“Greece, long Europe’s economic problem child, is trying to prove that it has made progress in its recovery efforts by announcing plans to sell debt for the first time in years. The proposed bond sale, the details of which were released on Monday, offered hope that Greece might at last be preparing to wean itself off the international bailouts totaling 326 billion euros, or about $380 billion, that it has relied on since 2010 to stay afloat. The sale is a pivotal moment in the painfully fought efforts of Greece to recover from troubles stemming from the financial crisis that began on Wall Street nearly a decade ago and that at one point threatened to break up Europe’s currency union.” (Liz Alderman, NYT, July 24, 2015)

“Athens has sold €3bn worth of its new five-year bond, at a yield (or interest rate) or 4.625%. That’s lower than the 4.95% that Greece last sold five-year bonds for, in 2014.” (Liz Alderman, NYT, July 24, 2015)

For a number of years Greece has been the poster child of everything that can go wrong for a small open country which is also a member of the European Union. The Greek banks and the national government have been in a precarious financial state for some time.

There is little doubt that the Greece still requires help to finance its outstanding debts even at current low market rates of interest. The markets recognize that Greece will require a fourth bailout when the current one expires next August.

The real economy in Greece expanded 0.4% in the first quarter of 2017 over the same quarter of the previous year. As the following chart shows, Greece’s real GDP growth has been roughly flat for the last two years now after experiencing massive contractions following the 2008 downturn and the country’s own financial crisis.

A measure of how much the Greece economy has shrunk can be seen in the following chart which traces the massive decline in per capita GDP expressed in U.S. dollars.

Related Posts

Twitter Inc. Dives After Earnings For Stagnant User Growth

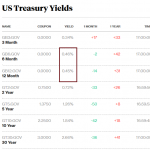

Twitter Inc. Dives After Earnings For Stagnant User Growth Portion Of U.S. Treasury Yield Curve Inverts

Portion Of U.S. Treasury Yield Curve Inverts GBP/USD: Reverses Losses On A Rally, Eyes 1.3300 Zone

GBP/USD: Reverses Losses On A Rally, Eyes 1.3300 Zone What Is “Solid Economic Reasoning”?

What Is “Solid Economic Reasoning”? June 2018 Headline Consumer Credit Growth Rate Well Under Expectations

June 2018 Headline Consumer Credit Growth Rate Well Under Expectations Gold Vs S&P 500: Polar Opposite Price Patterns

Gold Vs S&P 500: Polar Opposite Price Patterns

Leave A Comment