Let’s start with emerging markets where we want to cover a number of developments.

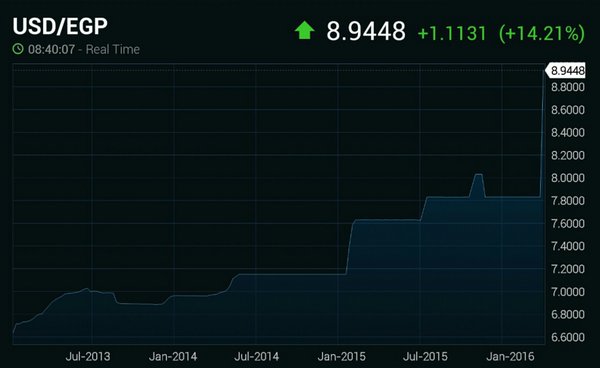

1. Egypt, running low on dollars, devalued its currency sending the Egyptian pound down some 14% (chart shows the number of pounds one dollar buys).

Source: Investing.com

2. India’s CPI seems to have stabilized (below consensus). Given the weakness in the nation’s industrial output (discussed yesterday), are we looking at more RBI rate cuts?

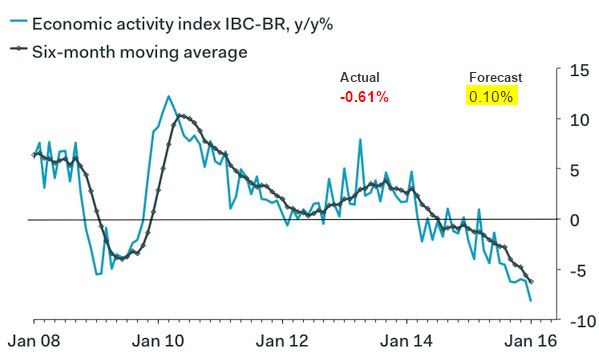

3. Brazil’s economic activity index came in below expectations as signs of recovery remain elusive.

Source: @andres__abadia

4. As Russia decided to pull out of Syria, the Russian ruble moves higher (chart shows the number of rubles one dollar buys – fewer rubles means the ruble is more expensive).

Source: CNN

Source: barchart

Also, Russia announced that Iran insists on oil output recovery before a possible freeze. Iran will therefore be “exempt” from the deal. This news sent crude oil prices lower, with Brent falling below $40 again.

5. Are portfolio managers under-allocated emerging markets? The rebalancing into developed markets hit new highs recently.

Source: Jefferies

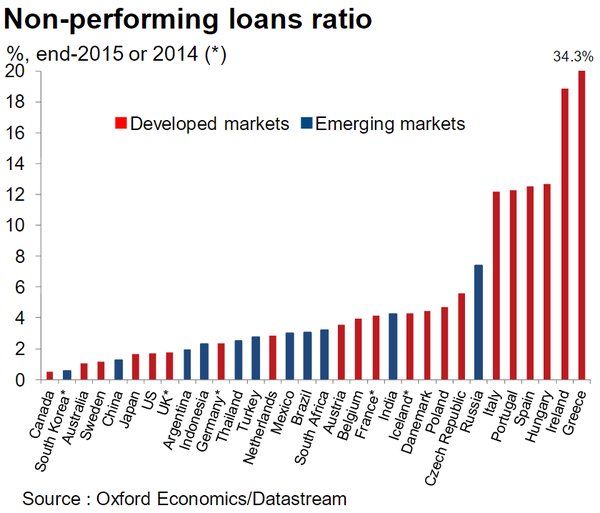

6. Here is the breakdown of non-performing loan ratio by country – comparing emerging and developed economies.

Source: @OxfordEconomics

Continuing with emerging economies, here are a few updates on China.

1. Starwood Hotels received an unsolicited bid from a Chinese-led investor group. Shares jumped nearly 8% in response. It will be interesting to see if this becomes a political issue in the US.

Source: Google

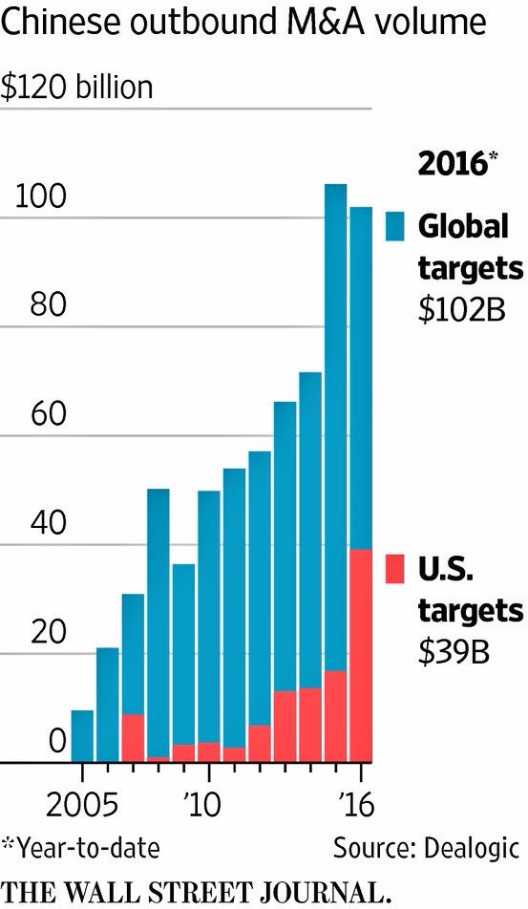

In general, China’s global M&A targets $102bn in 2016 with $39bn in the US. Right in time for the US election.

Source: @WSJ, @EMgist

2. Are China’s reserves adequate in relation to the liabilities? Using the IMFs risk-weighted methodology, apparently the nation’s reserves are just below the “adequate” cutoff.

Leave A Comment