We begin with Friday’s US employment report. The number of jobs created in January was below consensus but the market interpreted the figures as “hawkish” (potentially providing some ammunition for the Federal Reserve to continue raising rates). Short-term rates rose in response (treasuries and rate futures fell).

Fed Funds futures declining implies expected fed funds rate rising (Source: ?barchart)

Markets were especially spooked by rising wages: from 2% to 2.5% per year. It’s not clear however if this qualifies as “wage pressures”.

Another trend “spooking” the markets is the convergence between the unemployment rate and NAIRU (as the headline unemployment rate falls below 5%). NAIRU is the rate of unemployment below which inflation supposedly begins to rise.

However, the NAIRU trend can be misleading because the declines in some broader measures of unemployment have stalled. Here is U-6 for example.

We also see the average duration of unemployment remaining elevated.

The improvements in US labor markets therefore have been uneven.

One can see the markets’ lack of confidence in the jobs report in the flattening of the treasury curve on Friday.

Source: @SoberLook

Other than the nasty equity market selloff, several indicators pointed to significant jitters in the market.

1. Deutsche Bank CDS continued to widen (as discussed Friday).

Source: @MattGarrett3

2. Gold prices rose sharply.

Source: barchart

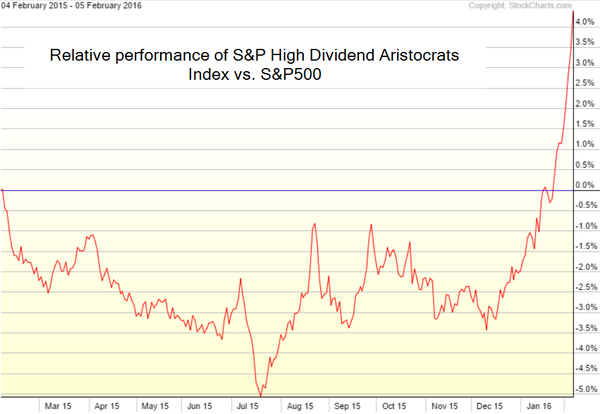

3. High-dividend shares saw a massive outperformance over the last few weeks.

Source: Stockcharts.com

Speaking of equity markets, here are several trends to watch.

1. Related to the above, US utilities are outperforming.

Source: Stockcharts.com

2. US “value” shares outperformed “growth” over the past couple of days.

Source: ?Ycharts.com

3. Related to the Deutsche Bank comment above, European financials continue to underperform. Comments reminding us of 2011 and even 2008 have been circulating in the social media and the blogosphere. Folks out there love a good financial crisis.

Leave A Comment