We begin with a few updates on the energy markers.

1. US miles driven reaches another record as Americans hit the road.

This has resulted in elevated gasoline demand which remains firmly above the 5-year range.

Source: Credit Suisse

Gasoline expenses are quite low as a share of disposable income and should continue to add to the demand.

Source: Credit Suisse

2. The amount of global crude oil sitting in floating storage remains elevated. This is expected to pressure Brent prices.

Source: ?Deutsche Bank

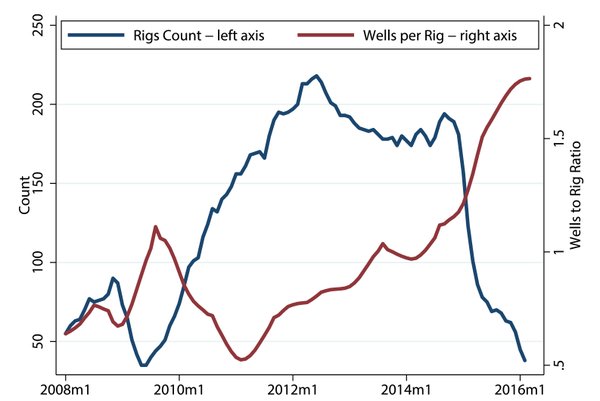

3. Productivity improvements at US oil firms have been impressive. As the number of rigs continues to fall, the number of wells per rig increases.

Source: The Federal Reserve, h/t @kkalev

4. Related to the above, energy CAPEX is expected to fall further in 2016. At some point, the US oil production declines should accelerate.

Source: @standardpoors

Turning to the US economy, the latest service sector PMI (from Markit) is not encouraging. Here is the commentary.

Source: Markit

As discussed before, some of the early projections for US Q1 GDP growth have been too optimistic. The Atlanta Fed Q1 GDP tracker is getting back to reality – and is now more consistent with the PMI report above.

Source: @AtlantaFed

Here are several other developments in the US.

1. Without the fancy seasonal adjustments, the US factory orders trend looks terrible.

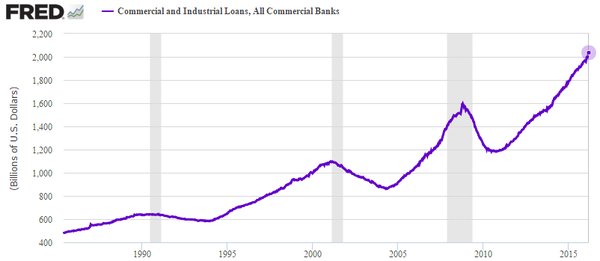

2. Corporate loans on banks’ balance sheets in the US are still growing at nearly 11% per year. There is no evidence of a significant bank tightening in the corporate credit markets.

3. Banks are ramping up home equity lines for US consumers. As the second chart below shows however, the overall usage (the drawn amount) of home equity lines is still declining.

Source: @NickatFP, @WSJGraphics, h/t Jake

4. US federal government debt to GDP ratio hits a new high. The nominal GDP growth is not keeping up with the US budget deficit (the US is not yet “growing out of” its central government debt).

Related Posts

Bristol-Myers Squibb Is Prepared To Heal Itself

Bristol-Myers Squibb Is Prepared To Heal Itself Are Fairstone personal loans worth It?

Are Fairstone personal loans worth It? Thai SEC to tighten up rules for crypto, focus on investor protection

Thai SEC to tighten up rules for crypto, focus on investor protection- Car makers may face tougher CO2 curbs

EUR/USD: Pressure Builds Up On The Upside, Eyes The 1.1724 Zone

EUR/USD: Pressure Builds Up On The Upside, Eyes The 1.1724 Zone Stewart To Be Acquired By Fidelity National In Deal Valued At About $1.2B

Stewart To Be Acquired By Fidelity National In Deal Valued At About $1.2B

Leave A Comment