What about the stronger-than-expected Q3 GDP report? The first read of Q3 GDP surprised to the upside, printing at 2.9%. This was better than the Street consensus estimate of 2.6% and the Atlanta Fed GDPNow estimate of 2.1%. It was also a big improvement from the Q2 reading of 1.4%. However, there were some potential anomalies/phenomena signs to consider.

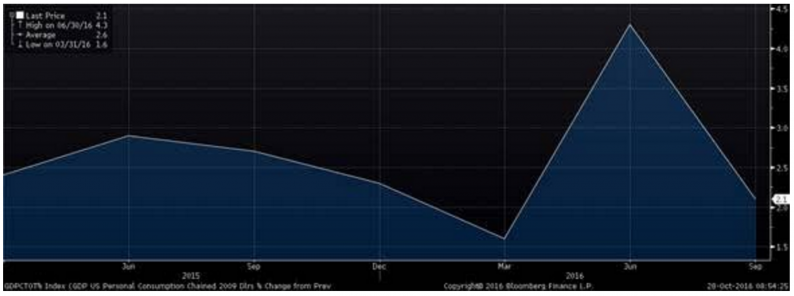

U.S. Personal Consumption since 2015 (Bloomberg):

I believe Q3 2016 was a “catch-up” quarter rather than the start of a new trend. As a catch-up quarter, it is just “alright,” as recent history demonstrates.

U.S. GDP since 2010 (Bloomberg)

I do believe that the Q3 rebound does indicate that the U.S. economy remains on its 2.0% growth track. Just as those who saw doom and gloom in the first half of 2016 were proved wrong (I was not among them), I believe that those who are euphoric about today’s GDP print will also be proved incorrect. During the current earning season, many (if not most) CEOs of multinational corporations warned of slowing global growth. If correct, slowing global growth could slam the brakes on U.S. exports, particularly if the U.S. dollar remains strong.

Related Posts

EUR/USD Trades In A Downtrend Channel As August Draws To An End

EUR/USD Trades In A Downtrend Channel As August Draws To An End Retail Sales & Earnings Season Highlight An Expected Turbulent Week For Markets

Retail Sales & Earnings Season Highlight An Expected Turbulent Week For Markets Iran CB to open accounts at South Korean banks

Iran CB to open accounts at South Korean banks Whiskey Wanters Win

Whiskey Wanters Win- Gold Strong Trend Could Reverse As Risks Ease

- World Markets Weekend Update: The Selloff Resumes

Leave A Comment