Some of Davidson’s best work….

“Davidson” submits:

One of the most difficult tasks investors face is assessing the mass of detail presented every day, sorting them into buckets and identifying which should be significant factors and which should be ignored. Every day, markets appear to be threatened by events or policy changes which some indicate could create an economic/market top but then evaporate without impact. The media gives equal attention to each, then moves on to the next with the same emphasis. With so many threats presented with the same intensity seemingly poised to initiate economic collapse at a moment’s notice, one can be easily feel overwhelmed. This is where being disciplined with economic data takes out the guess work!

There are no ‘Black Swans’ in my opinion, just investors who let emotions rule investments and ignore economics. There is a long history of market prices, economic trends and investor psychology from which to draw. There are large themes which stand out: Individuals seeking better Standards of Living drive Economic activity, in turn economic activity drives market psychology and finally market psychology drives market prices. Major investment corrections come from economic corrections to investment imbalances like a line of dominos set to be knocked over with a single push. Corrections do not occur magically out-of-the-blue! Major corrections have a history of substantial warning. Most investors are lost in market details seeking ever more sophisticated analysis and fail to pay attention to or understand the larger and simpler drivers of economic activity. I believe too many have become dependent on modern technology and computer analysis. They believe past markets offer little value interpreting modern markets. Computers and a belief in AI(Artificial Intelligence) has replaced ‘old fashioned thinking’. In a world which appears messy, threatening and a global economy that continues to expand, I believe that ‘old fashioned thinking’ is the most important tool one can use.

There is broad acceptance that markets cannot be deciphered and that market psychology drives economic activity. The major problem with the focus on computer analysis today is that there is no means of assessing data as ‘colored’ by investor psychology. At market lows, when Value Investors dominate pricing, the prices are established according to their perceived valuations. At market peaks, when Momentum Investors dominate pricing, prices are established according to existing price trends at the time. Not only does computer focused-analysis not distinguish between the market psychology of Value vs. Momentum Investing, this type of analysis lumps all data regardless of source as having the same level of importance and reliability. For example, Purchasing Manager surveys are not economic but sentiment surveys, but they are deemed as valuable (sometimes more so) as employment reports which are economic measures. ‘Old Fashioned Thinking’ makes this distinction and ignores market sentiment.

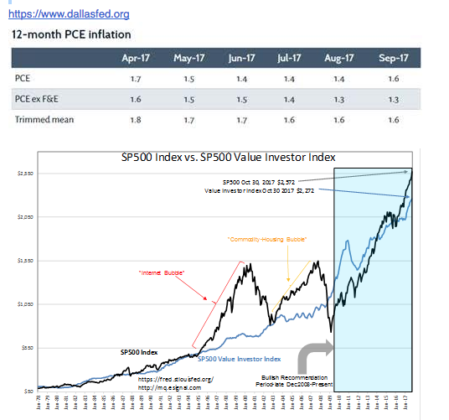

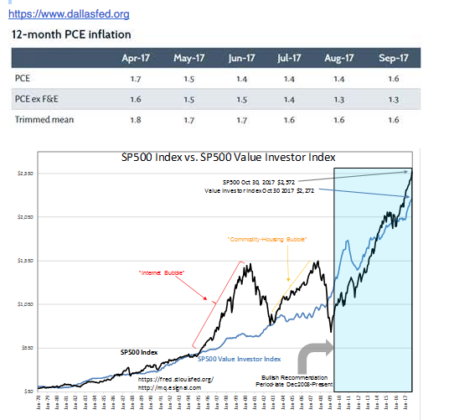

Three economic (not sentiment) indicators offer factual measures which let one look through the daily messy and conflicting mish-mash. First, is the SP500 Value Investor Index. This index provides a measure of market prices vs. long-term historical fundamentals. It permits one to compare market prices to the same fundamental valuation metric based on Knut Wicksell’s concept of “The Natural Rate”. It is based on Real Private GDP growth, the Dallas Fed’s 12-month PCE Inflation estimate and the long-term earnings trend for the SP500. With inflation reported recently at 1.6%, the SP500 currently at $2,572 is priced at a 13% premium to the SP500 Value Investor Index at $2,272. This is a modest level of market speculation with previous market peaks sporting premiums of 60%-100%. Markets remain modestly priced vs. past markets.

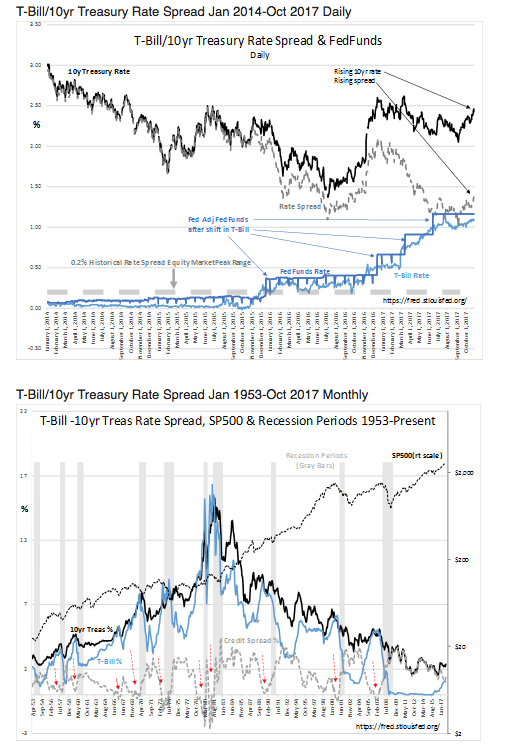

Second, is the T-Bill/10yr Treasury rate spread which is currently 1.35% (135bps-basis points). This rate spread with a history since 1953 is useful as a proxy for bank lending and investor psychology. When in recession with investors in a panic to sell equities, T-Bill rates are driven rapidly lower as investors shift to safety. This causes the T-Bill/10yr Treasury rate spread to widen dramatically to 2.5%-3.00%+. A sign of a high level of investor pessimism. As the economic cycle recovers, investors gradually become less pessimistic and the T-Bill/10yr Treasury rate spread narrows to 1.3%+/- range. This range roughly holds as the economic up cycle continues till investors finally become excessively optimistic and shift even backup capital into equities which drives T-Bill rates higher. High levels of optimism narrows the T-Bill/10yr Treasury rate spread to 0.20% (20bps) or lower. The spreads are so narrow at this point that bank lending losing its profitability slows markedly. Economic activity slows and a correction begins. The daily chart shows we are comfortably above 0.20% and economic activity continues to expand. The monthly chart from 1953 shows how reliable the T-Bill/10yr Treasury rate spread is as an indicator. The RED ARROWS tell the story.

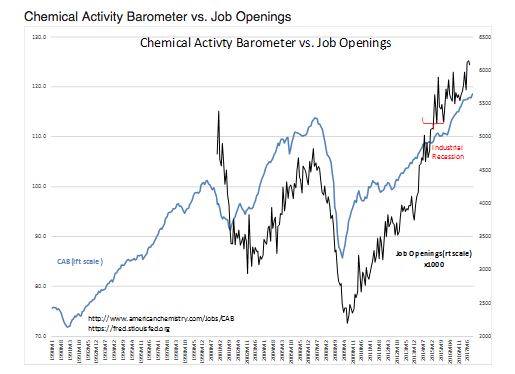

Third, shown here are the Chemical Activity Barometer(CAB) and Job Openings data, but other economic measures could have easily been used to arrive at the same analysis. Multiple economic measures indicate that economic activity from early 2009 continues and may even be accelerating. The history of the CAB series is impressive having been traced from 1919.

Summary:

Economic indicators provide investment signals well before investor market psychology begins to shift. Investors remain decently pessimistic while economic indicators forecast continued economic growth and higher profits. As more investors turn optimistic, markets should continue to rise higher. I expect markets to rise as long as the T-Bill/10yr Treasury rate spread remains favorable. One cannot predict how high. One can only discuss the potential. The SP500 in 3yrs+ has the potential to reach $3,500-$4,500. A wide range and over-valued, but it is impossible to predict how optimistic market psychology can become. For now, the best one can do is to simply say “higher”.

The cutoff point for equity investing will be in my opinion the T-Bill/10yr Treasury rate spread narrowing to 0.20%. At 1.35% today, we have 2yrs-3yrs of higher equity markets ahead in my opinion.

Related Posts

Bovespa Index Elliott Wave Technical Analysis 1

Bovespa Index Elliott Wave Technical Analysis 1 S&P Futures Soar, Global Stocks Rebound As Trade War “Perfect Storm” Fears Fade

S&P Futures Soar, Global Stocks Rebound As Trade War “Perfect Storm” Fears Fade Twitter (TWTR) Tops Q3 Earnings And Revenue Estimates

Twitter (TWTR) Tops Q3 Earnings And Revenue Estimates Crypto users spent $2.7B minting NFTs in first half of 2022: Report

Crypto users spent $2.7B minting NFTs in first half of 2022: Report US Job Growth Slows In March, But Annual Pace Holds Steady

US Job Growth Slows In March, But Annual Pace Holds Steady Qualcomm, Inc. 3Q 2017 Earnings: Shares Fall After Results, Guidance

Qualcomm, Inc. 3Q 2017 Earnings: Shares Fall After Results, Guidance

Leave A Comment