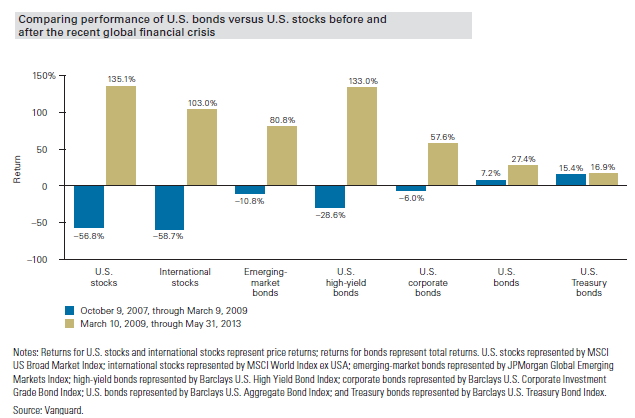

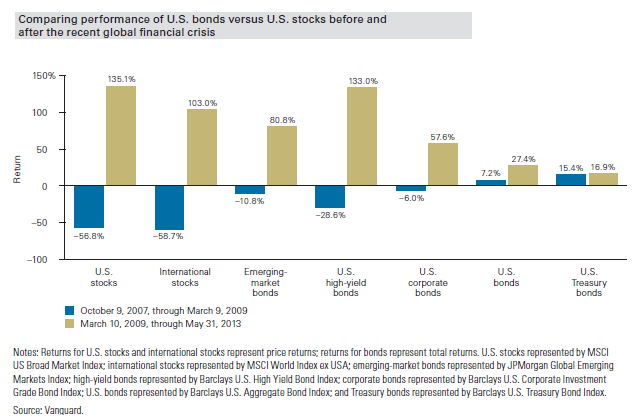

Although the rate of interest currently paid on high quality bonds today is at levels last seen in the early 1950’s, investors generally allocate a portion of their investment portfolio to bonds. One reason for having a portion of an investment portfolio in bonds is the fact bonds tend to hold up well when equity prices decline. Proof of this can be seen in the below chart comparing various stock returns to different bond category returns during the financial crisis. During the worst of the financial crisis that began in October 2007, U.S. stocks fell 56.8% while the Barclay’s Aggregate Bond Index and Barclay’s U.S. Treasury Bond Index were up 7.2% and 15.4% respectively.

Source: Vanguard

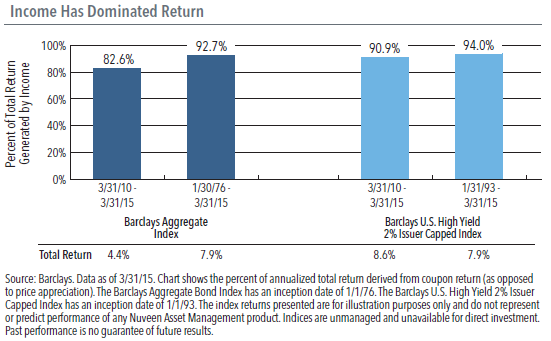

One near certainty is the Fed will increase interest at some point with it simply a question of when not if. When interest rates are moved higher (some believe a December liftoff), bond prices will decline and bond investors may be in for a bit of a surprise. A unique characteristic facing investors today is the rate of interest paid on high quality bonds is at extremely low levels. Historically, bond investors obtained some support when rates increased due to the income support provided by bonds. The below chart from Nuveen highlights the high percentage contribution to return that income has provided to overall bond returns since the end of the financial crisis and since 1976.

Source: Nuveen

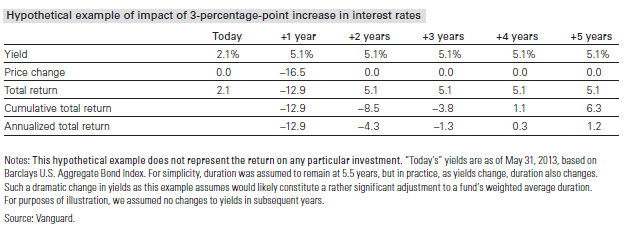

The below table from Vanguard is maybe a bit dramatic, but the table shows the impact on a bond’s price return given a three percentage increase in interest rates. One takeaway from the table is the amount of time it takes to recover the principal loss through the interest payment: over three years. This extended recovery is a result of the low interest rate starting point, 2.1% in the example and not far from today’s rate.

Source: Vanguard

T. Rowe Price recently opined on this same issue in a recent report. The firm notes,

Related Posts

Aircraft Orders: The Only Durable Goods Item Humming

Aircraft Orders: The Only Durable Goods Item Humming- Morgan Stanley: “Market Is So Distorted” The Fed Is Being Forced Into A “Pain Trade”

EC

Personal Savings Up, Meaning No Energy ‘Tax Cut’

EC

Personal Savings Up, Meaning No Energy ‘Tax Cut’ The Most Consistent Performing Hedge Funds Over The Past Five Years

The Most Consistent Performing Hedge Funds Over The Past Five Years- Bitcoin bulls may ignore Friday’s $730M options expiry by saving their energy for $40K

5 Top Stocks To Make The Most Of March Madness

5 Top Stocks To Make The Most Of March Madness

Leave A Comment