Historically, we’ve seen stocks correlated well as a ‘leading indicator’ for the US economy. That is considerably less the case now because of direct or indirect inventions by the U.S. Fed, as well as impacts from foreign central banks. They have generally intruded upon rational price discovery in market ranging from an obvious impact (waning for many months) of Quantitative Easing, or stimulus of various sorts on equities, to impacts on credit, futures, and currency markets as well.

This doesn’t throw technical analysis out the door at all; rather it has required a more focused exploration of the factors underlying markets, which continues to impact prices in every sector, beyond anyone’s long-term theories. Besides the key to recognizing last year as ‘distribution under cover of a firm DJ and S&P; it was essential to identify the retreat of Fed monetarist enthusiasm, and the lack of respect for declining economic and GDP indicators for several Quarters. This is true now as well, as hope springs eternal that this weekend’s G20 somehow is going to revive monetarism and inject needed liquidity into illiquid markets. In our view it won’t succeed for long even if attempted; because of earnings, plus the overall background and consumer constraints; which remain recessionary.

For our part, besides interpreting the most recent snap-back as a ‘bear market’ rally, and nothing more; it was important that we interjected the ‘phony’ oil story as a causal factor amid our technical work. And while I believed it would carry into the mid-1940-50 or so area (because short-covering rallies are sharp, if short-lived, there was little or nothing fundamentally behind it all). I suspected ‘front-selling early this week; if indeed the majority were suddenly talking about buying, for even higher S&P levels, which I thought ludicrous as you know.

What gave me the confidence to suspect market failure? Well aside respecting the coming G20 Meeting (risk of liquidity injections), month-end activity, and of course the questionable ceasefire in the Middle East (hoping it’s not placed at a particular time to allow plausible deniability to the U.S. and Russia if Turkey or Saudi Arabia happen to invade Syria, which is also standing-down, just then).

Or it’s even possible that everyone is standing-down so as to discourage Saudi incursions, which were rumored with an ‘exercise’ slated late this week too. The timing is just a bit too coincidental; hence bears watching. It’s ironic that none of the Western media appears to hone-in on ‘why’ Russia and the U.S. agreed to a ‘cessation of hostilities’ without any of the terrorist groups agreeing too (if it could even be coordinated). That’s part of why I believe we haven’t heard ‘the rest of the story’ (as radio’s late Paul Harvey would say).

Our view has been that any such ‘maneuvers’ (by all the powers involved) are a distraction to the main point: Oil and currencies. You do not have serious global growth; you don’t even have US consumers loosening up (or restaurants would be doing better given cheap gasoline); and you have a domestic political middle class upheaval, represented by two candidates on opposite political sides (but they are not polar opposites as some pundits try to portray them; as both focus on shaking-up the establishment). And then today you have a Federal Judge ordering deposing of State Dept. staffers, and flat-out questions as to ‘why’ the former Sec’y. of State saw a need for a private Server in the first place. All this conforms to the least sanguine environment seen in politics for some time.

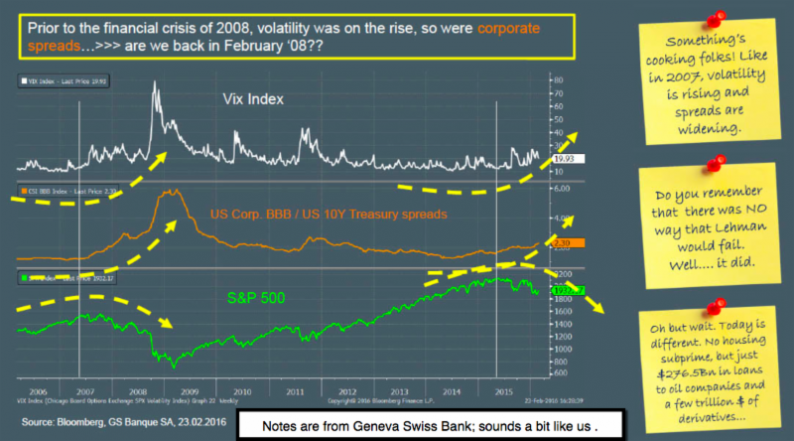

This is a time of turmoil. In society, and in markets. Ongoing, rather than merely looming, recession (we track it from July; said so since last Summer); imminent energy bankruptcies. Chinese devaluation any time soon, earnings stink, plus a continued valuation disconnect shows no prospect of quick restoration, except by one method: that’s a progressive march to lower levels for the S&P 500.

In sum: this market has pivoted around on the back of Oil, to cut to the chase. But that there was ‘no’ Production cut deal is how we interpreted the ‘dropped context’ to statements in Tehran, last week and yesterday; well before a denial of cooperation was reiterated by their oil minister during Tuesday’s market. The Saudi Oil Minister amplified that in Houston. That validates our interpretation of recent days, before the charts showed it all.

The markets have responded ‘as if’ something changed. He merely appeared in a live broadcast where no reporter could really spin the tale; as had been done with several Saudi, Iranian, and OPEC official statements earlier; and dating to the first phony story a week ago Thursday that made the WSJ newswires from the UAE, before it was retracted minutes later; though ‘the Street’ determined it wasn’t ‘clear’. Actually it was clear; there was no deal; and while realizing that we’d get a bear market rally we thought it would falter about where it did both in time and price this week.

Conclusion: the markets are not reacting significantly yet; but take a few more points off the S&P, and there will be some algorithmic signals generated. We continue short March S&P / E-mini from 2065; for the remaining 50% of total position; after taking 130 & 200 handle gains harvested earlier.

Daily action – lots of nervousness after JP Morgan discussed loan-loss reserve conditions (increased moderately but perhaps insufficiently). And they’re not in the worst spot of major banks involved with energy or related funding. All that’s happening is a return to recognition that nothing changed other than we got the bounce in the market; for which many apparently forgot to sell the rally.

This evening the futures are off just a couple handles; Asia is starting mildly off a bit; and there is a bit of focus on the revelation that China has set-up not just mobile missile batteries on the artificial islands, but added radar stations. Next, you will likely hear what a source claims happened today: Chinese jet fighters being deployed to the ‘atols’ or islands. If confirmed that sure douses the claim that it’s for fishing, respecting navigation, or even for ‘helicopter’ use. The West has given China every opportunity to tone-down their adventure; but they have not taken it; and in fact if this is true, then it’s likely considered an ‘escalation’.

There was another big Oil and Gasoline API inventory build reported late today as well. This may put additional downward pressure on WTI in the morning. If so, it will be hard to ‘cap’ the brewing S&P sell-off. Stay tuned.

For our part; we backed-away from any protective stop yesterday and Tuesday in-anticipation of the move running out-of-steam. It did, whether it’s just oil or a JPM discussion; or the geopolitical backdrop (mostly Oil, but everything plays a role). We simply hold short for now; with no changes; and it’s quite possible we have seen the end of the rebound just about where we desired it, with multiple short-term zigs-and-zags looming, but likely part of a process headed lower.

Wednesday could be a down-up-down session; even threatening the 1900 S&P futures level, if all goes well from a bearish perspective.

Prior highlights follow:

Leave A Comment