canadian experience can shed some light on the meaning of a flattening yield curve. There has been an unmistakable yield curve compression over the past 12 months in Canada (Figure 1). Canada never had a QE program, so this explanation for the flattening does not stand up to scrutiny. For the first half of 2017, the economy grew at a very impressive 4 per cent rate annualized—yet the spread between 30yr-5yr actually narrowed dramatically. So, economic growth, rather than pushing up long rates, had no impact on the rate spreads. The issue of economic growth has an asymmetrical influence on the yield curve. When growth started to weaken in the second half of the year, that weakness just accelerated the narrowing of the spread (Figure 1).

Figure 1: Govt of Canada Yield Spread

The Bank of Canada raised its policy rate three times since July, 2017 from 0.50 bps to 1.25 bps. During that time, the 10yr bond only moved up60 bps; 30yr yield did not budge at all (Figure 2). The Canadian bond investors did not change their views on the outlook for inflation and economic growth, despite the central bank’s efforts to have rates return to “normal”. Recent statements by bank officials seem to indicate that investors should not attempt to map out a set path for future rate changes since the outlook continues to be highly uncertain.[3]

Leave A Comment