The NASDAQ served up an annualized return of 66% in its final two years of dot-com mania. Only after the balloon had burst did people begin to question the lunacy of paying 10x revenue for the privilege of being a shareholder.

Ironically enough, since early 2016, the top 10 growth names in tech collectively produced an annualized return of 67%. That’s right. The NYSE FANG+ Index has topped turn-of-the-century craziness.

For the current bull-bear cycle, then, we may be witnessing peak FANG fanaticism. Components of the NYSE FANG+ Index like Facebook (FB), Netflix (NFLX), Twitter (TWTR) and Nvidia (NVDA) currently sport mind-boggling price-to-revenue (P/S) ratios of 13.3, 12.3, 10.9 and 15.3!

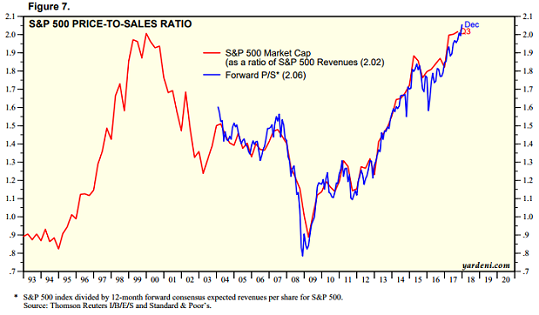

How zany are price-to-sales ratios above 10? For one thing, the S&P 500’s forward P/S above 2.0 is already the most expensive in history. And that includes the tech bubble at the start of 2000.

In the same vein, if one employs traditional valuation thinking, a P/S of 10 implies that a company need deliver 100% of its revenue stream for each year across a decade to provide a 10-year payback. Even with massive tax cut relief and exceptionally attractive borrowing terms, even with share buybacks by the boatload, it is virtually impossible to deliver 100% of corporate revenue stream back to shareholders for 10 consecutive years.

Investors should not pretend that they’re investing in the longer-term profitability of FANG+ components either. Amazon (AMZN) has been struggling with its cumulative profits and free cash flow for its entire existence. Pretending that the world’s second largest company by market capitalization justifies its forward price-to-earnings (P/E) ratio of 186 because it has transformed business as we know it is preposterous.

In truth, during the current bull-bear cycle, the stock shares of great companies have been getting pushed exponentially higher by machines that employ algorithmic trading. When the bear portion of the cycle hits, the “algos” will crush the overly leveraged FANG+ zealots.

Related Posts

Pro traders buy the Bitcoin price dip while retail investors chase altcoins

Pro traders buy the Bitcoin price dip while retail investors chase altcoins Crypto-centered public companies record profit beating Q2 estimates

Crypto-centered public companies record profit beating Q2 estimates February 2018 Initial Unemployment Claims Rolling Averages Continues To Improve

February 2018 Initial Unemployment Claims Rolling Averages Continues To Improve Best Of Old School Value 2017

Best Of Old School Value 2017- EC

Characteristics Of US Minimum Wage Workers

E

Canada’s Merchandise Trade Deficit Narrowed Dramatically In June, Though Future Trade Prospects Remain Cloudy

E

Canada’s Merchandise Trade Deficit Narrowed Dramatically In June, Though Future Trade Prospects Remain Cloudy

Leave A Comment