Greetings,

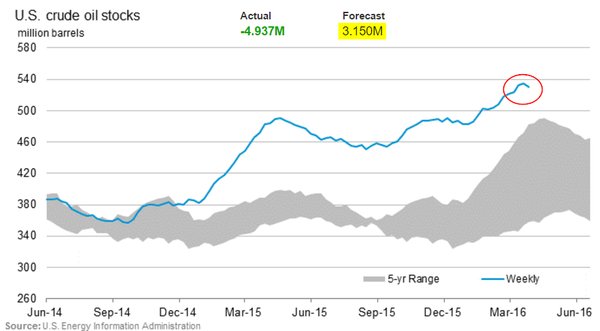

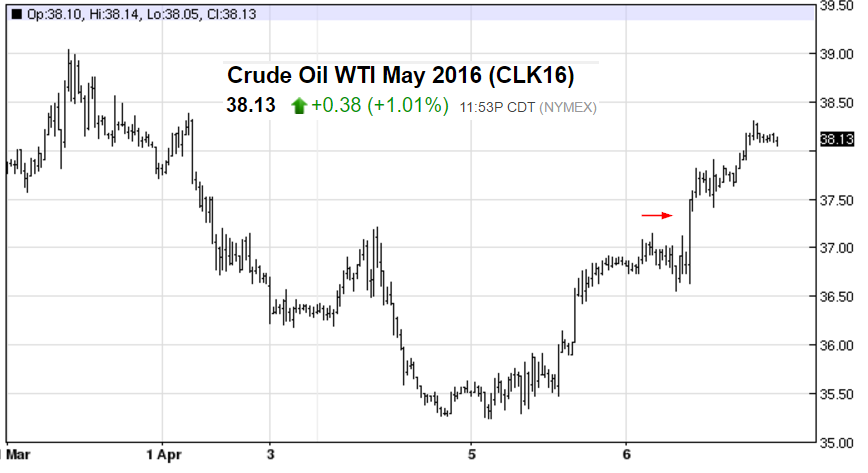

We begin with the energy markets where the Energy Information Administration (EIA) confirmed yesterday’s API report showing a larger than expected draw on US crude oil inventory.

NYMEX crude oil rallied 5% during the day in response and is up another 1% in the after-hours trading (boosting global equity markets). The fact that the amount of oil sitting in US storage facilities can impact the stock markets to such an extent is unprecedented.

Source: barchart

Continuing with energy, here are several other developments.

1. The crude oil curve has been flattening (contango shrinking).

Source: ?@JavierBlas2

2. Crude oil correlation with the HY markets is at record levels.

Source: @tracyalloway, Goldman Sachs

3. US crude oil production falls to 9 Mbbl/d from 9.6 at peak, with declines remaining very gradual. The second chart below compares the recent output decline with the previous year.

Source: EIA

Source: EIA

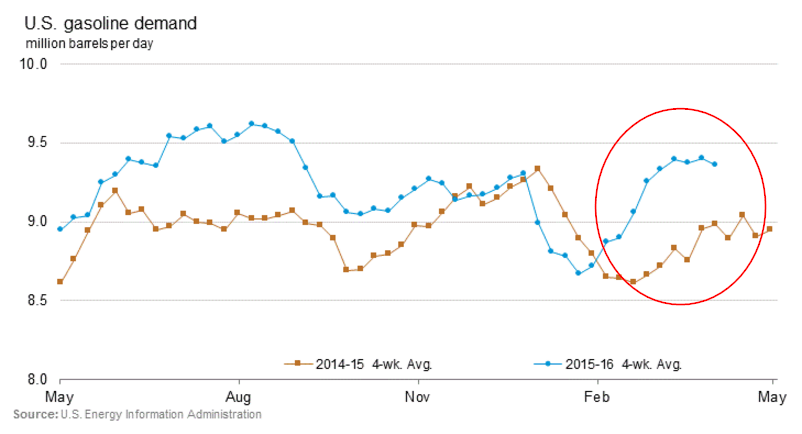

4. US refinery inputs and gasoline demand remain above last year’s level.

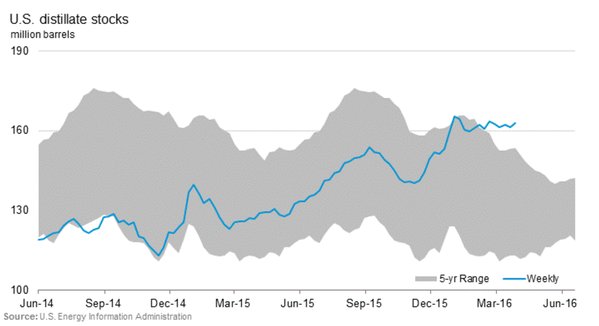

5. US distillates (heating oil, diesel) inventory levels are much higher than where they should be this time of the year.

Below are the inventory levels of US residual fuel (heavy fuel oil), jet fuel, and diesel – all highly elevated.

Source: Morgan Stanley

Source: Morgan Stanley

Source: Morgan Stanley

In other commodity markets, it seems that the wholesale diamond prices have stabilized for now. Most analysts don’t see significant appreciation from here.

Source: Zimnisky

In the currency markets, dollar-yen declines continue as the currency pair approaches 109 (yen per one dollar). This yen move puts the BoJ in a difficult situation as the yen strength could derail the fight against deflation.

The yen rally is surprising given the elevated risk appetite. As discussed yesterday, usually the yen rally corresponds to risk-off sentiment.

Leave A Comment