Truth is a rare commodity on Wall Street. You have to sift through tons of dirt to find the golden ore. For example, mainstream analysis of the Fed’s current monetary policy claims that it will be able to normalize interest rates with impunity. That assertion could not be further from the truth.

The fact is the Fed has been tightening monetary policy since December of 2013, when it began to taper the asset purchase program known as Quantitative Easing. This is because the flow of bond purchases is much more important than the stock of assets held on the Fed’s balance sheet. The Fed Chairman at the time, Ben Bernanke, started to reduce the amount of bond purchases by $10 billion per month; taking the amount of QE from $85 billion, to 0 by the end of October 2014.

The end of QE meant the Fed would no longer be pushing up MBS and Treasury bond prices (sending yields lower) with its $85 billion per month worth of bids. And that the primary dealers would no longer be flooded with new money supply in the form of excess bank reserves. In other words, the Fed started the economy down the slow path towards deflation.

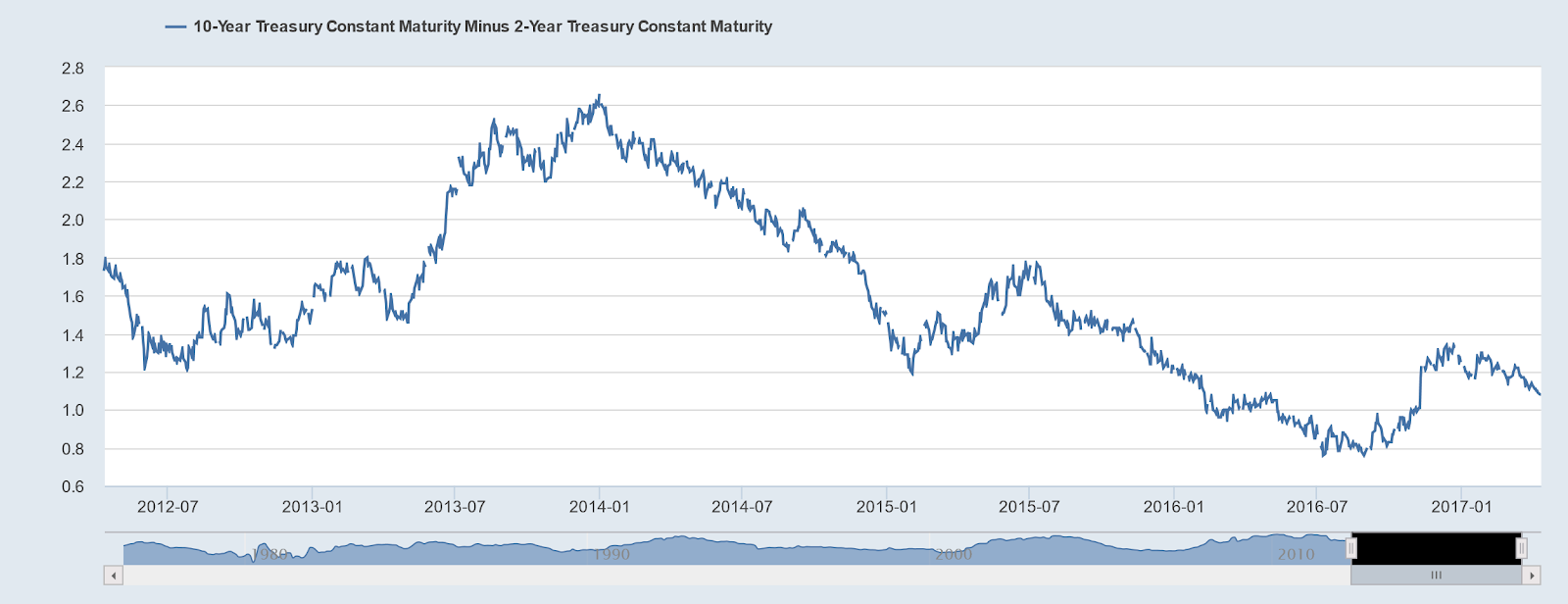

One of the greatest economic indicators is the steepness of the Treasury yield curve. A steep curve indicates inflation and strong growth; whereas a flat yield curve is indicative of economic stagnation and deflation.

Therefore, the view that the Fed has been in tightening mode for the past three years can be proven by the fact that the spread between the 10 and 2-Year Note yield began to collapse on the very month that the Fed began to Taper QE. That difference was 260 basis points in December 2013, but narrowed all the way down to just 76 basis points by the summer of 2016. Then, after a small recovery to 134 bps—mostly due to the enthusiasm caused by the election of Donald Trump—the spread is quickly retreating back towards 100 bps.

It is no coincidence that the 2-10 spread began to contract concurrently with the Fed’s taper of QE. Tapering is indeed tightening, even though the Fed tends to believe in a stock versus flow analysis. But now, Chair Yellen and the other members of the FOMC have indicated that two or three more rate hikes during this year are a distinct possibility. This is in addition to already increasing the Fed Funds Rate by 25bps in both December of 2016 and March of this year. Even more, the Fed has proposed to cease rolling over its asset holdings; as its $2.4 trillion worth of Treasuries and $1.7 trillion in MBS securities mature. That process is scheduled to begin by the end of 2017.

Related Posts

Chainalysis acquires cybercrime investigative firm Excygent in fight against ransomware attacks

Chainalysis acquires cybercrime investigative firm Excygent in fight against ransomware attacks From RCAT To SMCI: How We Nailed Yesterday’s Biggest Winners

From RCAT To SMCI: How We Nailed Yesterday’s Biggest Winners Double-Digit Year/Year Declines In The Dollar

Double-Digit Year/Year Declines In The Dollar Flippening? Record $10B Ethereum futures volume briefly outpaces Bitcoin’s

Flippening? Record $10B Ethereum futures volume briefly outpaces Bitcoin’s Senator Cynthia Lummis excited to buy the Bitcoin dip

Senator Cynthia Lummis excited to buy the Bitcoin dip The Bull: Why AAPL Now Has Its Highest Price Target Yet

The Bull: Why AAPL Now Has Its Highest Price Target Yet

Leave A Comment