Greetings,

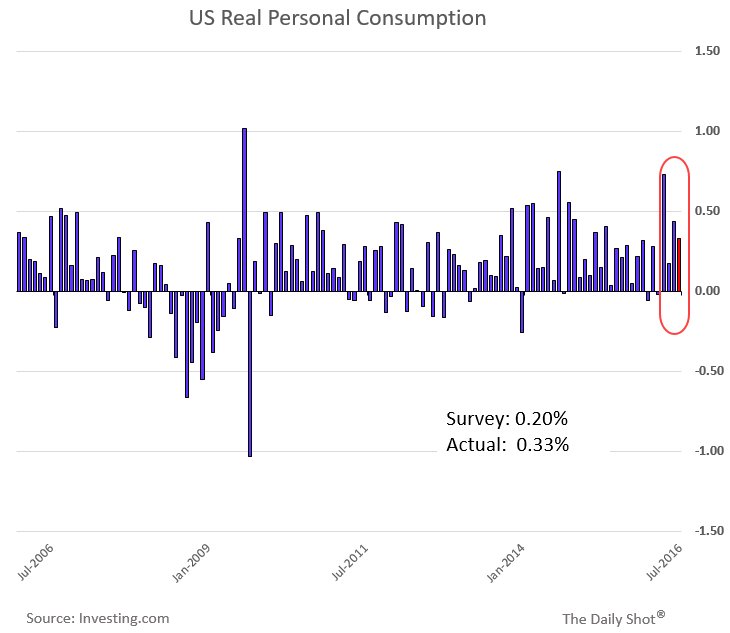

Once again we begin with the United States where consumer spending remains solid, with the July figures beating forecasts.

Further reading

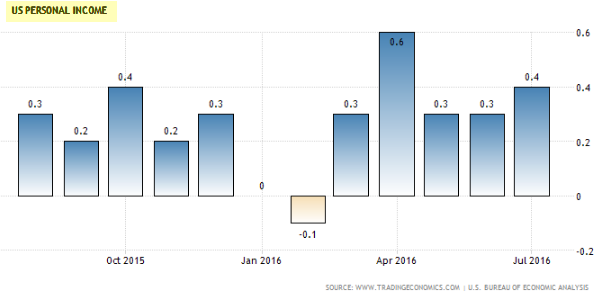

Personal income also continues to grow.

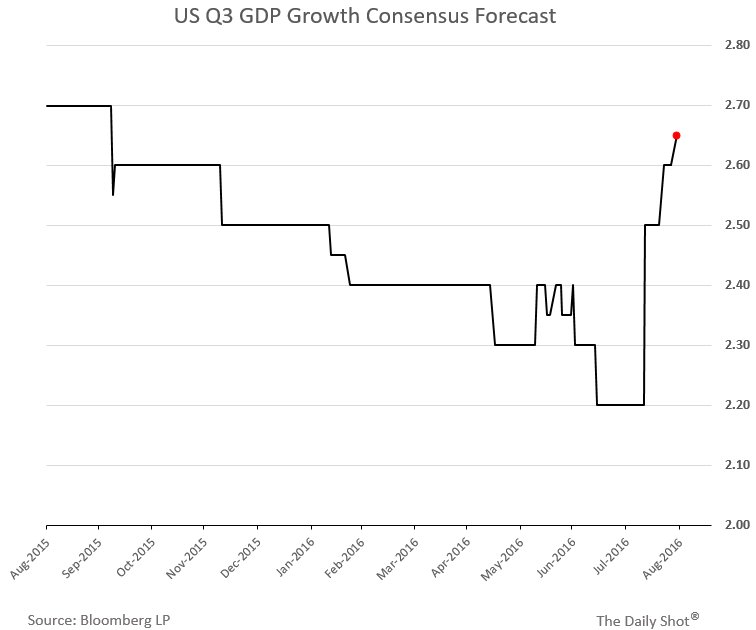

In response to the above data, economists are revising the Q3 GDP forecast higher again. Here is the consensus projection.

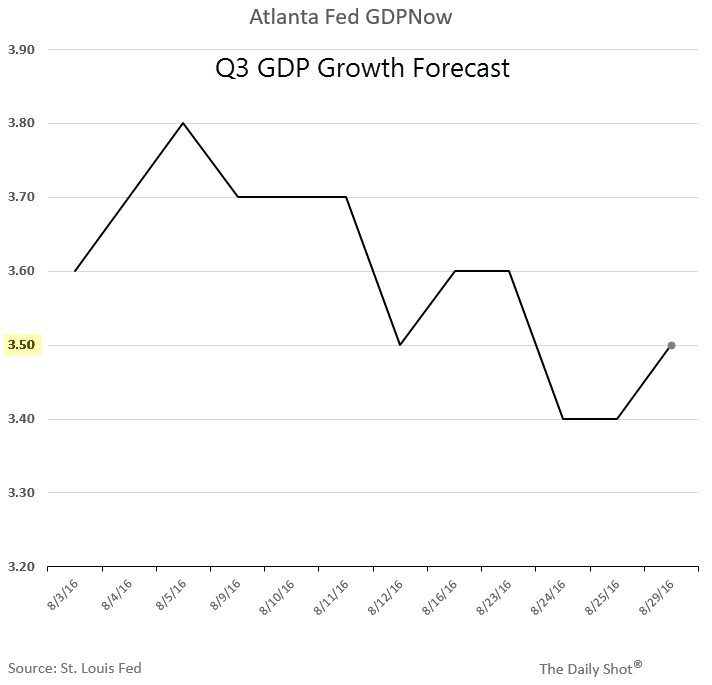

The latest nowcast model from the Atlanta Fed (GDPNow) also moved higher – still significantly above consensus (above).

Source: @AtlantaFed

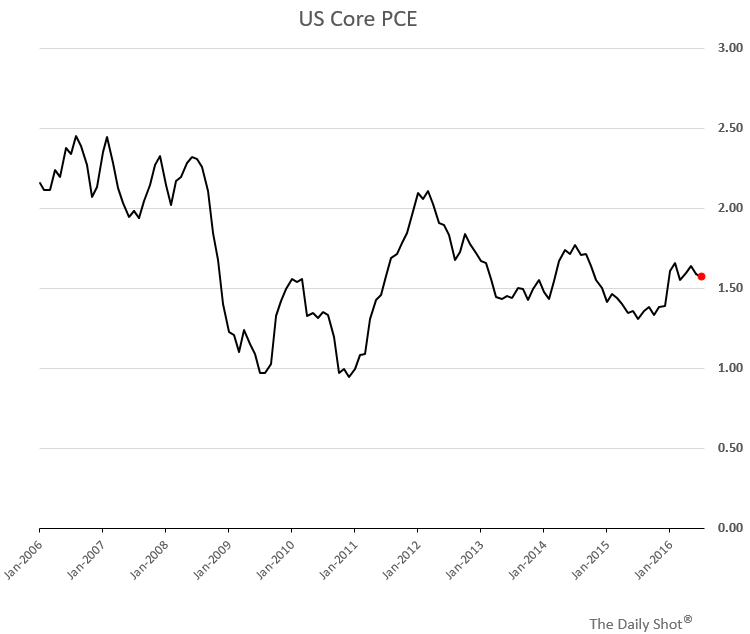

1. In other US economic developments, inflation remains benign. Here is the core PCE.

Source: St. Louis Fed (FRED)

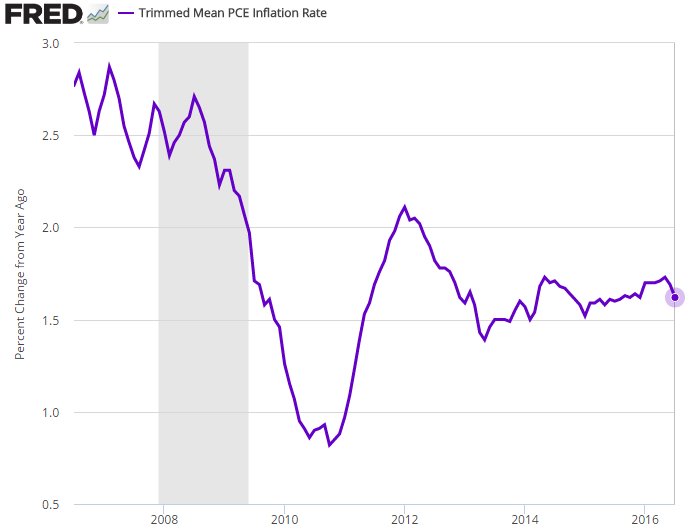

Similarly, the US “Trimmed Mean” PCE Inflation Rate (from the Dallas Fed) turned lower.

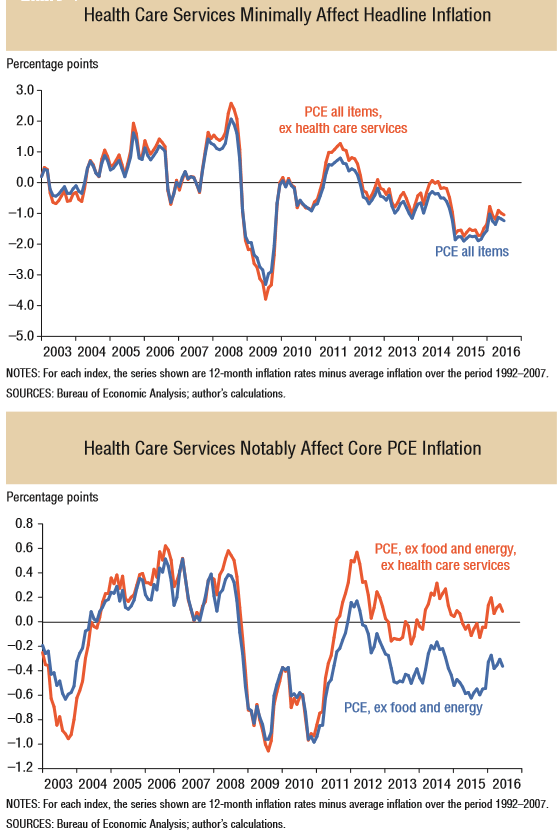

By the way, a paper from Dallas Fed points out that healthcare services, while having only a limited effect on the headline figure, generate a significant drag on the core PCE.

Source: Dallas Fed

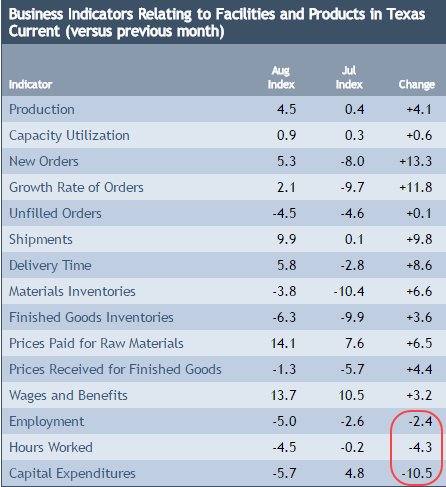

2. Speaking of the Dallas Fed, the Texas area manufacturing index showed improvement. However, employment and Capex components worsened. Also, the report seems to show some margin pressures.

Source: Dallas Fed

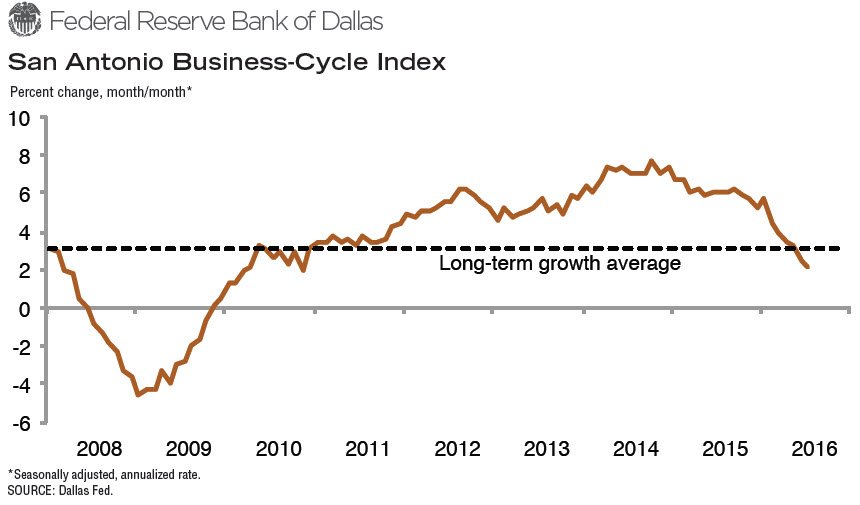

3. The Dallas Fed also highlighted San Antonio’s Business-Cycle Index turning sharply lower.

Source: Dallas Fed

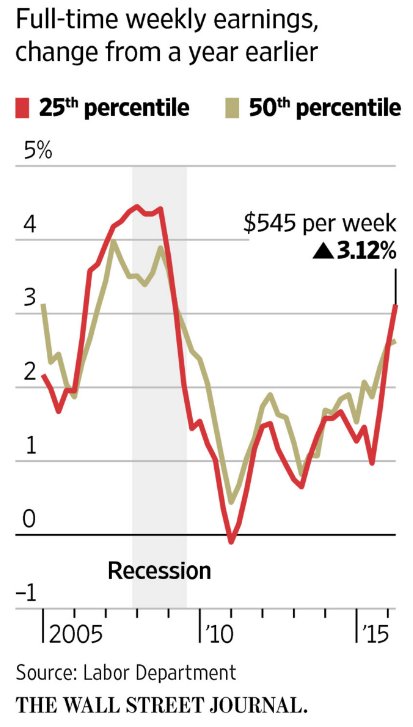

4. The Wall Street Journal pointed out a sharp pickup in wage growth for lower-paid Americans (discussed here a few weeks back). This trend is explained by the implementation of minimum wage laws as well as other factors.

Source: @WSJ

5. The Treasury yield curve flattening continues. Here is the 30y – 2y treasury spread.

Source: St. Louis Fed (FRED)

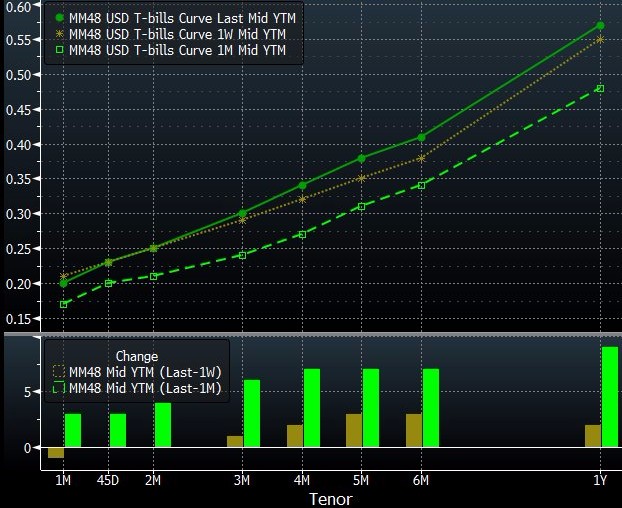

Note that the curve is actually steepening at the short end as rate hike expectations increase.

Source: Bloomberg Terminal; Function “GC”

6. Here are the projections of the Fed’s bond holdings which are of course dependent on when the central bank stops reinvesting maturing (or amortizing) securities. Many analysts remain skeptical of the Fed’s ability to begin exiting its holdings in the years to come.

Related Posts

United Posts Earnings Beat, CEO Apologizes Once More For Scandal

United Posts Earnings Beat, CEO Apologizes Once More For Scandal USD/CNH At Resistance, Event Risks In Focus

USD/CNH At Resistance, Event Risks In Focus 3 Factors Making A Strong Cash Stock Market Crash In 2018

3 Factors Making A Strong Cash Stock Market Crash In 2018 Is The Bearish Run Over For British Pound ETFs?

Is The Bearish Run Over For British Pound ETFs?- Recent Stock Purchase October 2017

Treasury Sells 30Y Bonds At The Lowest Yield Since January

Treasury Sells 30Y Bonds At The Lowest Yield Since January

Leave A Comment