Verizon (VZ) and AT&T (T) are big dividend telecom stocks with a reputation for safety. Many investors own them specifically for the high dividend yields (4.4% and 5.2%, respectively) and the low betas (0.2 and 0.3, respectively). However, both companies are being forced to deal with the same fundamental challenge: declining wireline business and dwindling wireless growth. The companies are dealing with the challenge differently, but the result is the same: more long-term risk. We consider whether a Yahoo acquisition makes sense for either company, and also address two big questions for shareholders: 1) How will “more long-term risk” impact price appreciation for Verizon and AT&T, and 2) How will it impact the dividends.

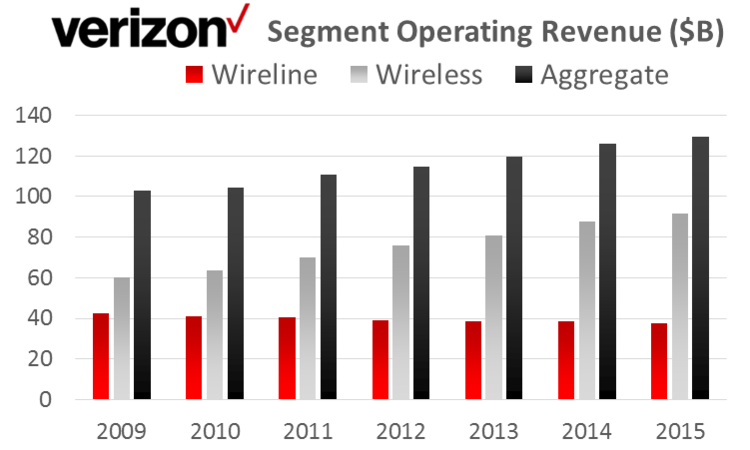

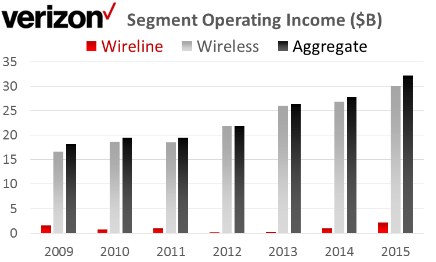

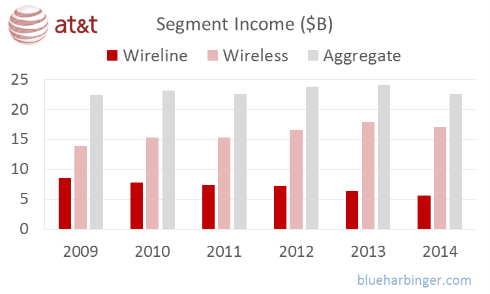

For starters, let’s look at the wireline results for both companies. As the charts below show, it is in decline for both Verizon and AT&T.

Note: AT&T’s segment income only goes through 2014 because in 2015 they changed their strategy (because it was struggling). Specifically, they acquired DirectTV for $48.5 billion, and they revised their operating segment breakdown into Business Solutions, Entertainment and Internet Services, Consumer Mobility, and International (more on AT&T’s new strategy later).

And regarding wireless business, the charts suggest that it is holding up. However, according to Verizon CEO, Lowell McAdam (Annual Report, p.3):

“New entrants are disrupting the wireless and broadband space. Competition is putting pressure on prices and margins… this suggests to investors that growth will be more challenging going forward.”

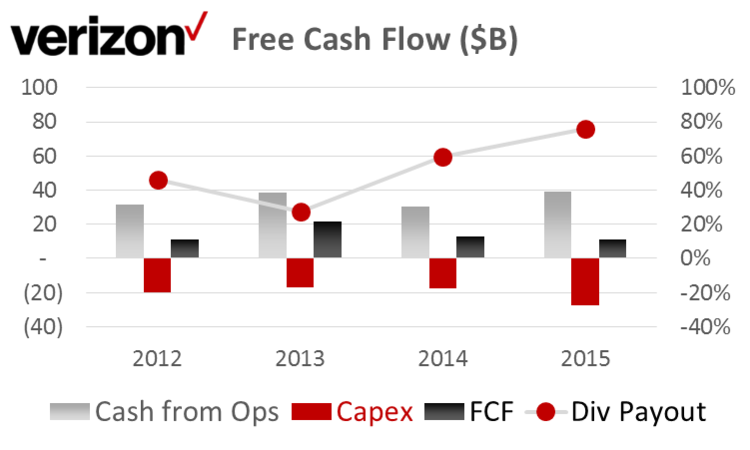

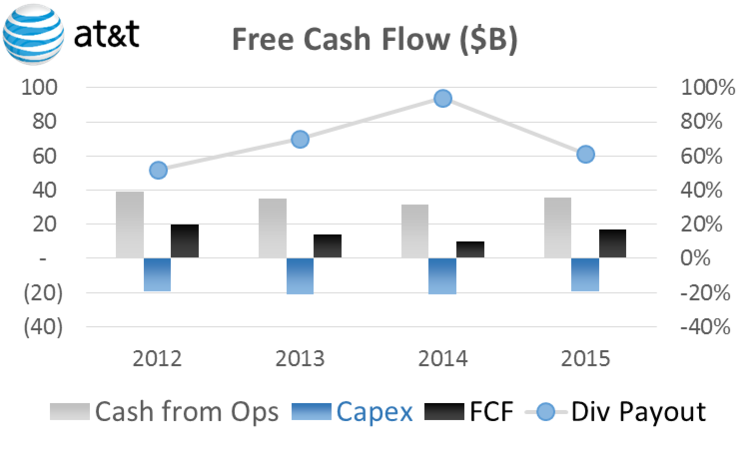

Next, let’s look at the free cash flows (FCF) for both companies. This is critically important for both companies because their long-term ability to pay dividends is dependent on their ability to generate sufficient free cash flow.

AT&T’s Evolving Strategy and New Risks:

As the free cash flow chart above shows, AT&T was paying out nearly 100% of their available free cash flow as dividends in 2014. And at the rate of increase in previous years, AT&T would have soon not been able to continue paying its big dividend if they didn’t do something drastic. And considering AT&T had already cut costs to the bone, their desperate action was to purchase DirectTV. And they did it NOT because it was a compelling long-term investment, but rather because it allowed them to structure the acquisition deal in a way that would increase the FCF available to AT&T shareholders and decrease the dividend payout ratio.

In our view, AT&T’s solution (buying DirectTV) was made just to keep the dividend safe for a few more years by kicking their problems down the road. DirectTV is not a long-term solution. You can read our more thorough analysis here. Also worth noting, DirectTV is not AT&T’s only attempt at inorganic growth; they also recently purchased two cell companies in Mexico (more on this later).

Verizon’s Slowing Telecom Business

As the FCF chart (above) shows, Verizon’s dividend payout ratio (as a percent of FCF) is increasing steadily. It hasn’t yet reached the dangerously high level that AT&T reached in 2014, but it will be there soon if Verizon doesn’t do something to address it. Particularly, Verizon’s wireline margins are razor thin, and competition and demographics will continue to pressure its wireless business further. And considering Verizon’s investor base owns the stock largely for the big dividend, strengthening FCF is of paramount importance for Verizon. Verizon’s 2015 acquisition of AOL (for $4.4 billion) was a small step towards addressing the future, and it is perhaps a foreshadowing of what is to come. Specifically, if Verizon can’t do something to organically address their growth and cash flow needs, they’ll likely look to grow inorganically via bigger acquisitions. And this is where Yahoo comes into consideration.

Related Posts

Here Are BofAML’s 4 Reasons To Worry About Risk Assets

Here Are BofAML’s 4 Reasons To Worry About Risk Assets Firm Founders Have Moved On; Investors Should Also

Firm Founders Have Moved On; Investors Should Also- AAPL Sends The Nasdaq Lower

Risks Of Dovish Forward Guidance In The March ECB Monetary Policy Meeting

Risks Of Dovish Forward Guidance In The March ECB Monetary Policy Meeting Cointelegraph Consulting: Deep diving with Ethereum whales

Cointelegraph Consulting: Deep diving with Ethereum whales International Business Machines Corp. 2Q 2017 Earnings: Sales Miss Est.

International Business Machines Corp. 2Q 2017 Earnings: Sales Miss Est.

Leave A Comment