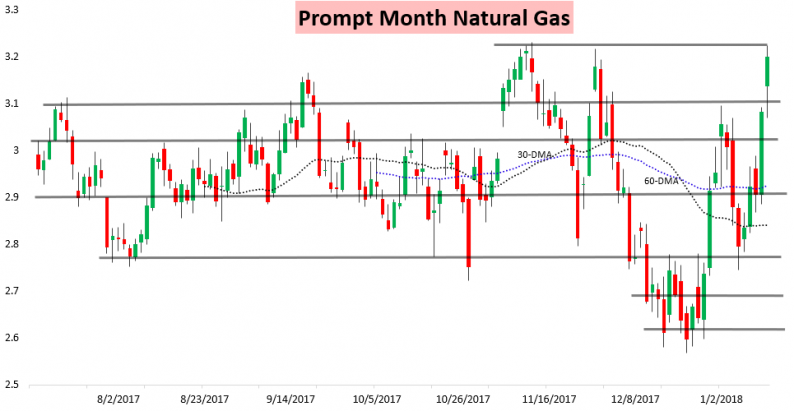

We had another wild day of natural gas trading today, with prices experiencing significant volatility this morning in attempting to pull back before slightly colder afternoon weather model guidance sent prices rallying into the settle.

Like yesterday, where you look along the natural gas strip determines how you saw price action. The February contract skyrocketed with the March contract making a solid move higher, and the rest of the strip ticked up just slightly.

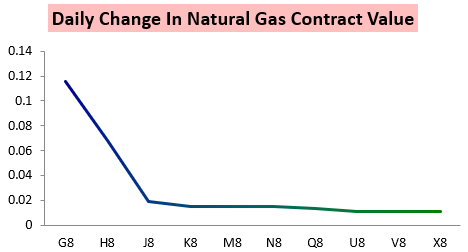

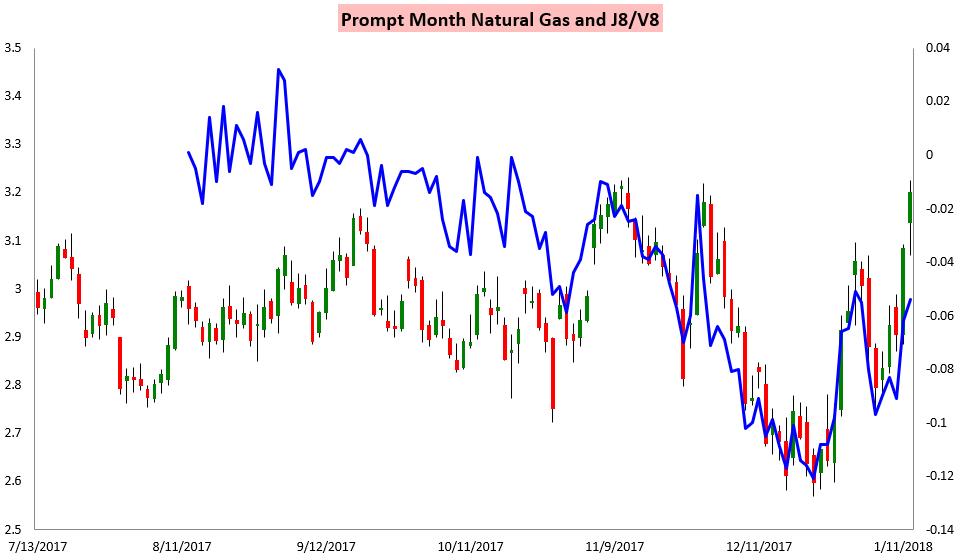

Shown differently, the G/H spread ballooned to record levels for the time of year, with the front of the natural gas strip taking all the risk with dwindling stockpiles heading into the end of the winter.

We can still compare that spread to the April/October J/V spread, whereby we see that the market remains convinced it can refill stockpiles from any starting levels this injection season as production surges.

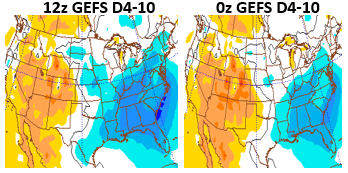

The surge came again at the front of the natural gas strip as we continued to add heating demand to the 15-day forecast today, with the afternoon GFS ensembles trending decently colder. We show the colder 4-10 Day forecast trends of this model below (courtesy of the Penn State Electronic Wall map site).

Much of the rally this week came as medium-term forecasts continued to trend colder, something we outlined was a continued risk for clients yesterday in our Note of the Day.

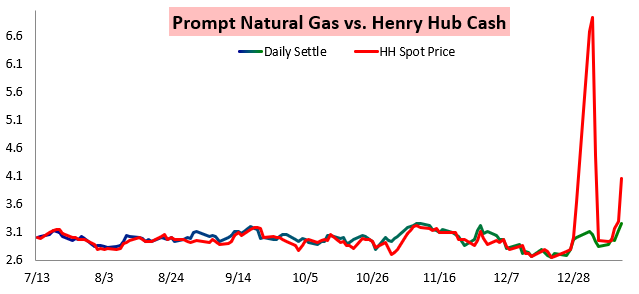

Clearly, those trends continued today, driving prices higher into the $3.20 level that we warned clients in our Morning Text Message Alert was “in play” given recent cash strength. This cash strength continued today, pulling Henry Hub spot back above $4.

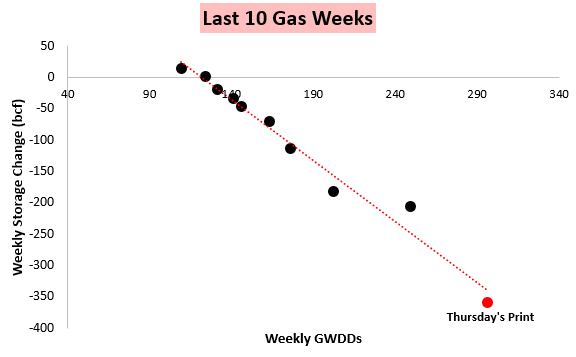

All of this came following what was an extremely EIA print announced yesterday.

Attention turns to next week now, where we should see another weak of very elevated volatility with short-term cold keeping cash prices elevated combine with late-week warmth and mixed long-range forecasts. Throw in rapidly dwindling natural gas stockpiles and elevated production, and we expect winter volatility to be in top form.

Related Posts

Kiwi Shot Down By Dovish Central Bank And US Protectionism

Kiwi Shot Down By Dovish Central Bank And US Protectionism Silver & Gold Are Surging

Silver & Gold Are Surging DAX Outlook As ECB Looms, S&P 500 Levitating While FTSE Seeks Resolution

DAX Outlook As ECB Looms, S&P 500 Levitating While FTSE Seeks Resolution Global Macro Trend Slips Closer To The Dark Side

Global Macro Trend Slips Closer To The Dark Side EUR/USD Closes Lower On Bear Pressure But With Caution

EUR/USD Closes Lower On Bear Pressure But With Caution Price analysis 11/29: BTC, ETH, BNB, XRP, SOL, ADA, DOGE, TON, LINK, AVAX

Price analysis 11/29: BTC, ETH, BNB, XRP, SOL, ADA, DOGE, TON, LINK, AVAX

Leave A Comment