June can be an ‘event-risk’ month- especially this year. Often it can go either way or vacillate in a range; such as last year with the projected dip and then the rebound into early-mid July (what I often refer to as the ‘Mom’s Birthday rally’).

It is trickier than usual this year, given not only our Fed or global central bank and geopolitical concerns; but also the upcoming BREXIT vote, which now has (as first noted here last week) a slight bias to leaving; and surprisingly that now includes many ‘in’ the financial industry. That development, of course minimized by analysts as a catalyst impacting us, indeed will especially if it’s perceived that a year or two of negotiating with the EU results in a UK economic contraction. If so you could pummel the Pound Sterling by as much as 15-25%; some currency guys estimate; which would roil markets significantly. Conversely, solid voting to ‘remain’ in the EU would simply trigger a relief rally, and probably not much of a lift to the Pound, but may trigger a short-term Euro rally and Dollar pullback, IF the vote goes that way. But again those would be transitory against a backdrop of a stronger US Dollar, which has evolved very close to the outlined pattern.

Now; the ‘added’ Travel Alert just as Summer travel plans are already made by a majority of vacationers, is a bit odd as relates to Americans, as we already do have an ‘alert’ ever since the Paris carnage and again the Brussels attacks. So I looked into it just a bit; and read about the poor performance of a ‘trial’ terrorist security drill at the main Paris soccer stadium last week; and acknowledgement by French Intelligence at a Conference within the last 3 days that they sadly do believe that ISIS and related elements active ‘in’ France and elsewhere now in Europe (thanks to naive policies some will say) have the personnel and capacity to mount attacks. Officials are concerned they won’t be able to prevent them all.

Related Posts

Foreign Energy Stocks May Be Up, But Don’t Take The Bait

Foreign Energy Stocks May Be Up, But Don’t Take The Bait Most Active Equity Options And Strikes For Midday – Monday, Oct. 15

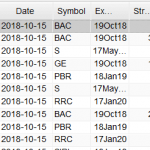

Most Active Equity Options And Strikes For Midday – Monday, Oct. 15 3 Things: Explaining The Consumption-Disfunction

3 Things: Explaining The Consumption-Disfunction- Hot Options Report For End Of Day – Monday, November 13

Insider Trading Report Edition 273: Notable Buys And Sales

Insider Trading Report Edition 273: Notable Buys And Sales Consumer Confidence ‘Steady’ Despite Weak Wages, No Spending, Slow Growth

Consumer Confidence ‘Steady’ Despite Weak Wages, No Spending, Slow Growth

Leave A Comment