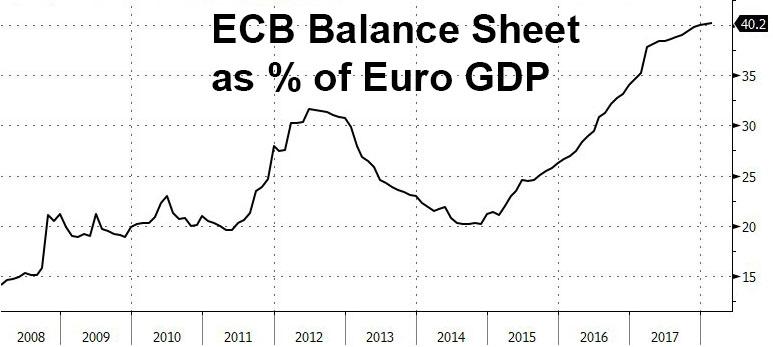

We find it amusing how much digital ink continues to be spilled to predict i) when the ECB will end its QE and ii) whether it will hike before or after it finally stops purchasing government and corporate bonds, or funnier yet, start selling them. The reason for that is that over the past 4 years, at the first indication of even the slightest market disturbance, the ECB comes rushing in to assure the market that all shall be well. As such, the world’s biggest hedge fund, which now owns more than 40% of Europe’s GDP in securities…

… remains forever entwined with the fate of the European capital markets.

The latest example of this was apparent in the latest week ended March 23, when the ECB nearly doubled its corporate bon buying the moment the market hit turbulence.

As the ECB reported several days ago, in the week ending March 23rd the ECB stepping up its purchases of corporate bonds under the Corporate Sector Purchase Programme, “oddly” at a time when EUR denominated IG non-financial spreads accelerated their march wider, and are now 23bp wider since February 2.

As Goldman calculates, after averaging €1.4 billion in weekly corporate bond purchases YTD, the ECB purchased €2.2 billion – 55% above their 2018 average and nearly double the €1.26BN in purchases from the prior week – in an effort to calm the market just as yields blew out.

It gets better: according to Goldman calculations, in the month of March, the ECB allocated 22% of its total APP purchases towards corporate securities. This is up from 18% in January and February, and only around 10% (on average) over the first 18 months of the program (through December of last year).

Some context: while on one hand Goldman makes it abundantly clear that the ECB is trapped and can not extricate itself from price formation without blowing up the bond market (it now owns roughly 15% of all outstanding European corporate bonds), and Draghi finds it unfathomable to allow the market selloff, and thus not only intervenes, but does so in force, the bank which spawned Mario Draghi forecasts a gradual tapering between September and December. At least there is no discussion on whether the ECB will taper its corporate bond buying program, something which the chart above clearly shows is impossible unless the ECB is willing to risk a blow out in European corporate yields.

Leave A Comment