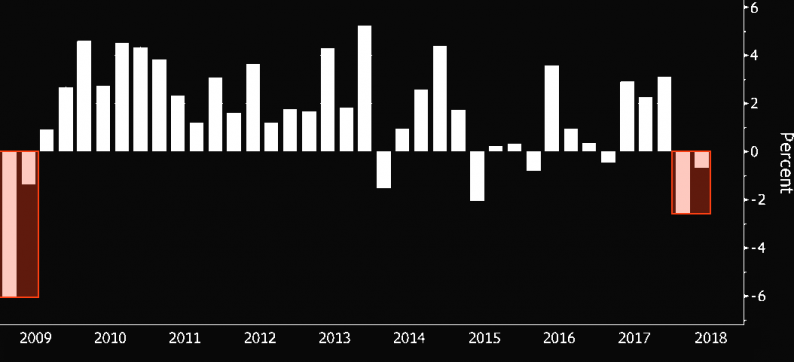

Well, South Africa is in a recession.

Q2 GDP fell an annualized 0.7% QoQ, missing estimates and confounding all but one economist surveyed by Bloomberg ahead of the report. The economy contracted by 2.6% in the first quarter. This is the first recession since 2009 and it marks a rather inauspicious start for Cyril Ramaphosa.

(Bloomberg)

Two people who aren’t surprised are Nedbank’s Mehul Daya and Neels Heyneke, whose research on dollar liquidity we’ve highlighted quite a bit in recent months. “We are not too surprised that South Africa has slipped into a recession,” Daya said Tuesday, adding that “we have had warning signals of this since the start of 2018 even despite Ramaphoria – this is because the financial cycle in South Africa has become bigger, more disruptive on the real economy than most acknowledge.”

To be clear, this was the last thing the rand needed. ZAR careened as much as 2.5% lower on the news and is the worst EM performer on Tuesday.

The currency has been under fire with the rest of the EM complex and had an extremely rough go of it in August.

(Bloomberg)

Multiple factors weighed on ZAR last month including, of course, concerns that it’s vulnerable from a fundamental perspective (current account) and thus likely to be one of the next dominos to tip after Turkey.

On August 12, just hours after USDTRY was quoted as high as 7.23 coming off a weekend during which Erdogan railed against the U.S. and pledged not to raise rates or seek an IMF lifeline to stop the bleeding in the lira, USDZAR flash crashed in yet another apparent Mrs. Watanabe stop out moment.One-month historical volatility jumped to its highest since 2016 in August.

(Bloomberg)

Notably, implied volatility picked back up amid renewed EM turmoil to close August after moderating during the dollar’s mid-month breather.

Related Posts

Gold Jigged, Silver Rigged, Stocks Pigged

Gold Jigged, Silver Rigged, Stocks Pigged RSP Vs. SPY: What’s The Difference Between These Two?

RSP Vs. SPY: What’s The Difference Between These Two?- E

Immunomedics Receives FDA Breakthrough Therapy Designation For Breast Cancer Drug

TON, TWT, CHZ and QNT breakout amid traders’ crypto contagion fears

TON, TWT, CHZ and QNT breakout amid traders’ crypto contagion fears Mobileye To Be Acquired By Intel; Deal Has Equity Value Of Approx. $15.3b

Mobileye To Be Acquired By Intel; Deal Has Equity Value Of Approx. $15.3b Cheat Sheet

Cheat Sheet

Leave A Comment