When celebrity investor Mark Cuban announces to the world that he is investing in gold, is that a sign that the ride up is just getting going, or that it has already peaked? The Gold Report reached out to long-time experts in the sector for a better understanding of what is moving the markets—negative interest rates, a topping dollar, Fed testimony, increased gold buying in China—and what that means for junior mining stocks in the coming months.

A lot of investors were turning back to gold in mid-February as an alternative to a larger stock market that didn’t seem to make sense anymore. The Dow Jones Industrial Average dropped 1.6% in one day, falling below its August low and spooking the chart-watchers. “I think people are so confused about this market. Nobody really understands what’s happening, including me,” billionaire businessman Mark Cuban told CNBC’s “Fast Money: Halftime Report” on Feb. 11. “When traders don’t know what to do, they go where everybody is. And I thought that would be gold.” He then shared his recent purchase of gold call options, not as a hedge, but in anticipation of momentum pushing the price of the metal higher.

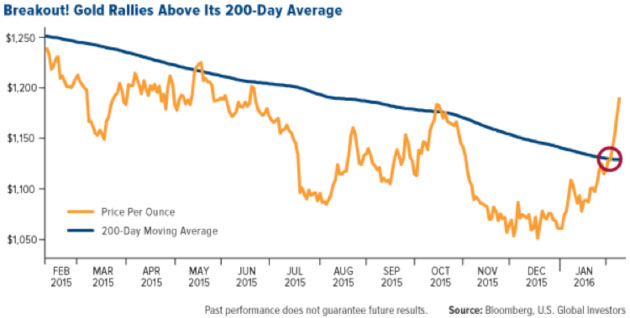

The day before, Frank Holmes, CEO and chief investment officer at U.S. Global Investors Inc., predicted in his blog that gold was shaking off its downward trend after three years of losses and that these highs will be “stickier” than previous rallies. His optimism was based on the gold price breaking through above the 200-day moving average.

Holmes pointed to increased demand for gold from China, where physical delivery reached a record 2,596 tonnes, and increased gold coin sales in Europe, the U.S. and Australia. He also noted that a trend toward negative interest rates in Sweden and Japan also makes gold more attractive.

We asked some of our most popular experts to comment on the fundamentals Holmes quoted.

Joe Foster, lead investment team member with the Van Eck International Investors Gold Fund, also credited increased Asian demand for pushing precious metal prices up, and pointed out that what is good for gold could be even better for gold equities. In a note to investors, Foster said, “It makes sense that equities should outperform gold during rising gold prices, and underperform if gold falls. We now see the industry in the best shape it has been in for a long time. Unfortunately, this positive transformation of the sector coincided with, and to some extent was intensified by, a period of falling gold prices. Equities have consistently demonstrated their effectiveness as leverage plays on rising gold during these past years.”

Related Posts

Three reasons why EOS price has pumped 100% in three days

Three reasons why EOS price has pumped 100% in three days UST staking goes live on Binance as Anchor reserves fall

UST staking goes live on Binance as Anchor reserves fall What Wall Street Thinks Of The Midterms

What Wall Street Thinks Of The Midterms Undersize Me? McDonald’s Franchise Owners Admit Fast Food Giant “Facing Its Final Days”

Undersize Me? McDonald’s Franchise Owners Admit Fast Food Giant “Facing Its Final Days” A Market Ready To Pull The Rug Out From Under You!

A Market Ready To Pull The Rug Out From Under You! Sucker Traps And The Arithmetic Of Risk

Sucker Traps And The Arithmetic Of Risk

Leave A Comment